While the implementation of capital controls presents an interesting storyline, Paul Krugman has raised a much bigger question into the public spotlight. After being challenged to expand the boundaries of political possibility, Krugman offered the following recommendation (emphasis added):

So here it is: yes, Cyprus should leave the euro. Now.

The reason is straightforward: staying in the euro means an incredibly severe depression, which will last for many years while Cyprus tries to build a new export sector. Leaving the euro, and letting the new currency fall sharply, would greatly accelerate that rebuilding.

The question for Cyprus is therefore whether “internal” or “external” devaluation offers the best prospects for the future? Let’s consider both of the options...

“Internal devaluation” (i.e. income deflation) - In return for continued assistance from the Troika (EU/ECB/IMF), Cyprus has agreed to impose losses on equity and debt holders, as well as uninsured depositors, of the two largest banks (Bank of Cyprus and Laiki Bank). This marks a distinct change in policy, especially with regard to the latter two groups.* Since uninsured depositors held a majority of those banks’ liabilities, the focus has naturally been on that group. Based on recent estimates uninsured depositors in the Bank of Cyprus may lose approximately 40%, while Laiki Bank’s uninsured depositors will be entirely wiped out.

The sharp reduction in (perceived) wealth stemming from these actions will put severe downward pressure on national income. Individuals and businesses experiencing losses will try to increase saving by reducing spending. Banks fearing deposit flight and falling asset prices will try build a stronger base of capital by restricting the supply of credit and possibly selling assets. Adding to the fall, the government will be forced to accept a MoU (Memorandum of Understanding) that establishes policies to increase taxes and reduce spending. Combining these deflationary pressures, the overall economic results may rival (or exceed) Greece’s recent history.

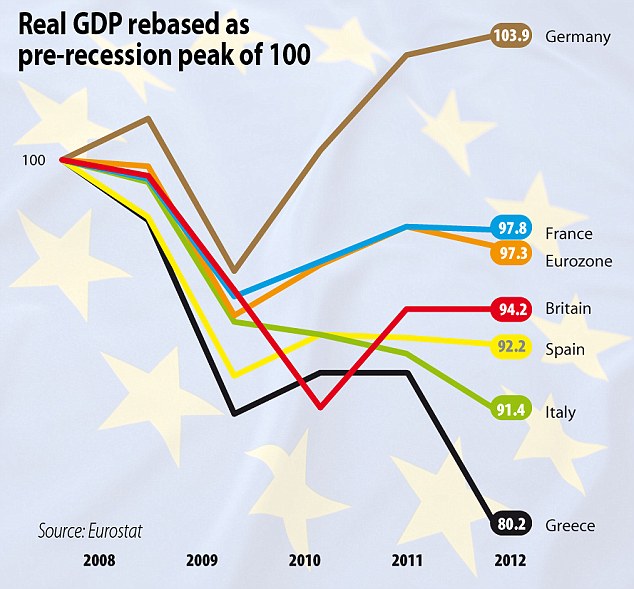

During the past 5 years Greece’s real GDP has declined by 20%

and unemployment has nearly quadrupled from ~7% to ~27%.

To offer some historical perspective, US unemployment during the Great Depression peaked at 25% and real GDP loss only exceeded 16% for one major European nation (Austria). Perhaps even more disheartening than the current data is recognition that output and unemployment appear unlikely to improve anytime soon.

Returning to Cyprus, unemployment has already quadrupled over the past 5 years (~3.5% to ~14%; shown above). Based on current estimates of a 20-30% drop in real GDP, Cyprus’ unemployment rate could easily approach or eclipse Greece’s in the next few years.

“External devaluation” (i.e. new currency) - If Cyprus were to leave the Eurozone, one of the first actions would be re-introducing the Cypriot pound at a heavily devalued rate against the euro. Not unlike the imposed losses on uninsured depositors, currency devaluation immediately imposes significant losses on all depositors. In this sense the impact on private demand would still be extremely deflationary, perhaps even more so. Though output and employment would fall dramatically, external devaluation presents reasons for potential optimism on both the foreign trade and government fronts.

Based on the recent bank losses and capital controls, Cyprus can no longer rely on its financial sector to support exports. By heavily devaluing its currency, Cyprus would be increasing its price competitiveness on the foreign market. However, as Barkley Rosser points out:

even with large elasticities [of trade relative to the exchange rate], there is the J-curve effect. Exports do not increase immediately, whereas the value of imports tends to jump up immediately with their price increases.Aside from these timing issues, there is also a concern regarding the certainty of each effect. A large devaluation will definitely raise the cost of living for Cypriots but as JW Mason comments, it:

might not lead to higher net exports in the next few years, or ever. That’s the question -- not how big the devaluation would be, but how strongly it will affect trade flows.

As for the government sector, returning to the Cypriot pound would remove some of the current fiscal constraints. This would permit the government to increase spending (ideally investment in a new export sector) and not raise taxes, raising private sector income. While these adjustments will not come remotely close to overcoming the other deflationary effects in the short-run, the counterbalance provided will be a significant improvement over current policy.

While this devaluation might make it easier for Cyprus to recover several years down the road, that recovery would indeed be several years down the road, and in the meantime there would be a lot of pain for the entire citizenry that will not happen if they stay with the euro.

If Greece has taught us anything about remaining with the euro, it’s that a lot of pain for the entire citizenry will happen regardless and a recovery may be decades down the road.

Cyprus is therefore faced with a choice between two terrible outcomes:

1) Remain in the Eurozone and experience a relatively slower “internal devaluation” whereby real output and employment experience large declines spread out over several years. A potential recovery is pushed even further into the future.

2) Leave the Eurozone and experience a quick “external devaluation” whereby real output and employment fall dramatically in the next year or two, but a recovery several years down the road becomes far more probable.

is that the real real issue here has to do with time preferences. It may get down to hyperbolic discounting. People do not want to have pain in the near term. So, the fear by the whole population of near term pain in terms of standard of living may outweigh fear of a more gradual decline with rising unemployment, even though the shorter term sharp pain is likely to lead to a sooner turnaround to growth.

Although this psychological tendency is very normal, it can at times be detrimental to achieving longer-term goals. The cases of Greece, Spain, Italy, Portugal, Ireland, and now Cyprus are examples of such times. The severe pain of reduced standards of living and high unemployment will be felt one way or another, but the option of “external devaluation” offers potential for a better future five and ten years down the road. Therefore I concur with Krugman, “Cyprus should leave the euro. Now.”

* From my perspective, imposing losses on debt holders should have been done from the outset in the US and Europe. The apparent change in policy may raise costs of debt financing for the largest banks, but that should be a welcome change after years of enjoying a TBTF subsidy.