Meanwhile, a small group of “rebels” that has opposed this movement for the past several years took solace in its coming unraveling. From their perspective, when the new monetarist theories are actually implemented through real-world policy, the results will mimic the failures of previous attempts at monetarism (I highly recommend reading The Scourge of Monetarism by Nicholas Kaldor). The current version, which relies on minimal empirical proof and a faulty understanding of modern monetary operations, will finally lose its luster.

Although I have been a relatively vocal member of this latter group, I suggested caution in believing the failure of new Fed policy to materially impact NGDP and unemployment, especially, would detract from monetarist momentum. Instead, at the first sign of reality diverging from expectations, I expect Market Monetarists (and most other economists who support further monetary stimulus) to claim that the most recent FOMC policy accommodations were either poorly crafted or insufficient in size. Similar reactions frequently stem from Keynesians regarding fiscal stimulus/spending, which can seemingly never be implemented correctly or in large enough doses to achieve the ideal outcome.

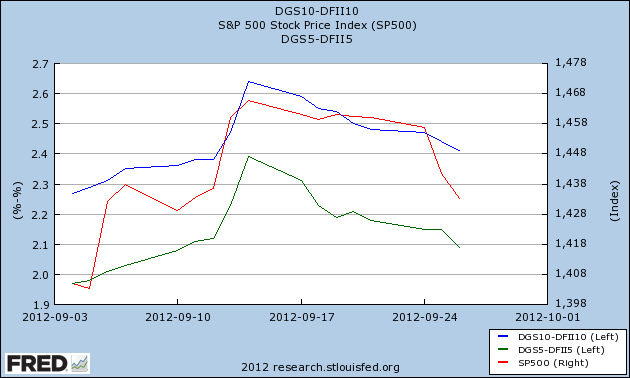

Only two weeks have passed since the FOMC policy statement was released, but inflation expectations and stocks have already given back nearly all of their gains:

(The green and blue lines depict 5- and 10-year inflation expectations, respectively, based on the difference between the corresponding Treasury rates and TIPS. The red line shows the S&P 500, which has primarily fallen since reaching a new post-recession peak the morning following the FOMC announcement.)

To my surprise, the clamor for more Fed action has already begun. Commenting on a similar graph to the one depicted above, Marcus Nunes asks:

Mr. Bernanke, “when will you ever learn”?If my expectations about the ineffectiveness of monetary stimulus and monetarist response prove correct, then Nunes’ question is only the first of what will soon be an overwhelming plea for more Fed action.

These actions over the past couple weeks have reminded me of Buzz Lightyear’s classic line, in the movie Toy Story, “To infinity...and beyond!” The Fed’s new policy offers potentially infinite asset purchases, but doubt is quickly growing over whether infinity is enough. Will we find out what is beyond QEternity?

Note: Since time has been limited these days with studying and homework, I haven't had a chance to share or comment on several wonderful posts about the reasons QEternity will be ineffective. Here are some that stood out from the rest:

A Disturbing Look Inside the Mind of Ben Bernanke

How?

Quantitative easing isn't magic

Oh NGDP, is there anything you can't do?

Endogenous Versus Exogenous Money, One More Time

Inspiration or Insanity? Fed action and Market Reaction

Effects of QE3

The Fatal Conceit

Shamanistic Economics

Bernanke Goes All In...but will it work?

Thanks for the links - and I agree with your perspective.

ReplyDeleteI'm not sure that the MMs though have been as smart as Krugman was - he got in his "it's just not enough" arguments even before the past fiscal stimulus started, taking two weeks is slacking by economists standards. ;)

I agree about the 'never enough' argument, even - to a certain extent - from the Keynesians. However, bear in mind Keynesians do have examples of where there has been enough: The New Deal before the 1937 cuts; the stimulus in 2001 in both US and UK; Sweden and China in the recent crisis.

ReplyDeleteThose are fair points/observations. Despite being skeptical of how govt actually uses deficits as stimulus, I strongly favor that approach over monetary policy given current circumstances. Also, my comment was not meant to imply that all Keynesians or Monetarists hold the 'never enough' argument but rather that it is a feature of both proposals that effectively renders them unfalsifiable.

Delete