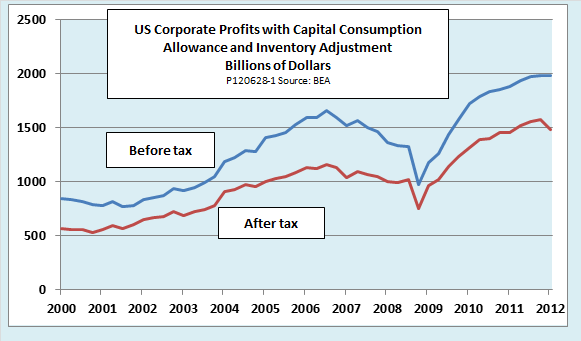

The BEA also released revised data showing that corporate profits in Q1 were weaker than previously thought. The broadest measure, corporate profits before tax with capital consumption allowance and inventory adjustment, decreased by 0.3 percent compared with Q4 2011. As the chart shows, that was the first decrease since profits hit their cyclical low in mid-2008. After tax profits with adjustments decreased much more sharply, by 5.9 percent. The difference reflected a whopping 20 percent increase in corporate profits taxes for Q1 2012 compared with Q4 2011.

The drop in corporate profits was largely due to weakness in the global economy. Domestic profits of U.S. corporations rose by a healthy 2.6 percent in Q1 2012 compared with Q4 2011 (5.7 percent for the financial sector and 1.4 percent for the nonfinancial sector). However, foreign profits fell by 12 percent, more than wiping out the increase in domestic profits, as receipts from the rest of the world fell and payments rose. (my emphasis)Read it at EconoMonitor

Latest Data Show U.S. Corporate Profits Falling Due to Global Woes while GDP Growth Remains Sluggish

By Ed Dolan

When the US housing decline began to create broader problems for developed economies, many people were quick to suggest that emerging markets had decoupled and would not be impacted by the developed world’s crisis. Despite those predictions being proven terribly wrong, as the current Eurozone crisis has picked up speed, the same individuals have been projecting the US will decouple and growth will be unaffected. Given the sharp decline in corporate profits, it appears decoupling proponents will once again prove mistaken. With S&P 500 earnings set to decline in the second quarter, this data suggests that current expectations of a minimal drop may still be optimistic. As Europe and China continue to slow, a turnaround in foreign profits is increasingly unlikely. It appears the US may already be in the midst of a profit recession.