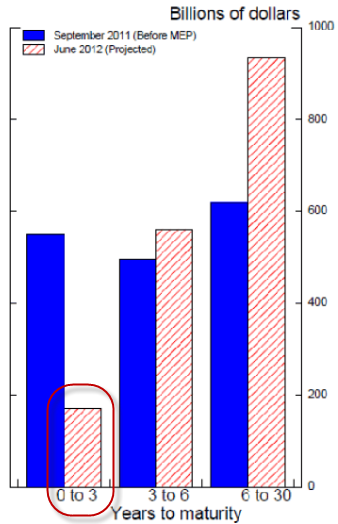

The Committee also decided to continue through the end of the year its program to extend the average maturity of its holdings of securities. Specifically, the Committee intends to purchase Treasury securities with remaining maturities of 6 years to 30 years at the current pace and to sell or redeem an equal amount of Treasury securities with remaining maturities of approximately 3 years or less. This continuation of the maturity extension program should put downward pressure on longer-term interest rates and help to make broader financial conditions more accommodative.As many forecasters predicted, the Fed is extending Operation Twist through the end of the year. Omitted from this statement is the specific size of the program, which was $400 billion for the previous round. One reason for this omission may be the limited remaining supply of short-term Treasury securities. Highlighting this topic in a recent post, Sober Look noted that:

BofA is projecting that by the time of the FOMC meeting this month, the Fed will have $175bn of short-term treasuries on its balance sheet.If these projections from BofA represent a valid approximation, the Fed will be unable to maintain the current pace of operations for the next six months. To comply with their statement, the Fed would therefore either have to lower the current pace, shorten the time span, or increase the maturity of securities being sold.

Regardless of the which option the Fed chooses, the effects of this program will be minimal, at best. As Gary Becker recently pointed out:

The Fed in what is called “Operation Twist” could try to further lower long term interest rates relative to the negligible rate on treasury bills by buying long term bonds. This might reduce further the spread in interest rates (that is, flatten the interest yield curve), but this effect is limited by a fundamental economic equilibrium condition. Long term interest rates tend to be an average of current and expected short term rates since more investors would shift into short term rates when long term rates are below this average; conversely, investors shift into long term rates when these are above the average of current and expected future short term rates.With yields on 30-year Treasuries already below 3% (currently ~2.75%), it’s hard to envision much of an incremental gain from another 25-50 basis point reduction. Asset (primarily equity) markets may rally on this news, but the short-term wealth effects are proven to have little carry over to real economic variables.

Even if we accept some minor benefits from the reduction in yields and rise in asset prices, those benefits are largely offset by the reduction in interest income to the private sector. This aspect of Operation Twist is often overlooked but equally important to understanding its impact on the real economy. By swapping short-term Treasury securities for longer-term issues, the Fed is not only increasing the duration of its portfolio but also the yield. This means that the Fed will collect a greater amount of interest income which otherwise would have been accrued by the private sector. In this manner, it’s certainly possible that Operation Twist could have the unintended effect of reducing aggregate demand.

Lastly, the FOMC’s decision to extend Operation Twist for the remainder of the year suggests that the Fed will not enact another round of balance sheet expansion (QE) until after the election. This may disappoint many investors who were expecting that “stimulus” to provide support for equity markets. Since the Great Recession began, the Fed has waited for the completion of each unconventional measure before electing to engage in further actions. Unless Europe or equity markets start to really unravel, I doubt the Fed will alter this typical progression right before a Presidential election.

Overall, the Fed’s new actions should once again have minimal effect on real economic growth or unemployment. With further action now on hold through the election, it will be interesting to see how markets hold up.

No comments:

Post a Comment