Scott Sumner at TheMoneyIllusion suggests that Evan Soltas provides the best argument for NGDP targeting. After offering praise he provides a brief criticism regarding Evan’s interpretation of some graphs in a recent blog post:

Evan states:The first graph shows that even the most massive amounts of monetary expansion are ineffective medicine for NGDP expansion. What matters is expectations; growth in the medium run is conditional on expectations — not on the monetary base or price level.

The second graph shows the extent to which monetary policy seems to have forgotten this. Nominal income growth expectations have been right at zero since the recession, when before that they had been stable at the 5 percent level for decades. The findings come from this study by the Chicago FRB, which I found through this Chicago Magazine article. Paging Scott Sumner…Sumner replies:

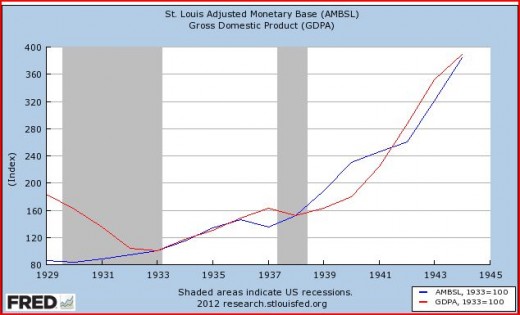

I mostly agree, and very much like the second graph, but I’d like to slightly quibble with the first graph. I redrew it setting both the base and NGDP equal to 100 in 1933, not 1929:

Notice that the base rose in the early 1930s while NGDP fell sharply. That’s because base demand was engorged by two factors, banking distress and ultra-low interest rates. The ultra-low interest rates continued between 1933 and 1944, but banking distress fell sharply after dollar devaluation and the creation of FDIC. Thus after 1933 the base and NGDP rose at roughly similar rates, both nearly quadrupling over those 11 years. As you know, I don’t regard the base as a reliable indicator of the stance of monetary policy, because base demand can be highly volatile under certain conditions. But the supply of base money is still very important; indeed it’s the major factor driving NGDP over the long term.

Judging this debate I’d actually like to argue that Evan may have the upper hand. Until the Great Recession, excess reserves in the financial system were maintained at a minimal level. As has been previously shown, demand for credit (loans) creates deposits. The Federal Reserve has primarily focused on targeting the price of reserves (interest rates), letting the quantity float by always providing a sufficient amount. The amount of base money should correlate reasonably well with the increasing demand for credit under these conditions. Steve Keen has shown in his models of the economy that changes in debt directly impact aggregate demand and thereby NGDP. One should therefore expect to see a positive correlation between NGDP and base money while those circumstances persist.

However, since the Great Recession the Fed has, to a degree, altered its approach to monetary policy by paying Interest-on-Reserves (IOR). Back in November of 2010 I blogged the Fed Stands in Own Way on Monetary Policy. In that post I highlighted a report from the New York Fed asking Why Are Banks Holding So Many Excess Reserves? As the authors’ note:

However, since the Great Recession the Fed has, to a degree, altered its approach to monetary policy by paying Interest-on-Reserves (IOR). Back in November of 2010 I blogged the Fed Stands in Own Way on Monetary Policy. In that post I highlighted a report from the New York Fed asking Why Are Banks Holding So Many Excess Reserves? As the authors’ note:

if the central bank pays interest on reserves at its target interest rate,..., the money multiplier completely disappears. In this case, banks never face an opportunity cost of holding reserves and, therefore, the multiplier process described above does not even start.Paying IOR above the risk-free-rate has resulted in a surge of excess reserves and base money uncorrelated with any increase in the demand for credit. Changing Fed policy has altered the conditions under which the previous relationship existed. The supply of base money (which was correlated but didn’t drive NGDP) may therefore no longer even show any material correlation with NGDP (as long as current condition prevail). Evan appears correct:

What matters is expectations; growth in the medium run is conditional on expectations -- not on the monetary base or price level.

There's only one reason to target nominal gDp, you can't forecast its components.

ReplyDelete"But the supply of base money is still very important; indeed it’s the major factor driving NGDP over the long term."

ReplyDeleteMilton Friedman's "monetary base" has never been, & is not now, a base for the expansion of new money & credit. GIGO

Monetary policy objectives should not be in terms of any particular rate or range of growth of any monetary aggregate. Rather, policy should be formulated in terms of desired rates-of-change (roc’s) in monetary flows (MVt) relative to roc’s in real GDP.

ReplyDeleteThere is evidence to prove that nominal-gDp can be used as a proxy figure for roc’s in all transactions. Roc’s in real GDP have to be used as a policy standard.

Because of monopoly elements, and other structural defects, which raise costs, and prices, unnecessarily, and inhibit downward price flexibility in our markets, the FOMC should follow a monetary policy which will permit the roc in monetary flows to exceed the roc in real GDP by c. 2-3 percentage points.

This is the root cause of Bubbles & Busts:

ReplyDeleteTo counter what Greenspan described as “irrational exuberance (at the height of the Doc.com stock market bubble), Greenspan initiated a "tight" monetary policy (for 31 out of 34 months). A “tight” money policy is defined as one where the rate-of-change in monetary flows (our means-of-payment money times its transactions rate of turnover) is no greater than 2-3% above the rate-of-change in the real output of goods & services.

Greenspan then wildly reversed his “tight” money policy (at that point Greenspan was well behind the employment curve), and reverted to a very "easy" monetary policy -- for 41 consecutive months (i.e., despite 17 raises in the FFR, -every single rate increase was “behind the curve”). I.e., Greenspan NEVER tightened monetary policy.

Then, as soon as Bernanke was appointed to the Chairman of the Federal Reserve, he initiated a "tight" money policy (ending the housing bubble in Feb 2006), for 29 consecutive months, or at first, sufficient to wring inflation out of the economy, but persisting until the economy plunged into a depression).

The FOMC continued to drain liquidity despite its 7 reductions in the FFR (which began on 9/18/07). I.e., despite Bear Sterns two hedge funds that collapsed on July 16, 2007, & immediately thereafter filed for bankruptcy protection on July 31, 2007 -- as they had lost nearly all of their value), the FED maintained its “tight” money policy (i.e., credit easing, not quantitative easing).

Note: Nominal gDp's 2 year rate-of-change (which equals what the FED can control -- i.e., MVt), peaked in the 2nd qtr of 2006 @ 12%. Bernanke let it fall to 8% by the 4th qtr of 2007 (or by 33%). It fell to 6% in the 3rd qtr of 2008 (another 25%). It then plummeted to a -2% in the 2nd qtr of 2009 (another [gasp] - 133%).

I.e., Bernanke didn’t initiate an “easy” money policy until Lehman Brothers later filed for bankruptcy protection (& it was one the Federal Reserve Bank of New York’s primary dealers in the Treasury Market), on September 15, 2008. The next day AIG’s stock dropped 60%.

By waiting to inject liquidity, risk aversion was amplified, haircuts were increased, additional and/or a higher quality of collateral was required, liquidity mismatches grew, funding sources dried up, long-term illiquid assets went on fire-sale, a counterparties’ creditworthiness was examined more carefully -- all of which lead to runs on financial companies.

I.e., Greenspan didn't start "easing" on January 3, 2000, when the FFR was first lowered by 1/2, to 6%. Greenspan didn't change from a "tight" monetary policy, to an "easier" monetary policy, until after 11 reductions in the FFR, ending just before the reduction on November 6, 2002 @ 1 & 1/4% (approximately coinciding with the bottom in equity prices).

I.e., Greenspan was responsible for both high employment (June 2003, @ 6.3%), & high inflation (rampant real-estate speculation, followed by widespread commodity speculation – peaking in July 2008 – Greenspan’s inflection point).

Bernanke then relentlessly drove the economy into the ground, creating a protracted un-employment, & under-employment rate, nightmare

Unfortunately the Federal Reserve doesn’t gauge the volume and timing of its open market operations in terms of the amount and desired rate of increase of member commercial banks COSTLESS legal reserves, but rather in terms of the levels of the federal funds rates (the interest rates banks charge other banks on excess balances with the Federal Reserve).

By using the wrong criteria (INTEREST RATES, rather than member bank reserves) in formulating and executing monetary policy, the Federal Reserve became the HOUSING bubble’s engine. I.e., the "administered or actual" prices would not be the "asked" prices, were they not “validated” by (MVt), i.e., “validated” by the world's Central Banks.

Targeting nominal gDp might be an improvement (but won’t work), because the FED’s technical staff doesn’t know how to hit it.

ReplyDeleteFor example even ex-post: “Although the evidence is mixed, the MSI (monetary services index), overall suggest that monetary policy WAS ACCOMMODATIVE before the financial crisis when judged in terms of liquidity. —Richard G. Anderson and Barry Jones.

Great comments Flow5. Very interesting insight and I largely agree with your take on the Fed's actions.

DeleteJust came across this old post - flow5 always makes me laugh. You see him pop up everywhere, always quality comments, but somewhat opaque and it's hard to discern a consistent thread running through them.

ReplyDeleteVery true. I had to read through all of his comments a few times to grasp the underlying perspective.

DeleteSeparately, thanks for sharing your thoughts and engaging in discussions the past several months. Hope you have a happy new year!