A Nobel Laureate is taught the limit of his own assumptions. Others pile on: Philip Pilkington: Krugman Makes Accusations of Fundamentalism to Defend His Own Dogma and Debt, Income and Aggregate Demand: Scoring Krugman vs Keen

Insight into Google’s use of a “Double Irish Dutch Sandwich” and many other clever practices being used by GE, Microsoft, Apple, etc.

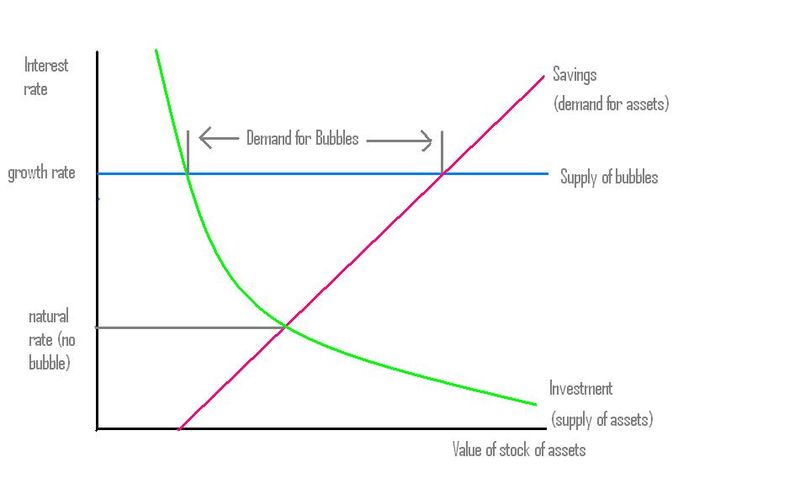

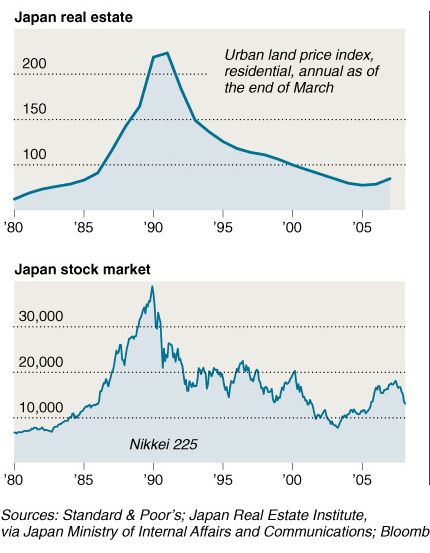

A former student of Minsky’s elegantly outlines the important aspects for understanding the reality of our financial and economic system. More on Minsky: Was 'Post-Keynesian' Hyman Minsky an Austrian in Disguise?

Without much fanfare, the “fraud-friendly JOBS Act” passed Congress this week with overwhelming support. William Black, a professor of law and economics, offers a history of anti-regulatory bills over the past several decades. If history is any guide, the JOBS Act will be front and center as having aided and abetted massive frauds during a financial crisis in the not too distant future. More on the JOBS Act: Bill Black: “The only winning move is not to play”—the insanity of the regulatory race to the bottom

What can I say...talk of The Hunger Games is everywhere these days!

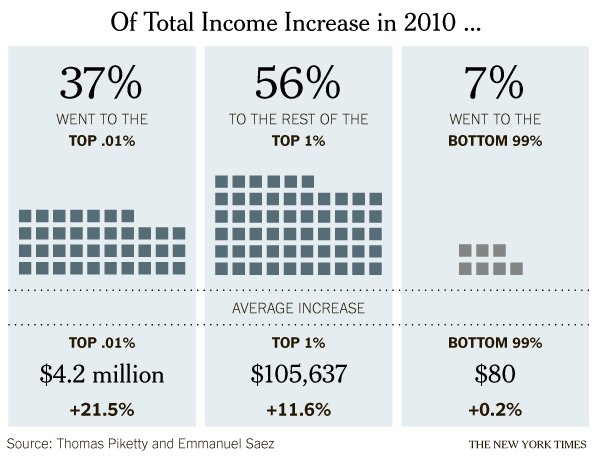

Source: NYT