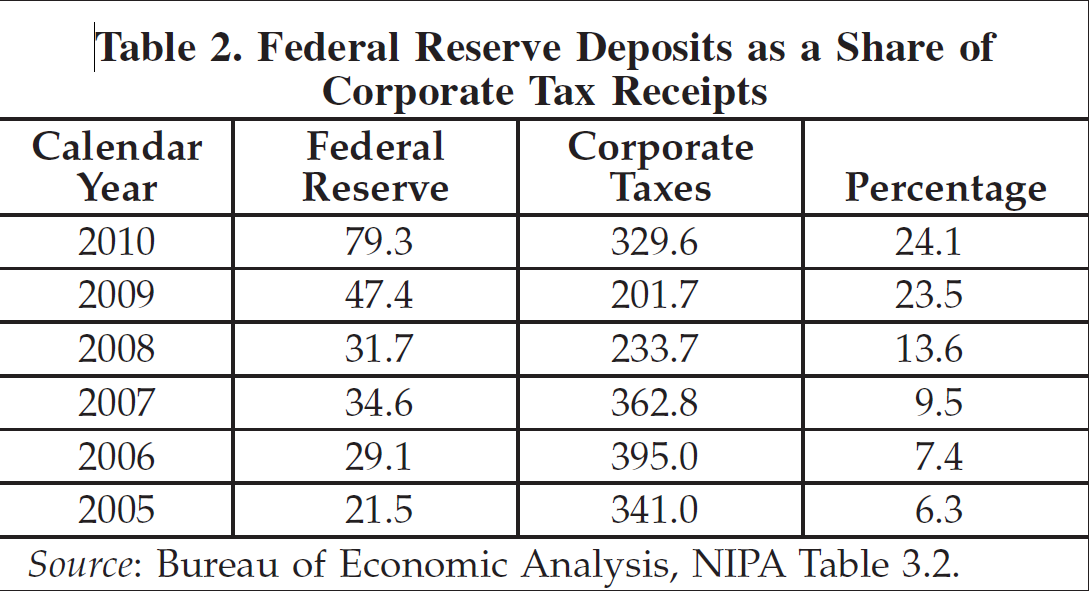

In the National Income and Product Accounts, the Fed’s revenue is considered part of corporate tax revenues. Because it constitutes close to a quarter of all corporate taxes, as shown in Table 2, this is important for analytical purposes when working with the data.

Read it at SSRN

The Fiscal Effects of the Federal Reserve

By Bruce Bartlett

(h/t Marginal Revolution)

During the past few years, the Federal Reserve has massively expanded its balance sheet to approximately $3 trillion. As a result of its holdings the Fed earns a significant amount of interest each year (over $75 billion in 2010 and 2011), most of which gets transferred back to the Treasury. Although MMT and MMR correctly note that the Fed and Treasury can be functionally considered as one entity, this distinction clearly remains absent from NIPA accounting.

Bartlett’s paper highlights an important, potentially overlooked, accounting principle that considers the Fed’s transfers to Treasury as corporate tax revenue. Separately, Bartlett points out that the Fed’s income is included in corporate profits from the financial sector. Given the increasing size of these figures, failure to recognize this distinction means that corporate profits and taxes may become increasingly overstated.

Stock market bulls frequently point to rising corporate profits and a rebounding financial sector to promote their views. Do these statistics include the profitability of the Fed, which is not really part of the private sector? If so, without the Fed’s “profits”, how would current corporate and financial sector profits compare with similar data from before the recession?

The Fed’s so-called “profits” actually work as a tax, removing income from the private sector. As the Fed’s balance sheet continues to expand in coming years (a seemingly common assumption) these “profits” will almost certainly make up an even larger portion of corporate profits and taxes. Recognizing this accounting quirk is clearly integral to providing useful analysis for both policy making and investing.

No comments:

Post a Comment