...is from Warren Mosler’s Soft Currency Economics II (Modern Monetary Theory):

the Fed must provide enough reserves to meet the known requirements, either through open market operations or through the discount window. If banks were left on their own to obtain more reserves no amount of interbank lending would be able to create the necessary reserves. Interbank lending changes the location of the reserves but the amount of reserves in the entire banking system remains the same. For example, suppose the total reserve requirement for the banking system was $ 60 billion at the close of business today but only $ 55 billion of reserves were held by the entire banking system. Unless the Fed provides the additional $ 5 billion in reserves, at least one bank will fail to meet its reserve requirement. The Federal Reserve is, and can only be, the follower, not the leader when it adjusts reserve balances in the banking system.

Bibliography

Mosler, Warren (2012-10-25). Soft Currency Economics II (Modern Monetary Theory) (Kindle Locations 367-373). . Kindle Edition.

Earlier this week I discussed the dangers of misunderstanding “helicopter money” and higher inflation targets. A focus of that post was the incentives stemming from negative real interest rates that will lead to greater investment in real assets, not businesses. The obvious implication is that negative real interest rates entail significant risk of spurring asset bubbles.

This discussion of asset bubbles comes on the heels of St. Louis Federal Reserve Governor Jeremy Stein’s speech that suggested the Fed was becoming increasingly concerned about bubbles, not inflation. According to a recent Bloomberg article, apparently Fed Chairman Bernanke was not onboard with the supposed shift (h/t Tim Duy):

Federal Reserve Chairman Ben S. Bernanke minimized concerns that the central bank’s easy monetary policy has spawned economically-risky asset bubbles in comments at a meeting with dealers and investors this month, according to three people with knowledge of the discussions.

Do Bernanke’s comments imply the change Stein alluded to is not really happening? Not necessarily. To understand why, one must consider the goals assigned to Bernanke or any Fed Chairman for that matter. The following is from Chapter 2 of the Federal Reserve System’s own publication, Purposes & Functions:

The goals of monetary policy are spelled out in the Federal Reserve Act, which specifies that the Board of Governors and the Federal Open Market Committee should seek “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

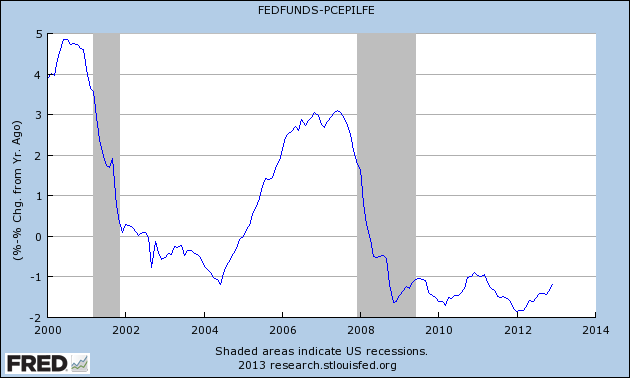

Although no explicit mention of preventing asset bubbles is made, the goal of stable prices leaves the door open for such an interpretation. Before addressing the Fed’s own interpretation of stable prices, its worth discussing the specific types of assets that are seemingly most prone to bubbles. The three major categories are commodities (e.g. oil, copper, sugar), financial assets (e.g. stocks and bonds), and housing. During the past decade real interest rates have actually been negative more often than not (Real Interest Rate = Effective Fed Funds rate - core PCE):

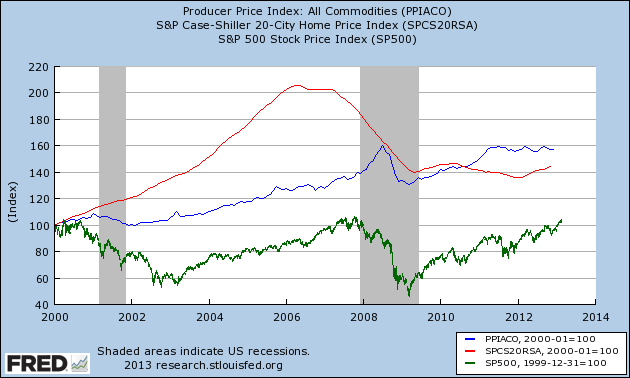

Unsurprisingly the past decade has also witnessed asset bubbles in commodities, stocks and housing:

Prices of these assets have clearly been anything but stable. So has the Fed failed in that aspect of its mandate? The answer is a resounding “NO.”

To remedy the cognitive dissonance readers may be experiencing, consider how the aforementioned real assets affect the FOMC’s preferred inflation measure, core Personal Consumption Expenditures (PCE). Financial assets are noteworthy in their distinct omission from the type of products making up PCE. Commodities are included in the general price measure, however core PCE is calculated by excluding a couple of the more volatile commodity components: food and energy. Housing is actually included in core PCE but is calculated using the space rent of nonfarm owner-occupied homes, not actual house prices. Focusing on core PCE thereby removes any direct concern with asset bubbles.

Bernanke has already announced his plans to step down as Fed Chairman early next year (2014). Given the Fed’s stated mandate and preferred measure of prices, it is no wonder that Bernanke is unconcerned with asset bubbles. The goals of his chair are to maximize employment and maintain stable prices. Since the types of assets prone to bubbling are not included in core PCE and appear relatively uncorrelated with that measure, to the degree that bubbles can benefit employment in the short run, they may actually be desirable.*

These institutional incentives of a Fed Chairman are unfortunately at odds with the country’s longer term economic goals. Asset bubbles created by excessive lending and/or negative real interest rates are always followed by busts. These busts are simply the recognition of malinvestment that already took place during the boom. If the booms are financed with significant leverage, the resulting deleveraging may lead to a debt deflationary spiral. Whether or not that’s the case, though it usually is, malinvestment suppresses both employment and economic growth over time.

One can argue over whether Bernanke’s views on the effectiveness of monetary policy are correct or not, but his decision to ignore asset bubbles is perfectly rational given the circumstances. Shifting the Fed’s focus from inflation to bubbles will therefore require changing the institutional incentives.

*The three major asset categories mentioned above presumably will have very different effects on employment. Among the three, commodity bubbles are least desirable from an employment perspective. Higher commodity prices generally hurt consumer spending, which may lead to a temporary decline in employment. Housing bubbles are the most desirable in these terms since the increased demand can generate a temporary employment boom in construction and housing-related services.

Rational nerdiness vs macho bada$$ery in monetary policy by Cardiff Garcia @ FT Alphaville

The US economy has had several false starts since 2009, and it’s likely that several tangled factors were responsible for their not lasting longer. It’s reasonable to think that one of these factors was that the initial reflationary effects of these unconventional measures faded, because of doubts about the Fed’s commitment to maintaining accomodative policy during a period of catch-up growth. If such growth threatened to generate above-target inflation, then monetary conditions could be expected to tighten.

The rational-nerdy thing to do was to soften the macho commitment to inflation and commit to a temporary period of inflation-tolerance, thereby balancing the two sides of the mandate — but to do so while retaining credibility on both. But as Harless notes, ceding a little ground on one side could be interpreted as ceding all ground. Being a “macho badass” central banker means credibly committing to never cede ground.

…

All of which has been a long windup to saying that the appeal of the Evans Rule, and if we ever get it, some variation of NGDP level targeting, is this: they institutionalise the macho badassery, which in a dual-mandate framework can only be applied to one of the two mandates.

Woj’s Thoughts - This post is reminiscent of a thread from last year involving Steve Roth and Ryan Avent on The Asymmetric Nature of Monetary Policy. In that post I made the following claim:

Whereas Roth suggests that asymmetric credibility stems from the Fed’s actions, I believe it is actually an inherent condition in our current monetary system. The Fed sets the base price for money and credit, but with private banks free to create credit, it holds relatively little control over the total amount outstanding at any time. As growth in the US has exceeded inflation for much of the past three decades, the conditions were ripe for borrowing and credit outstanding now greatly surpasses the sum of base money.

Even if the Fed promised indefinite QE, it’s hard to see the mechanism, aside from adjusting inflation expectations (wealth effects are minimal), by which this would spur real growth. Given the Fed’s skewed abilities and determination to maintain its credibility, it seems more obvious why inflation targeting remains prominent. Further, this may help explain why the Fed downplays its employment mandate (which should be removed anyways). Facing the endgame, the Fed knows it can reduce inflation (and growth) but remains unsure how successful it could be at achieving other targets.

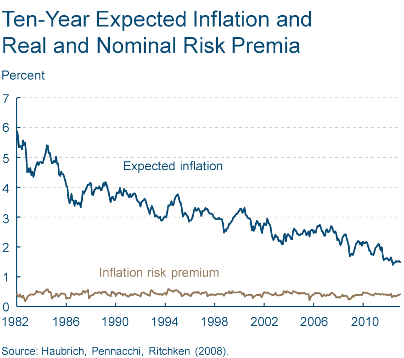

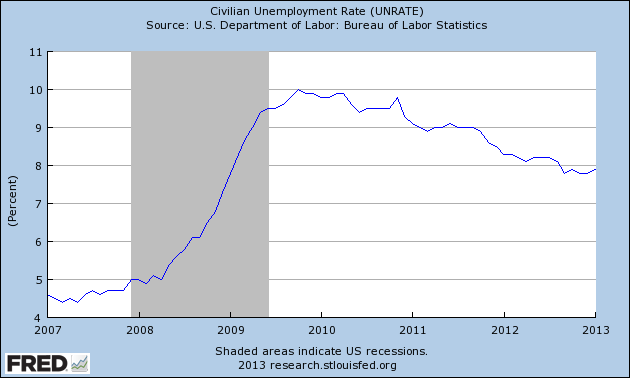

Sucumbing to pressure, the Fed has finally decided to cede ground on its commitment to inflation. Unfortunately for the Fed, both inflation expectations and unemployment are not cooperating:

At this point I doubt whether even altering inflation expectations would provide any boost to actual inflation or employment. If fiscal policy continues to contract the budget deficit, these numbers will continue moving in the wrong direction. The Fed has taken a big risk with its established credibility. I fear the results will be very disappointing.

Last year I took a chance and threw my own projections into the ring. Similar to Byron Wien and Edward Harrison, I mostly selected events that were widely seen as having a low probability (less than 33%) but which I believed held a greater than 50% chance of occurring. The final results were a bit disappointing, but that won’t stop me from trying again this year. Since these predictions already represent a late release, without further adieu, here are the 2013 predictions:

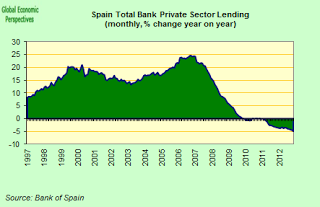

1) Spain requests access to ECB’s OMT - Since ECB President Mario Draghi announced the OMT program, yields on Spanish debt have fallen rather dramatically. Although this eases financing pressure, it has done little to alter the actual economy’s downward spiral. During 2012 Spain’s GDP growth became increasingly negative, falling by 1.8% year-on-year in the fourth quarter. Meanwhile unemployment continues its meteoric rise to over 26% for the general population and nearly 60% for youth. With the large banks still severely undercapitalized and households over-indebted, private sector lending continues to decline:

Seeing no recovery and potentially a worsening decline, “bond vigilantes” will eventually test Draghi’s threat. At that point Spain will be forced to accept a Memorandum of Understanding (MoU) in return for ECB bond-buying through the OMT program.

2) The Euro finishes the year above $1.30 - After falling nearly 10% during the first half of 2012, the euro has more than recouped its losses on the back of optimism and deflationary policies.

At points during 2013 the optimism is likely to fade, but I expect politicians and central bankers will take the necessary steps to quell fears for the time being. Unfortunately those steps will involve further deflationary policies that push the euro higher. These competing forces will largely cancel out, leaving the euro close to or above where it began the year.

3) The Eurozone remains in recession the entire year - Forecasters now expect euro-zone economic activity to be flat this year, down from a previous prediction of 0.3% growth made just three months ago. Last year saw practically continuous downgrades to GDP growth forecasts and I expect this year to be no different. Austerity measures are momentarily easing, but more will likely be enacted based on the outcomes of several elections. The recent appreciation of the euro against several major currencies will also dampen growth by putting pressure on net exports. With banks across Europe trying to build up capital and persistently high unemployment, the private sector will remain especially weak. Though Germany may experience a temporary rebound, the Eurozone as a whole will not register GDP growth this year.

4) The Japanese yen rises above 90 per $ - Since the election of PM Shinzo Abe, the yen has fallen fast and is down more than 20% from recent highs.

During this time the Nikkei has risen more than 20%, yet yields on Japanese sovereign debt are little changed. This suggests many foreigners may be speculating on the supposedly forthcoming monetary and fiscal stimulus. As previously stated, the fiscal stimulus will probably be small and short-term. On the monetary front, short of actually entering the foreign exchange market, the Bank of Japan (BOJ) has essentially no mechanism to spur inflation and thereby cause a sustained depreciation of the yen. When market participants recognize the inability of Japan to avoid continued deflation, the yen will return to appreciating against the dollar.

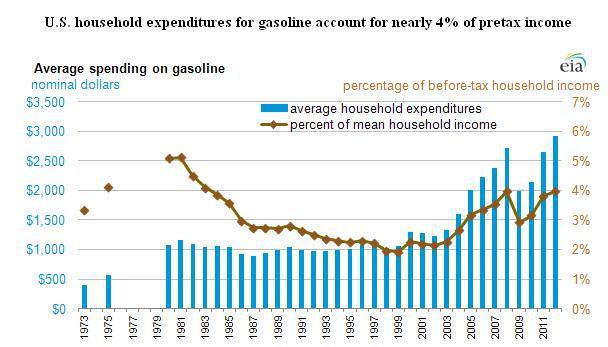

5) Gas prices will peak above $4.20 per gallon and set a new yearly record-high average above $3.75 per gallon - Gasoline prices have been on the rise for the past 31 days, currently averaging approximately $3.75 per gallon. Though this current streak will probably end soon, prices are unlikely to give back much of the gains before beginning the typical rise into summer. The ongoing potential for flare ups in the Middle East will keep prices elevated throughout the year. Higher gas prices, which already account for 4% of before-tax household income (chart below), will be a drag on consumer spending in 2013.

6) U.S. Yearly GDP growth falls below 1.5% - Forecasts of ~3% annual GDP growth over the past couple years have been overly optimistic as real growth in 2011 and 2012 was merely 1.6% and 1.9%, respectively. Apparently forecasters are being a bit tamer in their estimates this year, now expecting only 2% annual growth. Unfortunately I suspect these estimates will once again prove too optimistic. Various tax hikes and the upcoming sequester (which will go through in some respect) will reduce the budget deficit by a few percent this year. Housing is likely to remain a bright spot, but further declines in interest rates will not lead to similar magnitudes of the wealth effect. Credit remains tight for many households and small business, which should also limit private sector activity. All of these factors combined will probably not be enough to bring about a new recession but will lead to the lowest annual growth rate during this upswing.

7) U.S. Unemployment rises above 8% - Currently sitting at 7.9%, the unemployment rate is forecast to decline during 2013. Due to weaker GDP growth, corporate revenues will barely rise again this year. As companies face increasing pressure to maintain profit margins at record levels, a new wave of layoffs may occur. Separately, continuing economic growth will encourage previously discouraged workers to re-enter the job market. Both of these factors will lead to slightly higher measured unemployment.

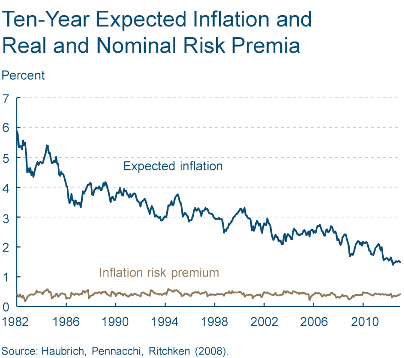

8) Federal Reserve forecasts shift first rate hike to 2016 - After extending their forecast for the first rate hike to 2015, the Federal Reserve changed its tactics to a more rule-based monetary policy. The Fed has, in effect, promised to keep rates low until we've hit either 6.5 percent unemployment or 2.5 percent inflation. Based on the above outlook for unemployment and a continuing decline in inflation expectations (chart below), FOMC members will revise their own forecasts and push back expectations for the first rate hike.

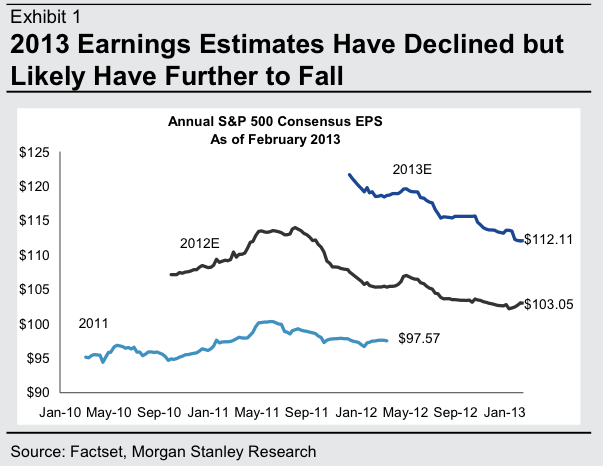

9) U.S. Corporate Earnings (ex-Federal Reserve) finish year below 2012 peak - Meager revenue growth was not enough to prevent U.S. Corporate Profits after tax from reaching record highs in the fourth quarter of 2012 on the back of record profit margins.  As global growth slows in 2013, revenues will come under further pressure. At this point the ability of firms to continue cutting costs without sacrificing output seems limited, which means margins may begin to compress. As margins revert to previous norms, earnings will register a yearly decline.

As global growth slows in 2013, revenues will come under further pressure. At this point the ability of firms to continue cutting costs without sacrificing output seems limited, which means margins may begin to compress. As margins revert to previous norms, earnings will register a yearly decline.

10) Bonds outperform stocks - During the first seven weeks of this year the stock market has been on fire, even though earnings estimates continue to fall.

Multiple expansion is currently being driven by the Federal Reserve’s actions despite their ineffectiveness at generating actual NGDP growth. When investors eventually turn their attention to continuing troubles in Europe, ongoing deflation in Japan, and/or weakening growth in China, U.S. earnings may once again enter the picture. Recognition that S&P 500 earnings growth has slowed substantially may cause the market to give up much of this year’s gain. These concerns combined with declining inflation expectations will result in many investors returning to the safety of U.S. Treasuries. The subsequent rise in prices (decline in rates) will generate another year of positive returns for the Treasury market.

Will my predictions prove too pessimistic once again? Only time will tell...

Ashwin Parameswaran has a fantastic post today explaining why Helicopter Money Is Not Dangerous, All Macroeconomic Policy Is Dangerous “in the sense that irresponsible implementation can lead to macroeconomic chaos.” Before jumping into the main attraction of the post, I want to briefly clarify a general discrepancy regarding what helicopter money actually entails.

More than forty years ago, Milton Friedman famously quipped that price deflation can be fought by "dropping money out of a helicopter."[37] Friedman was referring to central bank policy and, to this day, a “helicopter drop” is typically associated with monetary policies, such as quantitative easing (QE). This is an unfortunate interpretation of monetary policy since most central banks, including the Federal Reserve, are as equally unable to actually implement a “helicopter drop” today as they were back in 1969. Willem Buiter clarifies how the policy could realistically be implemented in a paper on “Helicopter Money” (equations omitted):

Technically, if the Central Bank could make transfer payments to the private sector, the entire (real-time) Friedmanian helicopter money drop could be implemented by the Central Bank without Treasury assistance.

…

The legality of such an implementation of the helicopter drop of money by the Central Bank on its own would be doubtful in most countries with clearly drawn boundaries between the Central Bank and the Treasury. The Central Bank would be undertaking an overtly fiscal act, something which is normally the exclusive province of the Treasury.47

An economically equivalent (albeit less entertaining) implementation of the helicopter drop of money would be a tax cut (or a transfer payment) implemented by the Treasury, financed through the sale of Treasury debt to the Central Bank, which would then monetise the transaction. If the direct sale of Treasury debt to the Central Bank (or direct Central Bank lending to the Treasury) is prohibited (as it is for the countries that belong to the Euro area), the monetisation of the tax cut could be accomplished by the Treasury financing the tax through the sale of Treasury debt to the domestic private sector (or overseas), with the Central Bank purchasing that same amount of non-monetary interest bearing debt in the secondary market, thus expanding the base money supply. (2004: p. 59-60)

One might inquire whether changing to a “permanent floor” monetary policy regime alters the necessity of monetisation. Apparently prepared for such a future outcome, Buiter says:

This difference between the effects of monetising a government deficit and financing it by issuing non-monetary debt persists even if the interest rates on base money and on non-monetary debt are the same (say zero), now and in the future. When both money and bonds bear a zero nominal interest rate, there remains a key difference between them: the principal of the bonds is redeemable, the principal of base money is not. (2004: p. 10)

Although monetisation may be necessary to achieve the full effect of “helicopter money,” this practice does not alter the dangers associated with the Treasury’s actions. As Ashwin points out:

Whether they are monetised or not, excessive fiscal deficits are inflationary.

On the topic of inflation, I have recently been engaging in a debate with Mike Sax (see here and here) about the potential benefits of targeting a higher inflation rate. This policy has garnered support from both sides of the political and economic aisle (New Keynesians and Monetarists), yet I think its potential benefits are being extremely oversold. My two basic arguments against such a policy are the following:

1) Higher inflation does not necessarily entail higher nominal wages (which many people clearly assume).

Aside from the top quintile of households, real income has been declining for nearly 15 years. The only way higher inflation helps reduce real debt burdens is if nominal wages increase faster than nominal interest rates on debt. If instead higher inflation stems primarily from higher costs-of living (nominal food and energy prices), than most Americans may find themselves in the precarious position of requiring even more debt to maintain current living standards.

2) Higher inflation alters saving, investment and consumption decisions which can lead to a misallocation of capital. On this second point is where Ashwin’s post really hits home:

During most significant hyperinflations throughout history, the catastrophic phase where money loses all value has been triggered by the central bank’s enforcement of highly negative real interest rates which encourages the rich and the well-connected to borrow at negative real rates and invest in real assets. The most famous example was the Weimar hyperinflation in Germany in the 1920s during which the central bank allowed banks and industrialists to borrow from it at as low an interest rate of 5% when inflation was well above 100%. The same phenomenon repeated itself during the hyperinflation in Zimbabwe during the last decade (For details on both, see my post ‘Hyperinflation, Deficits and Real Interest Rates’).

This also highlights the danger in simply enforcing a higher inflation target without taking the level of real interest rates into account. For example, if the Bank of England decided to target an inflation rate of 6% with the bank rates remaining at 0.50%, the risk of an inflationary spiral will increase dramatically as more and more private actors are tempted to borrow at a negative real rate and invest in real assets. Large negative real rates rarely incentivise those with access to cheap borrowing to invest in businesses. After all, why bother with building a business when borrowing and buying a house can make you rich? Moreover, just as was the case during the Weimar hyperinflation, it is only the rich and the well-connected crony capitalists and banks who benefit during such an episode. If the “danger” from macroeconomic policy is defined as the possibility of a rapid and spiralling loss of value in money, then negative real rates are far more dangerous than helicopter money.

These pernicious traits of higher inflation and especially negative real interest rates are entirely compatible with recent experience. Households and businesses “with access to cheap borrowing” have been pouring money into stock, bond, housing and commodity markets rather than investing in tangible capital. The remarkable rise in asset prices has unfortunately not funneled down to households in the bottom four quintiles of income and wealth, only furthering the inequality gap. Recognition of these effects is precisely why a Federal Reserve fearing bubbles, not inflation, would be a significant step in the right direction.

To be clear, similar to Ashwin, I am in favor of “helicopter money” and believe higher wages for the bottom 80 percent are key to ending the balance sheet recession as well as ensuring more sustainable growth and unemployment going forward. Targeting higher inflation and larger negative real interest rates is the wrong approach to achieve these goals and may actually work in the opposite direction. Yes, all macroeconomic policy is dangerous. But even more dangerous is misunderstood and misrepresented macroeconomic policy.

Bibliography

Buiter, Willem H., Helicopter Money: Irredeemable Fiat Money and the Liquidity Trap (December 2003). NBER Working Paper No. w10163. Available at SSRN: http://ssrn.com/abstract=478673