I’ve been thinking a lot about this over last few weeks when I have the chance to think. It seems like we are on a real estate monetary standard. Much like how we can use assets like gold to create a commodity money system, it seems like we operate our current monetary system as a real estate standard.

Banks create money against real estate assets. We use this money in our day-to-day transactions, without much thought about what stands behind this money, but most loans are for residential and commercial real estate.

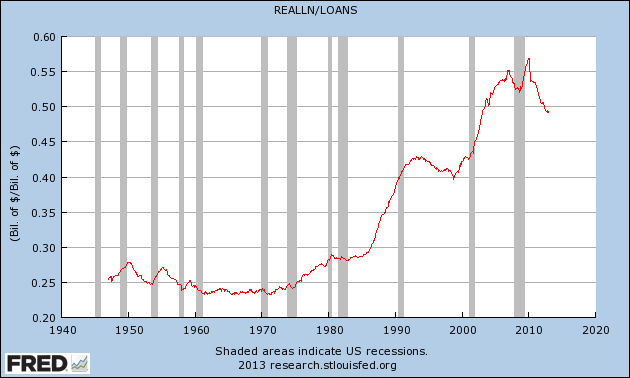

If we did operate under a real estate standard, we would expect to see the larger economic business cycle greatly impacted by the real estate cycle, far more than the declines in real estate activity would predict.The impetus for this discussion is a recent paper by Ed Leamer, “Housing is the Business Cycle,” that confirms Mike’s prediction. The following graph shows real estate loans at all commercial banks as a percentage of total loans and leases:

Notice that the percentage held relatively steady around 25 percent for nearly 40 years following the end of WWII. Then, in the mid-1980’s, the percentage surged higher. This massive change may have been a consequence of the Tax Reform Act of 1986 that included “ increasing the Home Mortgage Interest Deduction,” a “Low-Income Housing Tax Credit,” and changes to “ the treatment of imputed rent, local property taxes, and mortgage interest payments to favor homeownership.” After leveling off in the mid-1990’s, the percentage of real estate loans once again spiked higher beginning in late 1998. Once again, changes in tax policy may have played a substantial role. The Taxpayer Relief Act of 1997 substantially lowered the capital gains rate and “exempted from taxation the profits on the sale of a personal residence of up to $500,000 for married couples filing jointly and $250,000 for singles.”

Notice that the percentage held relatively steady around 25 percent for nearly 40 years following the end of WWII. Then, in the mid-1980’s, the percentage surged higher. This massive change may have been a consequence of the Tax Reform Act of 1986 that included “ increasing the Home Mortgage Interest Deduction,” a “Low-Income Housing Tax Credit,” and changes to “ the treatment of imputed rent, local property taxes, and mortgage interest payments to favor homeownership.” After leveling off in the mid-1990’s, the percentage of real estate loans once again spiked higher beginning in late 1998. Once again, changes in tax policy may have played a substantial role. The Taxpayer Relief Act of 1997 substantially lowered the capital gains rate and “exempted from taxation the profits on the sale of a personal residence of up to $500,000 for married couples filing jointly and $250,000 for singles.” The shifting of bank lending from primarily commercial to real estate loans has clearly been accompanied by shifts in policy to vastly reduce taxes accompanying rents, interest and capital gains. These changes, as well as other public policy initiatives, have helped significantly increase the value of homes that could be borrowed against. As Michael Hudson argues in The Bubble and Beyond, the overall effect has been to transfer former tax payments to private financial institutions, ultimately increasing wealth inequality and making the economy (and government) more beholden to the banks.

Although total real estate loans have actually fallen during the past few years, they still account for nearly 50 percent of total loans. This real estate monetary standard is certainly not restricted to the U.S. and actually appears to be prominent in Europe, as well as several other developed nations. To the degree that bank lending affects aggregate demand, real estate will clearly continue to have an outsized effect on the global business cycle.

(Note: For those interested, Leamer actually discussed this paper during an episode of EconTalk with Russ Roberts back in May 2009.)

Does this mean we should be aiming for Real estate level targeting :)

ReplyDeleteWith the fed holding MBS, that's what we're doing. ;)

Deletehaha!

DeleteGood post but I was wondering if you could write a litte more on this subject? I’d be very thankful if you could elaborate a little bit further. Appreciate it! תמ"א 38 רמת אביב

ReplyDeleteI recently came across your blog and have been reading along. I thought I would leave my first comment. I don't know what to say except that I have enjoyed reading. Nice blog. I will keep visiting this blog very often. Haute Residence Rancho Santa Fe Luxury Real Estate

ReplyDeleteThis is very educational content and written well for a change. It's nice to see that some people still understand how to write a quality post! HOA Services

ReplyDelete

ReplyDeleteتسليك مجاري

تنظيف افران

Ankara

ReplyDeleteAntalya

istanbul

Ordu

izmir

XJG0L

elazığ

ReplyDeletebilecik

kilis

sakarya

yozgat

BDGWO

kars

ReplyDeletesinop

sakarya

ankara

çorum

M6SB

https://titandijital.com.tr/

ReplyDeletetunceli parça eşya taşıma

ordu parça eşya taşıma

aydın parça eşya taşıma

van parça eşya taşıma

PH5T6

Adıyaman Lojistik

ReplyDeleteTrabzon Lojistik

Muğla Lojistik

Bayburt Lojistik

Bayburt Lojistik

İTF8

51626

ReplyDeleteGölbaşı Fayans Ustası

Ağrı Şehirler Arası Nakliyat

Antalya Şehir İçi Nakliyat

Giresun Parça Eşya Taşıma

Çankaya Fayans Ustası

Bitlis Şehirler Arası Nakliyat

Batman Şehir İçi Nakliyat

Muş Lojistik

Karapürçek Boya Ustası

F42F2

ReplyDeletesteroid cycles for sale

buy parabolan

Sivas Evden Eve Nakliyat

order steroid cycles

trenbolone enanthate for sale

masteron

Çerkezköy Çatı Ustası

buy testosterone propionat

Ankara Asansör Tamiri

39C2D

ReplyDeleteBingöl Evden Eve Nakliyat

Bitexen Güvenilir mi

Ünye Petek Temizleme

İstanbul Evden Eve Nakliyat

Coin Nedir

Malatya Şehir İçi Nakliyat

Van Evden Eve Nakliyat

Samsun Parça Eşya Taşıma

Yozgat Parça Eşya Taşıma

631A6

ReplyDeleteprimobolan for sale

Şırnak Evden Eve Nakliyat

buy steroid cycles

Tekirdağ Cam Balkon

Giresun Evden Eve Nakliyat

trenbolone enanthate for sale

order steroids

buy parabolan

Ardahan Evden Eve Nakliyat

F0517

ReplyDeletepeptides

masteron for sale

turinabol

buy parabolan

order parabolan

order trenbolone enanthate

testosterone propionat for sale

anapolon oxymetholone

primobolan for sale

744EC

ReplyDeleteParibu Güvenilir mi

Çanakkale Şehir İçi Nakliyat

Antep Parça Eşya Taşıma

Gümüşhane Şehir İçi Nakliyat

Area Coin Hangi Borsada

Amasya Şehirler Arası Nakliyat

Afyon Evden Eve Nakliyat

Silivri Cam Balkon

Kucoin Güvenilir mi

82A95

ReplyDeletenevşehir rastgele sohbet uygulaması

kilis goruntulu sohbet

kilis sohbet

trabzon sesli görüntülü sohbet

burdur canlı sohbet odası

tekirdağ mobil sohbet odaları

kastamonu görüntülü sohbet

aksaray canlı sohbet odası

urfa ücretsiz sohbet sitesi

D573B

ReplyDeletecanlı sohbet siteleri ücretsiz

tunceli chat sohbet

Antep Canlı Sohbet

kütahya telefonda sohbet

kütahya canlı sohbet uygulamaları

sohbet chat

trabzon telefonda görüntülü sohbet

kadınlarla görüntülü sohbet

nevşehir sohbet odaları

DC40D

ReplyDeleterastgele sohbet odaları

Erzincan En İyi Ücretsiz Sohbet Siteleri

mobil sohbet sitesi

Aksaray En İyi Rastgele Görüntülü Sohbet

ağrı ücretsiz sohbet

görüntülü sohbet

rastgele görüntülü sohbet ücretsiz

tunceli en iyi rastgele görüntülü sohbet

kars canli sohbet chat

2CFFE

ReplyDeleteburdur yabancı görüntülü sohbet siteleri

bursa görüntülü sohbet uygulamaları ücretsiz

sinop mobil sohbet chat

Çankırı Görüntülü Sohbet Uygulama

bolu kızlarla canlı sohbet

mersin muhabbet sohbet

Balıkesir Görüntülü Sohbet Uygulama

bolu parasız sohbet siteleri

kırşehir canlı sohbet ücretsiz

5CF33

ReplyDeletebedava sohbet chat odaları

bilecik telefonda kadınlarla sohbet

Kocaeli Sesli Sohbet

van yabancı canlı sohbet

canlı sohbet siteleri

sesli sohbet sitesi

sivas parasız görüntülü sohbet uygulamaları

yabancı görüntülü sohbet

adana görüntülü sohbet sitesi

9345A

ReplyDeleteKripto Para Üretme

Bitcoin Nasıl Alınır

Gate io Borsası Güvenilir mi

Cate Coin Hangi Borsada

Binance Nasıl Üye Olunur

Kripto Para Kazanma

Telegram Görüntüleme Satın Al

Parasız Görüntülü Sohbet

Binance Referans Kodu

A2CC1

ReplyDeleteTwitter Trend Topic Satın Al

Görüntülü Sohbet

Bitcoin Nasıl Kazanılır

Qlc Coin Hangi Borsada

Bitcoin Üretme Siteleri

Clubhouse Takipçi Satın Al

Kripto Para Nasıl Üretilir

Twitch Takipçi Satın Al

Btcturk Borsası Güvenilir mi

10B98

ReplyDeleteCoin Nedir

Mexc Borsası Güvenilir mi

Trovo Takipçi Hilesi

Binance Hangi Ülkenin

Tumblr Beğeni Satın Al

Bitcoin Nasıl Alınır

Binance Referans Kodu

Coin Kazma Siteleri

Apenft Coin Hangi Borsada

D85DD

ReplyDeleteledger live

sushi

avax

yearn

chainlist

trust wallet

arculus

solflare

aave

44E54D1DE6

ReplyDeletetiktok takipçi

F35943B6D1

ReplyDeletegerçek organik takipçi

3BABB8435C

ReplyDeleteyabancı takipçi satın al

Türkiye Posta Kodu

Kafa Topu Elmas Kodu

Sıra Bulucu

Azar Elmas Kodu

Danone Sürpriz Kodları

Whiteout Survival Hediye Kodu

Yalla Hediye Kodu

Coin Kazan

C0ACE484A2

ReplyDeleteinstagram takipçi

Kafa Topu Elmas Kodu

Osm Promosyon Kodu

Lords Mobile Promosyon Kodu

Total Football Hediye Kodu

Lords Mobile Promosyon Kodu

Footer Link Satın Al

Pokemon GO Promosyon Kodu

Pokemon GO Promosyon Kodu

17EA51FA77

ReplyDeleteTelegram Para Kazandıran Botlar

Telegram Airdrop Botları

Telegram Coin Botları

Telegram Para Kazanma

Binance Hesap Acma

F7A15C335D

ReplyDeleteinstagram yabancı gerçek takipçi

beğeni satın al

ig takipçi

türk takipçi

yabancı takipçi

3E83E9EEB6

ReplyDeleteorganik türk takipçi

instagram beğeni satın al

telafili takipçi

kaliteli takipçi

takipçi