Earlier this week the U.S. dollar nearly reached a new all-time low against the Japanese yen. Unable to hold out any longer, the Bank of Japan (BOJ) intervened in the currency markets, buying dollars and selling yen. Except for during recent recessions, the dollar’s exchange value has been falling against most other major currencies for the past decade. Effects of and reasons for currency devaluation are frequently misunderstood and therefore it’s imperative to shed light on the fluctuating valuations.

When discussing money and currency, an initial point to highlight comes from The Theory of Money and Credit by Ludwig von Mises. Mises notes that fiat currency has no value apart from acting as a means of exchanging goods. A currency exchange rate, at its most fundamental level, is therefore merely the reflection of differing monetary values of goods between nations. Attempting to quantify rates of exchange between nations, economics created a purchasing power parity (PPP) exchange rate.

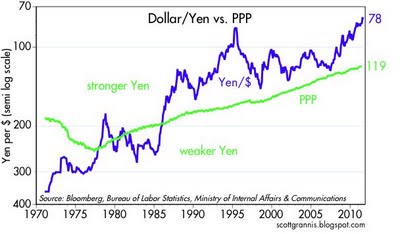

Understanding the rise of the yen, by Scott Grannis of Calafia Beach Pundit, highlights the diverging dollar/yen exchange rate from a theoretical PPP (shown below).

When discussing money and currency, an initial point to highlight comes from The Theory of Money and Credit by Ludwig von Mises. Mises notes that fiat currency has no value apart from acting as a means of exchanging goods. A currency exchange rate, at its most fundamental level, is therefore merely the reflection of differing monetary values of goods between nations. Attempting to quantify rates of exchange between nations, economics created a purchasing power parity (PPP) exchange rate.

Understanding the rise of the yen, by Scott Grannis of Calafia Beach Pundit, highlights the diverging dollar/yen exchange rate from a theoretical PPP (shown below).

At first glance one notices that the yen is approaching levels of significant historical and relative strength. However, before addressing the yen’s strength, some discussion is necessary to explain the PPP’s longstanding upward trend.

Inflation and deflation represent basic concepts for expressing price changes over time. The U.S. experienced high inflation during the 1970’s. After moderating significantly in the early 1980’s, inflation has been fluctuating around 2-3% ever since. Due to inflation, more dollars are required today when purchasing similar goods. Japan’s inflation rate was not nearly as high in the late 70’s and over the past two decades has been effectively nil. Recent deflation means Japanese consumers actually requires less yen to purchase similar goods than ten years ago. A rising PPP therefore reflects today’s need for fewer yen and more dollars to purchase similar goods compared to several decades ago..

Recognizing that changes in PPP have been relatively small and consistent, one might question the more sizable variations in market exchange rates between these currencies. Simply put, short-term movements likely reflect changing opinions about each nation’s future inflation. Displayed clearly above, similar to other financial markets, opinions are volatile but tend to fluctuate around an underlying equilibrium. Today’s stronger yen therefore depicts a belief that future U.S. inflation will be significantly greater than inflation in Japan.

Japan has been mired with slight deflation for the past decade, despite record low interest rates. Monetary experimentation and occasional fiscal stimulus have been unsuccessful to date. Although other stimulative options exist, desire for such policies appears weak, leaving the current status quo as the most probable outcome. Given Japan’s unchanging outlook, recent changes in the exchange rate appear more indicative of updated opinions on future U.S. inflation. Fearing deflation, the Federal Reserve has already embarked on two exercises in quantitative easing, with potential for a third looming. Operationally these measures were merely an asset swap between the Fed and banks aimed at lowering interest rates and increasing asset prices. However, market participants largely believe quantitative easing is a form of printing money that will eventually lead to surging inflation. Expectations of further quantitative easing may therefore account for continued weakening of the dollar.

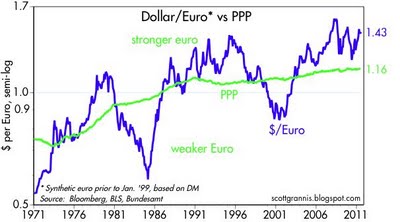

Along similar lines, I’ve recognized an interesting dichotomy in market opinion with regards to quantitative easing. As previously noted, the Fed’s decision to purchase large quantities of treasury notes has seemingly led increasing inflation expectations and a weakening dollar. Just yesterday, on the other side of the Atlantic, the European Central Bank (ECB) announced it would intervene in debt markets by buying Italian and Spanish sovereign debt. Over the past 18 months, the ECB has made numerous announcements involving their purchase of European sovereign debt. Oddly, these announcements are typically met with a strengthening euro. Below is a graph depicting the dollar/euro exchange rate against a comparable PPP.

Although the dollar/euro exchange rate has experienced wide swings, the PPP has remained fairly constant over the past two decades. Personally, the current euro strength is surprising in the face of ECB intervention and a rapidly deteriorating sovereign debt crisis. Yet considering both market valuations, the most apparent conclusion is that market participants expect much higher relative inflation in the U.S. going forward.

Anytime the market’s prevailing opinion distinctly contradicts your own, a potential investment opportunity arises. Congress’ recent decision to take up austerity measures will likely weaken the economy, causing disinflation. Even if the Fed embarks on a third, similar, round of quantitative easing, the short-term inflationary aspects of rising energy and food prices will create deflationary pressures over a longer period. Regardless of S&P’s U.S credit rating downgrade, the dollar should remain the world’s reserve currency for at least another decade, retaining its safe-haven status in especially uncertain times. Given this outlook, I expect the dollar/yen and dollar/euro to move back towards their PPP over the next few years.

(Note: I tend to disagree with Scott Grannis’ economic and political outlook, especially the last paragraph in the attached blog. However, Grannis often provides interesting data points and graphs making his blog a worthwhile opposing perspective.)

I have been trying to know why the dollar rate is rising and why is the rupee value falling? When will all these get over and India will have a better economy? Please share your ideas with me if you are aware of it.

ReplyDeleteAs India's economy continues to struggle, markets are expecting further rate cuts from the Indian central bank. The reduced spread between US and Indian rates is putting downward pressure on the rupee versus the dollar. I'm no expert on India's economy, but exports are clearly going to struggle with China and Europe faltering. Domestic consumption is probably unable to make up the slack, which means the government would have to spend more to try and sustain growth. That is not a long-term solution unfortunately. I wish I could offer more on when the economy will turn around but I simply don't know enough to say.

Delete