The vast majority of the U.S. $727 billion trade deficit in goods for 2011 is due to "intra-firm" or "related party" trade, that is, trade between two units of the same corporation, according to the U.S. Census Bureau. This is significant because such trade is the most open to companies manipulating the prices between subsidiaries to minimize tax liabilities, usually known as abusive transfer pricing. Moreover, as Stuart Holland argued in 1987, intra-firm trade is also less responsive to changes in exchange rates than is trade between independent businesses, since within an individual multinational corporation each subsidiary will have a specific role to play in its supply chain, which won't be quickly changed.

U.S. goods trade and related party trade (billions of dollars), world and selected countries, 2011:

Country Exports from US Imports to US Balance

World $1480.4 $2707.8 - $727.4

World (RP) $ 365.0 $1056.2 - $691.2

Canada $ 280.9 $ 315.3 -$ 34.5

Canada (RP) $ 98.1 $ 162.0 - $ 64.1

Ireland $ 7.6 $ 39.4 - $ 31.7

Ireland (RP) $ 1.5 $ 34.6 - $ 33.1

Mexico $ 196.4 $ 262.9 - $ 64.5

Mexico (RP) $ 60.5 $ 155.7 - $ 95.2

…

The bottom line is that we need to reverse the incentives in the tax code that encourage the offshoring of jobs. (Why does Apple have $64 billion in cash abroad?) However, to emphasize the point I made last time about what Americans want out of tax reform and the "reform" that has actually happened, it's worth pointing out that Robert Gilpin of Princeton University, author of the seminal U.S. Power and the Multinational Corporation (1975), made the same policy recommendation almost 40 years ago, and it hasn't happened yet. We've got our work cut out for us.2) Zero rates have created a dangerous risk seeking return mentality by Edward Harrison @ Credit Writedowns

You saw the posts by Sober Look on the excess risk investors are taking on in the high yield market and the consequences of low yields on US households. Let’s make it a trilogy of posts then. There are plenty of other posts today that highlight this problem. And it is a problem. One thing Austrians harp on is the misallocation of resources caused by heavy handed and persistent interest rate market intervention. They are right that the industrial organization and the structure of investment capital priorities is critical to longer-term growth. What we are seeing now is a skew into high risk activities. As I wrote 4 years agoWoj’s Thoughts - Follow the last link for a marvelous step-by-step description of a credit bubble and bust. Harrison combines insights from the Austrian and Modern Money traditions, which is a prospect I hope to further in my own research.

3) The Jackson Hole "fix" is not coming by Walter Kurtz @ Sober Look

Market participants are looking for a fix, a repeat of the "high" Bernanke delivered at Jackson Hole in 2010 when QE2 was introduced. Markets however are in for a major disappointment because no outright asset purchases will be announced. There are multiple reasons for this, including the fact that real rates are now deep in the negative territory (as discussed here) and the policy as expressed in long-term real rates is far more accommodative than it was in 2010.

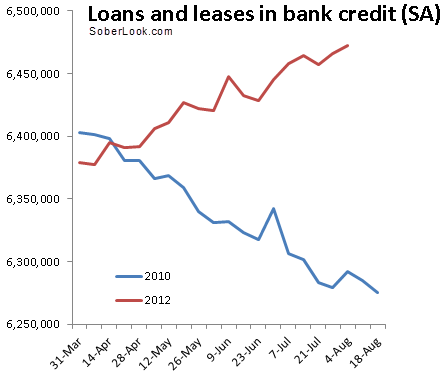

But what makes 2012 entirely different is that the key concern that pushed the Fed into asset purchases in 2010 no longer exists. The summer of 2010 was marked by renewed fears of deflation driven by credit contraction. The Fed was afraid of Japan-style deflationary pressures that are extremely difficult to arrest as bank lending shuts down. In the months preceding the 2010 Jackson Hole speech, credit was contracting sharply with banks steadily shrinking balance sheets. As discussed before, just the opposite is true in 2012 - credit is expanding at a decent pace. The chart below compares the trends now and in 2010.

Woj’s Thoughts - Kurtz goes on to suggest that markets may sell-off if disappointed by Bernanke, but I’m not convinced. Expectations of further “stimulus” have consistently proven resilient when faced with no new information. Markets may therefore simply shift expectations of further action to September, October, December and on, or until enough FOMC voting members explicitly state action is not coming.

Credit expanding?

ReplyDeletehttp://dollardeathspiral.blogspot.com/2012/08/consumer-credit-minus-federal-student.html

The argument that student debt is not the ideal form of credit expansion is reasonable. However, I haven't seen the Fed previously hint at using the measure you highlight in their determination of monetary policy. If you have comments from the Fed regarding this measure, please share them and I will happily stand corrected.

Delete