Lars Christensen points us toward an article by Ambrose Evans-Pritchard:

Mr Abe plans to empower an economic council to “spearhead” a shift in fiscal and monetary strategy, eviscerating the central bank’s independence.

The council is to set a 3pc growth target for nominal GDP, embracing a theory pushed by a small band of “market monetarists” around the world. “This is a big deal. There has been no nominal GDP growth in Japan for 15 years,” said Mr Christensen.Since my extreme skepticism towards NGDP targeting has been previously outlined on numerous occasions (here, here, and here for example), I won’t rehash those arguments now. With Monetarists focusing attention on the possible NGDP target, I want to consider a different view from Tim Duy (h/t Economist’s View):

The loss of the Bank of Japan's independence to force the direct monetization of deficit spending is the real story.

…

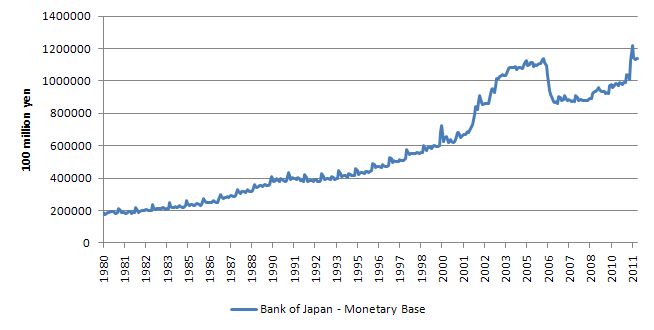

Bottom Line: Inflation targeting is not the whole story in Japanese monetary policy. It is a facet of a much greater story. A story of a modern central bank stripped of its independence. Of a modern central bank forced to explicitly monetize deficit spending. Ultimately, it is the story of the end game of the permanent zero interest rate policy.Over the past couple decades, the Bank of Japan (BOJ) has been implicitly monetizing deficit spending through its own QE programs (graph courtesy of billy blog) :

The question then becomes, is making these actions explicit really a game changer? The BOJ has been unsuccessful in trying to stimulate private credit markets (and thereby growth and inflation) for the better part of two decades. Zero-interest rates, a rapidly expanding balance sheet, and unconventional asset purchases have all failed to do the trick. If removing the central bank’s independence simply results in more of the same, with larger quantities and new targets, then I fail to see why the outcome will be any different.

From my perspective, the loss of independence only really matters to the degree it permits a looser fiscal stance. As modern money proponents have frequently shown, currency issuers such as Japan need not worry about bond vigilantes and the BOJ can set interest rates indefinitely at whatever level it chooses. If Abe wishes to increase inflation and nominal GDP, there is little doubt he could do so by expanding the government’s budget deficit. The economic significance of Prime Minister Abe’s appointment therefore lies more with his stance on fiscal policy, not monetary policy.

Since Abe previously held the Prime Minister position from September 2006 through September 2007, we have the good fortune of reviewing his fiscal policies during that time. According to Bloomberg, following that election:

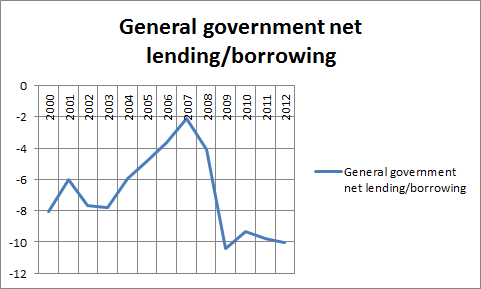

“The government [was] aiming to find as much as 90 percent of the money it needs to achieve a primary balance from spending cuts, with the rest coming from other measures such as higher taxes.”As the following chart shows, Abe’s previous leadership entailed the smallest budget deficit during the past 12 years, by a wide margin (Source: IMF):

Although Abe may be willing to accept short-term fiscal expansion this time around, his medium and long term views still seem focused on reducing public debt.

After 20-plus years of shifting debt from the private to public sector, the private sector is once again in position to drive growth and inflation higher. The ongoing struggle for policy makers is how to revive private demand for credit that has been lacking for so long (chart courtesy of The Economist):

Considering this background, the most likely outcome from Abe’s election is brief fiscal stimulus that is reversed once the economy begins to recover. As demographics continue to work against the Japanese economy, encouraging private credit demand will become even tougher. Whether or not the BOJ officially loses its independence, explicitly monetizes the budget deficit or targets NGDP, it will be of little consequence for medium-run inflation and economic growth if fiscal policy remains effectively the same.

No comments:

Post a Comment