Carola Binder was struck by the historical relevance of the chosen terminology and offered the following comment in a post on Overheating and the Fed:

In the New York Times, Binyamin Applebaum writes that Stein's speech "underscored that the Fed increasingly regards bubbles, rather than inflation, as the most likely negative consequence of its efforts to reduce unemployment by stimulating growth." In fact, the Fed's concern about bubbles is not so new. After the Great Depression, it was widely believed that the stock market overheated in the 1920s, leading to the Great Crash in 1929 and the onset of the Depression. In those days, the word for bubbles or overheating was speculation, and it became a dirty word indeed. After the Great Depression, speculation remained a major concern of the Fed. The Fed very explicitly regarded bubbles as the most likely negative consequence of its efforts to reduce unemployment by stimulating growth.Apparently the Fed has come full circle. Carola goes on to provide a couple excerpts from FOMC minutes during the 1950’s, the last time the Federal Reserve was concerned with asset bubbles instead of inflation. The subsequent change in thought is not overly surprising given that stock markets flatlined starting in the mid-1960’s, as inflation picked up and became a major cause for concern throughout the 1970’s. What is disturbing, is the Federal Reserve’s failure to recognize the changing landscape over the past three decades.

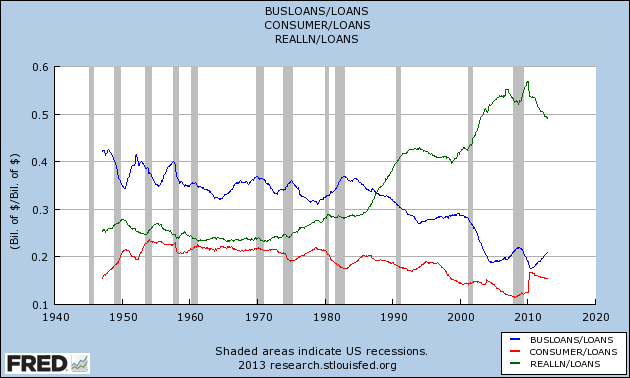

During that time, commercial bank lending has largely shifted its priorities from financing tangible (capital) investment through business loans to financing the purchase of already existing assets (e.g. houses, stocks and bonds):

(BUSLOANS = Commercial and Industrial Loans; REALLN = Real Estate Loans; LOANS = Loans and Leases at All Commercial Banks)

It should therefore come as no surprise that the transmission mechanism of monetary policy is now primarily through various asset markets (i.e. real estate monetary standard).

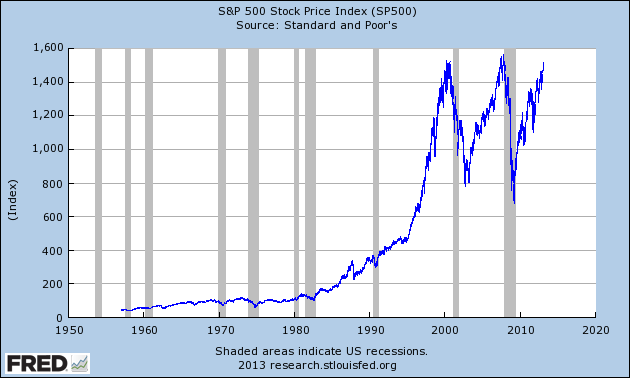

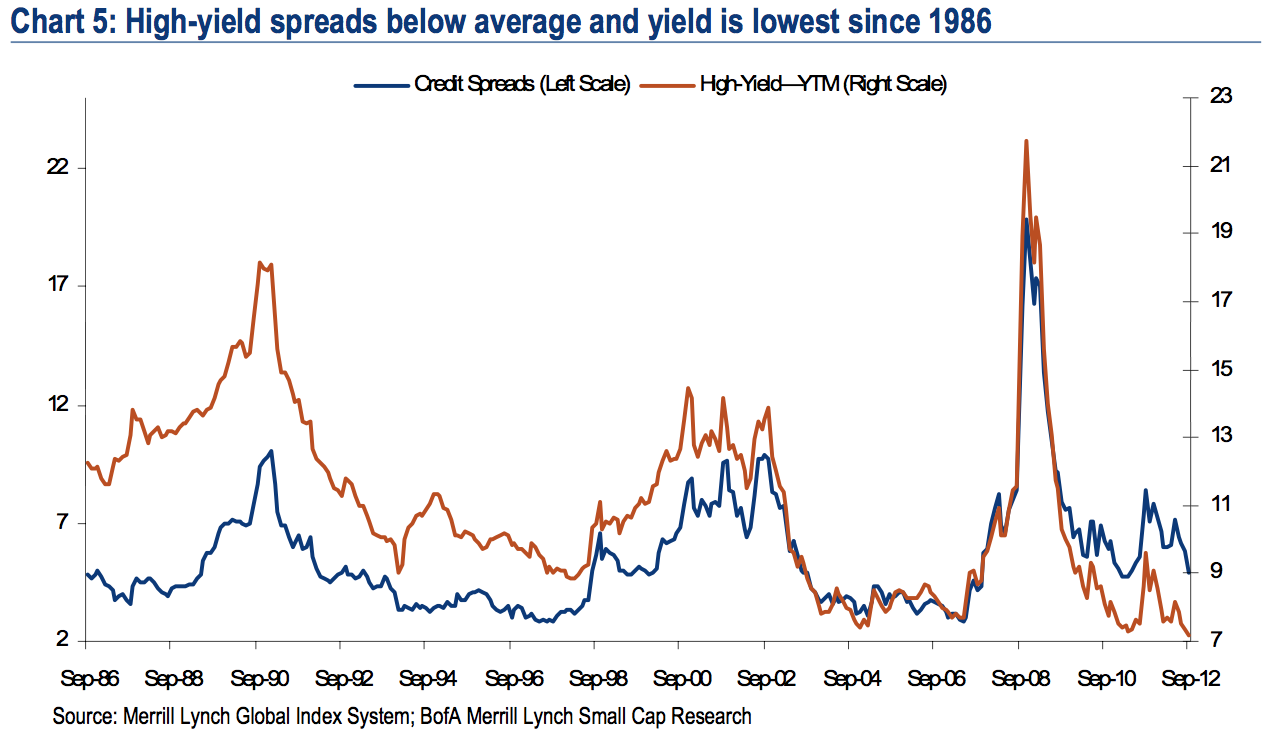

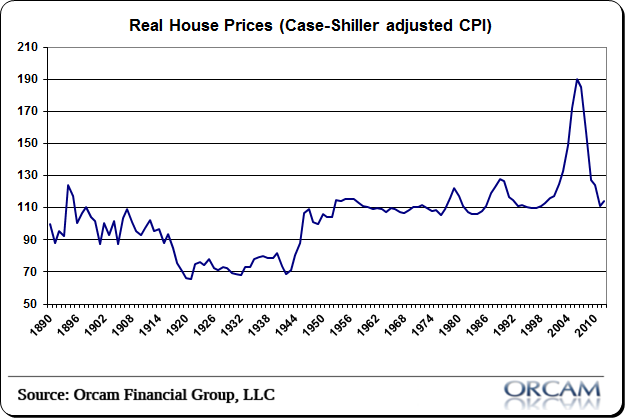

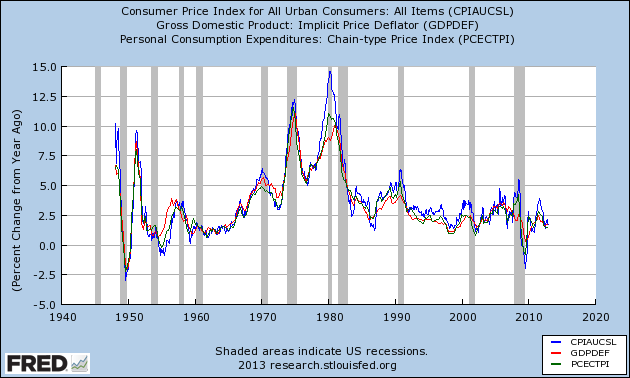

Consider the following charts showing various asset prices and inflation rates during the past 30 years:

Stocks:

High-Yield Corporate Debt:

Houses:

Inflation:

Over the past few years I’ve been very critical of the Federal Reserve’s actions spanning the last couple decades. One of the primary reasons behind this view was the incessant focus on limiting inflation and utter lack of concern regarding asset bubbles. The present risk of a zero interest rate policy (ZIRP) and QEternity lies mainly in inflating new asset bubbles, not creating excessive measured inflation. If the Fed has finally come back around to this realization, that would certainly be a big step in the right direction.

No comments:

Post a Comment