Last Friday, over at TripleCrisis, Jeff Madrick posted 10 Questions for Economists Who Oppose Manufacturing Subsidies. Conversations regarding this topic have been persistent for much of President Obama’s term in office and are unlikely to dwindle heading towards the election. Although the questions are posed towards mainstream economists, of which I am not, here are some succinct, sensible, non-mainstream responses in opposition to to manufacturing subsidies.

1. Doesn’t America already have an anti-manufacturing strategy? It has enthusiastically supported a high value for the dollar since the 1990s. The high dollar raises export prices but, as noted, very much helps Wall Street attract capital flows and lend at low rates. Shouldn’t we get the value of the dollar down?

Answer - Lowering the value of the dollar will make exports cheaper, but it will likewise make imports more expensive. Many Americans, not on Wall Street, will therefore be able to purchase less goods with the same income. Reducing the dollar value is also an imprecise mechanism that could very well drive up food and energy prices well in excess of any benefits to manufactures.

2. Don’t Germany, China, and many other countries subsidize their own manufacturing industries? Do you really think the World Trade Organization works all these out? If they do subsidize, isn’t it only fair to place manufacturing on a level playing field and subsidize our own?

Answer - While Germany, China and many other countries do subsidize their own manufacturing industries, America currently does as well. A cursory glance at the tax statements of GE, GM, Ford and a host of other manufacturers will display a multitude of tax breaks/loopholes specifically to support American manufacturing. A better questions is whether or not American taxpayer dollars are best used supporting/bailing out manufacturing companies so that foreign consumers can buy goods at cheaper prices.

3. Doesn’t manufacturing having a multiplier effect? Some say we can never boost the share of manufacturing adequately. So what if we create even as much as another 2 or 3 million manufacturing jobs. (The president is settling for a couple of hundred thousand.) But wouldn’t manufacturing’s multiplier effect stimulate the rise of other manufacturing and service industries and the creation of other jobs?

Answer - Despite receiving massive subsidies over the past decade(s), the companies mentioned in question 2 have been shedding American workers. Efforts to stimulate manufacturing jobs are more likely to redirect funds from other sectors, resulting in American job losses outside of manufacturing. Accounting for the potential production of those 2 or 3 million outside of manufacturing, any multiplier effect is not necessarily positive. A cardinal rule of economics is there is no free lunch, hence creating manufacturing jobs will not be free.

4. How can we get our trade deficit down if we don’t sell more manufactures? They account for about seven-eighths of our exports. I know the answer some of you will give: savings. But do you really think raising our savings rate will reduce capital inflows adequately to lower the dollar in order to promote more exports?

Answer - This question assumes that reducing the trade deficit is definitively positive and that a lower dollar is needed to promote exports, both of which are not true. Until this past year, Japan ran persistent trade surpluses notwithstanding an almost perpetually rising Yen. Regardless, a different answer than the one expected: services. As noted above, manufactures are not the only form of exports (or imports). During the past century, US exports shifted dramatically from agriculture to manufactures. Over the next century is may shift again towards services.

5. Without manufacturing, what will we export? Isn’t there a point at which we lose too many industries and labor skills to make a comeback? Given the symbiotic nature of business clusters and supply chains, aren’t we rapidly losing the subsidiary companies that make manufacturing and exports possible?

Answer - As mentioned above, similar arguments were made when manufacturing began encroaching on agriculture’s territory. Looking back, few people probably wish that agriculture had been protected so that many of us would still be working on farms today. Google makes enormous profits across the globe even though it manufactures almost nothing. What’s wrong with most Americans eventually working in offices rather than factories?

6. Weren’t persistent trade imbalances a major cause of the 2007-2008 financial crisis as debt levels soared? Don’t you worry that the export-led models of China, Germany, and Japan are unsustainable? On a worldwide basis, they are really debt-led growth models. How do we get balance without promoting our exports?

Answer - Trade imbalances and debt levels are separate, relatively uncorrelated factors, of which the latter was more likely a major cause of the financial crisis. Total debt levels soared in the US and many European countries with import-led models as well. If debt levels are a major problem, which I believe is true, than one option to achieve balance would be reducing subsidies to acquiring debt, such as the mortgage interest deduction.

7. Isn’t manufacturing a source of innovation in and of itself? Isn’t that where the scientists and engineers are? Don’t we learn and innovate by doing? One commentator recently said that those innovations are exploited by others, so it doesn’t matter. Really? Then maybe we should stop promoting R&D altogether.

Answer - Manufacturing is one source of innovation, but what about companies like Amazon, Netflix, Apple and Facebook. Is buying goods online today not cheaper and quicker? Is watching movies and listening to music not more accessible for less cost? Can we not interact with people all over the world far quicker and more easily? These companies and others are constantly innovating and improving our lives, undeterred by a lack of manufacturing or scientists..

8. Where will the good jobs come from? You always say high technology. But America now imports more high-technology products than it exports, especially to China. Even Germany has a high-technology deficit with China. I ask again, where will the jobs come from as technology gets more complex? Do you think more education is really an adequate answer, the only answer?

Answer - Why are manufacturing jobs so ‘good’? Does this imply that all non-manufacturing (or high-tech) jobs are ‘bad’? What about teachers or doctors? The future offers a potentially massive increase in service jobs with new markets that have not yet been conceived. Education within schools may not be adequate and is certainly not the only answer, however education through increasing work apprenticeships may be a good place to start.

9. Why did the job market do so poorly throughout the 2000s? If you say we can’t know where jobs will come from, that the market will decide, then why aren’t you worried about the job market’s poor performance over the last decade, with huge losses in manufacturing jobs? Again, you say, inadequate education. Yetaccording to CEPR’s John Schmitt, we have not produced more good jobs as GDP grew — good jobs measured by wages and benefits provided. Is there hard evidence we don’t have the labor to fill the high-technology jobs — and if we did, are there enough jobs going unfilled to make a difference?

Answer - According to CEPR’s Dean Baker, in The End of Loser Liberalism: Making Markets Progressive, supposedly “free-trade” agreements have exposed many lower wage (manufacturing) jobs to foreign competition while erecting barriers against trade in higher wage areas such as health care and law. At the same time, patent laws and tax codes have been continually adjusted to protect large corporations and enforce monopolies. The economy is also structured to encourage home buying/building, which for some time vastly expanded construction jobs beyond a sustainable amount. Even with all of these poor choices, about 92% of Americans desiring work are employed today. Americans have the knowledge and expertise to reach full-employment, but policies that raise the cost of hiring workers and discourage small business creation are not helping.

10. Will the jobs come from services? The rapid growth of finance has fouled up the numbers. Finance services did provide high-paying jobs, but we now know many of these were phantoms. And the salad days may be over. The other big area of productivity growth in services was retail. We all know what kinds of jobs Wal-Mart provided.

Answer - Yes, services will provide one source of new jobs but hopefully finance will not be a significant contributor. It remains unclear why manufacturing jobs are necessarily better than retail or other service jobs. Either way, the beauty of capitalism is that the future is unknown but there has been no better economic system in history for supporting growth. Jobs will return, but manufacturing subsidies are not the best approach and may well cause more job losses than they create.

Tuesday, February 28, 2012

Sunday, February 26, 2012

Quote of the Week

...is from The Intelligent Investor, Rev. Ed (2009) by Benjamin Graham and Jason Zweig:

“About a half century ago the “miracles” were often accompanied by flagrant manipulation, misleading corporate reporting, outrageous capitalization structures, and other semifraudulent financial practices. All this brought on an elaborate system of financial controls by the SEC, as well as a cautious attitude toward common stocks on the part of the general public. The operations of the new “money managers” in 1965–1969 came a little more than one full generation after the shenanigans of 1926–1929. The specific malpractices banned after the 1929 crash were no longer resorted to—they involved the risk of jail sentences. But in many corners of Wall Street they were replaced by newer gadgets and gimmicks that produced very similar results in the end. Outright manipulation of prices disappeared, but there were many other methods of drawing the gullible public’s attention to the profit possibilities in “hot” issues. Blocks of “letter stock” could be bought well below the quoted market price, subject to undisclosed restrictions on their sale; they could immediately be carried in the reports at their full market value, showing a lovely and illusory profit. And so on. It is amazing how, in a completely different atmosphere of regulation and prohibitions, Wall Street was able to duplicate so much of the excesses and errors of the 1920s.”Graham was talking about the late 1960’s, a period few recall today, that presaged nearly 16 years of a sideways stock market. Now another full generation later, these insights are once again especially relevant. New “hot” issues within technology (ie. Facebook), fraudulent practices in mortgage lending, debt-heavy capitalization structures and the continued absence of mark-to-market accounting are the new means of portraying illusory profits. Graham then continues:

“No doubt there will be new regulations and new prohibitions. The specific abuses of the late 1960s will be fairly adequately banned from Wall Street. But it is probably too much to expect that the urge to speculate will ever disappear, or that the exploitation of that urge can ever be abolished. It is part of the armament of the intelligent investor to know about these “Extraordinary Popular Delusions,” and to keep as far away from them as possible.”The Dodd–Frank Wall Street Reform and Consumer Protection Act represents the most recent set of regulations intended to prevent, or at least limit, the most recent forms of abuse. Just as the reforms of the 1930’s, 1970’s and even 2000’s have failed to alter this dominant cycle, the current efforts are almost certain to follow the same path. Regulations may prevent a repeat of the exact actions previously abused, but may also provide the loopholes necessary for the next semi-fraudulent scheme. Both investors and policy markers should be wary of these historical lessons when approaching future actions.

Saturday, February 25, 2012

Points of Public Interest

- Restraining unit labor costs is a right-wing conspiracy - Steve Randy Waldman discusses how the Federal Reserve’s explicit actions are helping reduce labor’s share of output over time.

- The rule of more - A former professor of mine, Susan Dudley, is quoted on the subject of inconsistent cost-benefit analysis that allows the regulatory system to be gamed. (h/t Cafe Hayek)

- Keeping an Eye on Wealth Creation - Renowned investor Hugh Hendry continues to expect a Chinese hard landing and, most importantly, expresses his view that “ the road to hyperinflation is via hyperdeflation.”

- Hayek, Equilibrium and Complexity - Paul Omerod succinctly explains the importance of Hayek’s thinking to the study of complex systems.

- The Longest Quarterly Letter Ever - Legendary investor Jeremy Grantham offers his updated investment outlook and continues to recommend patience. (h/t Zero Hedge)

Sunday, February 19, 2012

Quote of the Week

...is from Of the Influence of Consumption on Production by John Stuart Mill (h/t Russ Roberts of Cafe Hayek):

Nearly 200 years ago, Mill recognized the faulty logic in trying to stimulate wealth by encouraging individuals to increase consumption. Sadly this lesson remains unlearned, as far too many public policies today are directed at subsidizing consumption (ie. autos, houses, oil). What is worse, a great deal of discussion regarding this topic blatantly ignores that two types of consumption even exist. Partially due to this omission, incentives to consume are often directed towards the unproductive type.

At an early age I was taught the virtues of saving and the potential benefit of compound interest. It strikes me as odd that this lesson, generally taught to children, is reversed for adults on the macro scale. Holding large amounts of outstanding debt (auto loans, mortgages, student loans, credit cards) has seemingly become the norm and an expected outcome for many individuals. Compound interest works against the borrower, raising the level of outstanding debt and reducing chances of ever paying down principal balances. (This appears to be precisely how the private sector can maintain a positive savings rate while the ratio of private debt to GDP continually increases.)

The Great Recession was largely influenced by a massive accumulation of private/household debt that could not be repaid or refinanced when assets values, most notably homes, turned lower. Increasing the nation’s wealth, for more than a couple years, will not be attained by stimulating unproductive consumption. Policy discussion must now shift to encouraging a healthy level of saving and greater focus on reproductive consumption.

II.4

In opposition to these palpable absurdities, it was triumphantly established by political economists, that consumption never needs encouragement. All which is produced is already consumed, either for the purpose of reproduction or of enjoyment. The person who saves his income is no less a consumer than he who spends it: he consumes it in a different way; it supplies food and clothing to be consumed, tools and materials to be used, by productive labourers. Consumption, therefore, already takes place to the greatest extent which the amount of production admits of; but, of the two kinds of consumption, reproductive and unproductive, the former alone adds to the national wealth, the latter impairs it. What is consumed for mere enjoyment, is gone; what is consumed for reproduction, leaves commodities of equal value, commonly with the addition of a profit. The usual effect of the attempts of government to encourage consumption, is merely to prevent saving; that is, to promote unproductive consumption at the expense of reproductive, and diminish the national wealth by the very means which were intended to increase it.

II.5

What a country wants to make it richer, is never consumption, but production.

Nearly 200 years ago, Mill recognized the faulty logic in trying to stimulate wealth by encouraging individuals to increase consumption. Sadly this lesson remains unlearned, as far too many public policies today are directed at subsidizing consumption (ie. autos, houses, oil). What is worse, a great deal of discussion regarding this topic blatantly ignores that two types of consumption even exist. Partially due to this omission, incentives to consume are often directed towards the unproductive type.

At an early age I was taught the virtues of saving and the potential benefit of compound interest. It strikes me as odd that this lesson, generally taught to children, is reversed for adults on the macro scale. Holding large amounts of outstanding debt (auto loans, mortgages, student loans, credit cards) has seemingly become the norm and an expected outcome for many individuals. Compound interest works against the borrower, raising the level of outstanding debt and reducing chances of ever paying down principal balances. (This appears to be precisely how the private sector can maintain a positive savings rate while the ratio of private debt to GDP continually increases.)

The Great Recession was largely influenced by a massive accumulation of private/household debt that could not be repaid or refinanced when assets values, most notably homes, turned lower. Increasing the nation’s wealth, for more than a couple years, will not be attained by stimulating unproductive consumption. Policy discussion must now shift to encouraging a healthy level of saving and greater focus on reproductive consumption.

Saturday, February 18, 2012

Points of Public Interest

- Up to Speed, but Still Lagging Behind and "Memento", the Meltdown and the Mainstream - Matias Vernengo notes how a recent survey of mainstream economists, meant to offer an ex post explanation of the financial crisis, fails to acknowledge the numerous contributions of heterodox economists ex ante. Gerald Epstein expands the list of economists, who are broadly trained in the ideas of Keynes and Minsky. Both articles include links to some very important papers and ideas still overlooked by mainstream economists.

- So, what would your plan for Greece be? - Over at Crooked Timber they have created an interesting, fun “Choose Your Own Adventure” for resolving Greece’s current troubles. (h/t The Reformed Broker)

- Face the Music - Excellent interview with Lacy Hunt of Hoisington Investment Management. Hunt approaches investing from a non-equilibrium economic perspective that focuses on debt levels across sectors of the economy. My belief that 30-year Treasuries will ultimately touch 2% in this cycle is shared by Hunt.

- What the Austrian Business Cycle Theory Can and Cannot Explain - Steve Horwitz argues that the “ABCT is not a theory of the causes of the length and depth of recessions/depressions, but a theory of the unsustainable boom.”

- More on Savings and Investment - Michael Sankowski directs us to Steve Waldman, who explains why a government deficit is not necessary for the household sector to increase savings.

- LTRO: A User's Manual (h/t Zero Hedge)

Thursday, February 16, 2012

Returning Economics to Reality

As I mentioned recently in the Quote of the Week, Hyman Minsky’s work on financial instability continues to play a major role in my own thinking and in several strands of heterodox economics. A dissertation advisee of Minsky’s, Randall Wray, partially founded Modern Monetary Theory (MMT) which falls within a similar realm of economic thinking. When I began exploring economic blogs nearly two years ago, MMT offered an escape from mainstream (neo-classical synthesis) thinking and provided a better fit with my perception of reality. Diving deeper into the theory, I continued to learn a great deal from the descriptive aspects but felt there lay an inconsistency with the prescriptive, political policy recommendations. Luckily Cullen Roche of Pragmatic Capitalism (who has played an invaluable role in my learning) has helped create a solution.

Just over one week ago, Modern Monetary Realism: Economics Without Politics... was launched. Attempting to remove the prescriptive aspects from MMT and basic economic thinking, “Modern Monetary Realism (MMR) is a description of the monetary system within a nation operating a fiat currency which involves an autonomous monetary system, monopoly supply of currency and floating exchange rates.” Only days after posting a primer, Understanding Modern Monetary Realism, a fascinating discussion broke out in the comments section involving Cullen and JKH, among others. Although I recommend reading through the entirety of the page, the general conclusion is that MMT relies upon a federal Job Guarantee program and corresponding nationalization of the financial sector. As with any grouping of individuals, there will certainly be some MMTers whom only align with certain aspects (myself included). Regardless, these policy positions are clearly at the heart of my concern in accepting the prescriptive measures of MMT. (I hope to elaborate on both the positive and negative aspects of MMT in a future post.)

The Great Recession has exposed many ways in which mainstream economic theories are devoid of any realistic application to our current social (human) environment. Modern Monetary Realism, in its limited time, has already made a significant impact in bringing economics back to reality. My hunch is that MMR will ultimately play an important role in defining the future direction of economics. Understanding the operational aspects of our monetary system is a critical first step in grounding policy discussions. Hopefully more widespread recognition of these descriptive factors will lead to better, more informed policy decisions in the future.

Just over one week ago, Modern Monetary Realism: Economics Without Politics... was launched. Attempting to remove the prescriptive aspects from MMT and basic economic thinking, “Modern Monetary Realism (MMR) is a description of the monetary system within a nation operating a fiat currency which involves an autonomous monetary system, monopoly supply of currency and floating exchange rates.” Only days after posting a primer, Understanding Modern Monetary Realism, a fascinating discussion broke out in the comments section involving Cullen and JKH, among others. Although I recommend reading through the entirety of the page, the general conclusion is that MMT relies upon a federal Job Guarantee program and corresponding nationalization of the financial sector. As with any grouping of individuals, there will certainly be some MMTers whom only align with certain aspects (myself included). Regardless, these policy positions are clearly at the heart of my concern in accepting the prescriptive measures of MMT. (I hope to elaborate on both the positive and negative aspects of MMT in a future post.)

The Great Recession has exposed many ways in which mainstream economic theories are devoid of any realistic application to our current social (human) environment. Modern Monetary Realism, in its limited time, has already made a significant impact in bringing economics back to reality. My hunch is that MMR will ultimately play an important role in defining the future direction of economics. Understanding the operational aspects of our monetary system is a critical first step in grounding policy discussions. Hopefully more widespread recognition of these descriptive factors will lead to better, more informed policy decisions in the future.

Sunday, February 12, 2012

Quote of the Week

...is from p.162-163 of Hyman Minsky’s superb book, John Maynard Keynes:

Minsky has been on my mind frequently over the past few months as much of today’s economic work in Post-Keynesianism and Modern Monetary Theory stem from his unique insights about instability in a capitalist society. In Facebook's $500 Million Tax Refund and The BIG Political Lie, I was trying to shed light on the manner by which politicians control the tax system to redistribute income upwards. Minsky brilliantly expands on this concept above, noting how policy that guarantees profits (quasi-rents) from speculation leads to instability. The rise in non-traditional mortgages, extremely low levels of down payments and government support in the recent housing crisis represents a prime example of the consequences highlighted above. As long as policy continues in this manner, economic performance is likely to be volatile and current income inequality will persist or expand even further.

“The economy is now a controlled rather than a laissez-faire economy; however, the thrust of the controls is not in the direction envisaged by Keynes. Investment has not been socialized. Instead, measures designed to induce private investment, quite independently of the social utility of investment, have permeated the tax and subsidy system.”

“The success of a high-private-investment strategy depends upon the continued growth of relative needs to validate private investment. It also requires that policy be directed to maintain and increase the quasi-rents earned by capital—i.e., rentier and entrepreneurial income. But such high and increasing quasi-rents are particularly conducive to speculation, especially as these profits are presumably guaranteed by policy. The result is experimentation with liability structures that not only hypothecate increasing proportions of cash receipts but that also depend upon continuous refinancing of asset positions. A high-investment, high-profit strategy for full employment—even with the underpinning of an active fiscal policy and an aware Federal Reserve System—leads to an increasingly unstable financial system, and an increasingly unstable economic performance.”

Minsky has been on my mind frequently over the past few months as much of today’s economic work in Post-Keynesianism and Modern Monetary Theory stem from his unique insights about instability in a capitalist society. In Facebook's $500 Million Tax Refund and The BIG Political Lie, I was trying to shed light on the manner by which politicians control the tax system to redistribute income upwards. Minsky brilliantly expands on this concept above, noting how policy that guarantees profits (quasi-rents) from speculation leads to instability. The rise in non-traditional mortgages, extremely low levels of down payments and government support in the recent housing crisis represents a prime example of the consequences highlighted above. As long as policy continues in this manner, economic performance is likely to be volatile and current income inequality will persist or expand even further.

Saturday, February 11, 2012

Points of Public Interest

- Why Jews Don’t Farm - Steve Landsburg approaches this question from the perspective of literacy and education as hallmarks of Jewish religion. (h/t Don Boudreaux, Cafe Hayek)

- Repulsive progressive hypocrisy - Glenn Greenwald expresses fear over Democratic support for policies, including Guantanamo and drone usage, under the Obama Administration that were highly criticized when similarly carried out by the Bush Administration. I share Greenwald’s concern that political support may become tied to individuals rather than actual policy actions. (h/t Anthony Gregory, The Beacon: “Repulsive Progressive Hypocrisy” and Why Peaceniks Should Oppose Democrats)

- What Europe might look like without the Eurozone and EU - Bruno Frey dispels with the view that a collapse of the Euro will lead to chaos and war. On the contrary, he argues that countries will likely establish more flexible, smaller agreements that maintain free trade and may even improve European economic prospects.

- The Top Twelve Reasons Why You Should Hate the Mortgage Settlement by Yves Smith

- S = I + (S – I) : The Most Important Equation in Economics The “mysterious” JKH explains a key component of sectoral balances in an incredibly clear and concise fashion.

- How Economists Contributed to the Financial Crisis John T. Harvey discussed how making math the ends rather than means of economics has led much of the discipline off course from the real world. Post-Keynesianism, especially Steve Keen, and MMT receive acknowledgement for raising awareness of the crisis in advance and, in my opinion, continue to offer some of the best insights. (h/t Tom Hickey, Mike Norman Economics)

Thursday, February 9, 2012

Facebook's $500 Million Tax Refund and The BIG Political Lie

Over the next nine months, leading up to the Presidential election, conversations about optimal tax rates are certain to play a major role. Much of the recent media focus has already addressed the low effective tax rates paid by both Warren Buffett and Mitt Romney (although the light in which the two are held is a world apart). Current debate generally regards the low level of taxes paid by both men as being “unfair,” leading to calls for higher income tax rates on the wealthy. Although this proposed solution seems obvious, the reality is that neither Buffett or Romney will end up paying significantly more even if income tax rates return to the levels during the Clinton era.

How could this be? Behind this confusion lies innumerable intricacies within the US tax code, where rates differ for varying types of income and the laws are littered with various deductions, credits and provisions. Facebook’s upcoming IPO displays a perfect example of the unintended consequences of US tax laws. In Options and Taxes: Is a "Facebook" tax next?, Aswath Damodoran (NYU finance professor) comments that:

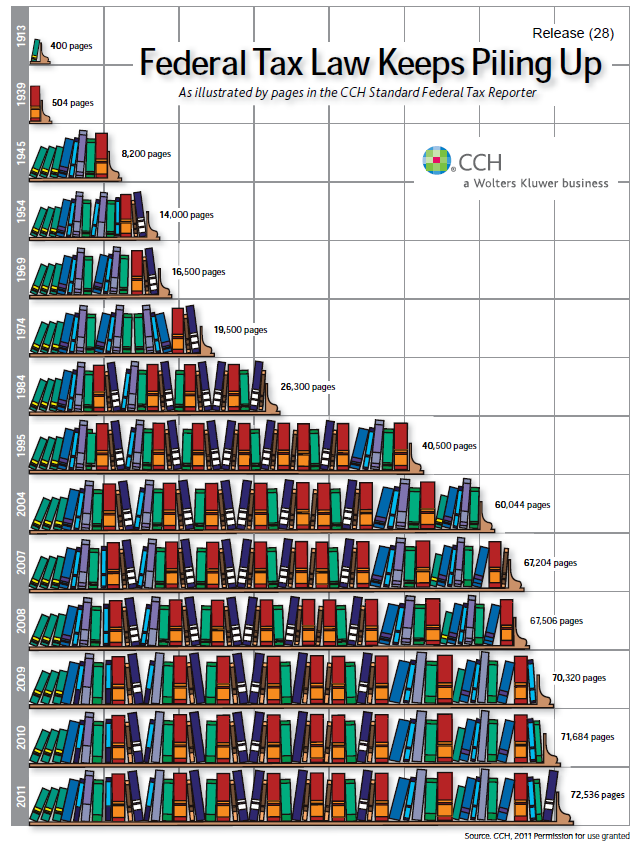

When these questions are posed, a typical response suggests these outcomes represent the natural workings of a free-market system. Sadly this could not be farther from the truth. As Mish Shedlock points out in Is Romney to Blame for Paying Low Taxes or is 72,536 Pages of Tax Code to Blame? What's the Real Solution? Thanks to AMT, Man Pays 102% Tax Rate, “from 1984 until now, 46,236 pages of tax code have been added.” (shown below) Anyone would be hard pressed to find an economist who believes this level of complexity is either efficient or representative of a free-market economy.

How could this be? Behind this confusion lies innumerable intricacies within the US tax code, where rates differ for varying types of income and the laws are littered with various deductions, credits and provisions. Facebook’s upcoming IPO displays a perfect example of the unintended consequences of US tax laws. In Options and Taxes: Is a "Facebook" tax next?, Aswath Damodoran (NYU finance professor) comments that:

“Mark Zuckerberg is planning to exercise about $ 5 billion of options ahead of the offering, resulting in a tax bill of roughly $ 2 billion for him.”*On the surface, this seems reasonable since Zuckerberg will be paying nearly 40 percent between federal and state income taxes. The criticism stems from the corporate tax deductions that Facebook is permitted based on the exercise of employee stock options, including Zuckerberg’s. As WithumSmith + Brown states in Tax Aspects of the Facebook IPO (Alternate Title: Mark Zuckerberg Could Buy Most of Europe With His 2012 Tax Bill):

“Assuming Facebook stock reaches a price of $40 per share on the open market, the corporate deduction related to the exercise of employee options will be in the billions; large enough not only to enough to wipe out the comany’s 2012 taxable income, but also –according to the prospectus — to generate an NOL [net operating loss] that will be carried back to generate $500 million in tax refunds.”From a distinctly corporate perspective, Facebook, which may earn upwards of $2 billion in pre-tax income this year, will not only owe nothing in taxes but may actually receive a $500 million refund. How is it that an extremely profitable company ends up with a sizable tax refund? Why has GE and numerous other companies not paid taxes during the past decade despite earning substantial profits (G.E.’s Strategies Let It Avoid Taxes Altogether)? Why does Warren Buffett pay a smaller effective tax rate than his secretary?

When these questions are posed, a typical response suggests these outcomes represent the natural workings of a free-market system. Sadly this could not be farther from the truth. As Mish Shedlock points out in Is Romney to Blame for Paying Low Taxes or is 72,536 Pages of Tax Code to Blame? What's the Real Solution? Thanks to AMT, Man Pays 102% Tax Rate, “from 1984 until now, 46,236 pages of tax code have been added.” (shown below) Anyone would be hard pressed to find an economist who believes this level of complexity is either efficient or representative of a free-market economy.

click on chart for sharper images

Image from Tax Law Pile Up

The reality is that consistent increases and alterations of US tax code, over the years, is primarily intended to benefit a special group or class. A rational choice perspective of public policy and administration implies that much, if not most, of this tinkering is done at the behest of groups with the largest political sway (funding capacity and desire).

Improving the tax system is possible both from the perspective of reducing government intervention and increasing progressiveness. Unfortunately the right (conservatives) has been persuasive in convincing individuals across the political spectrum that a complex tax code is part of a free-market system. In The End of Loser Liberalism: Making Markets Progressive, Dean Baker expresses his feelings on this subject noting:

“the vast majority of the right does not give a damn about free markets; it just wants to redistribute income upward.”It’s important to note that the left (liberals) has also been complicit in this false perception, frequently adjusting the tax code in regressive ways to garner political funding and support.

Heading towards the election, both political parties will try to represent the current US tax system as “unfair” in an effort to push new laws that will “right” the system. Adding more layers of complexity, however, is unlikely to make the outcomes either more efficient or progressive. Overcoming the current trend requires exposing the truth that our current tax codes do not represent a free market. Hopefully both sides of the political spectrum can join together in encouraging politicians to create a far simpler, progressive tax system.

*Zuckerberg plans to exercise options for 120 million shares with an exercise price of $0.06. The nearly $5 billion profit assumes a per share value of approximately $40.

Monday, February 6, 2012

Quote of the Week

...is from p.152 of Raghuram Rajan’s 2010 book, Fault Lines: How Hidden Fractures Still Threaten the World Economy:

“If banks have an incentive to take risk, they will always look for opportunities to get the greatest bang for the regulatory buck. But the regulatory mistake of requiring too little capital for certain activities is then compounded because in taking advantage of regulatory mistakes, banks build up exposure to the same risks. The dynamic associated with systemic risk exposures then kicks in: if everyone is exposed to the same risk in a big way, the authorities have no option but to intervene to support banks and the market if the risk materializes—in which case a bank maximizes profits by increasing exposure to the risk.”

In Rajan’s book the above statement was largely referring to the mass accumulation of mortgage related debt by all the large US banks. The concept may however be prescient when considering the actions of European banks purchasing large quantities of sovereign debt. Based on current market prices for sovereign and mortgage debt, many large European banks are likely insolvent. Thanks to lax accounting requirements and massive balance sheet expansion by the ECB (and other Eurozone central banks), these banks have been able to continue operating. Unless the European economy picks up dramatically across the board, the only chance to return to solvency is through earning substantial profits.

Faced with this troublesome predicament, the best option for European banks may be to vastly increase risk by loading up on European sovereign debt. Private investors in Greek and Portuguese debt will almost certainly face write-downs, however greater effort is being made to ensure Italy and Spain’s creditors are bailed out. By investing in shorter-term Spanish and Italian debt, banks have the potential for sizable profits if the bailout mechanisms are successful for at least a couple years. Even if these profits fail to return the banks to solvency, the returns can be used to continue paying large bonuses over the coming years. If these bets on sovereign debt fail, but enough troubled banks are playing the game, the ECB and EU will almost certainly be pressured to bailout the banks. Although risk may appear to be subsiding, systemic risk may actually be building in the background.

“If banks have an incentive to take risk, they will always look for opportunities to get the greatest bang for the regulatory buck. But the regulatory mistake of requiring too little capital for certain activities is then compounded because in taking advantage of regulatory mistakes, banks build up exposure to the same risks. The dynamic associated with systemic risk exposures then kicks in: if everyone is exposed to the same risk in a big way, the authorities have no option but to intervene to support banks and the market if the risk materializes—in which case a bank maximizes profits by increasing exposure to the risk.”

In Rajan’s book the above statement was largely referring to the mass accumulation of mortgage related debt by all the large US banks. The concept may however be prescient when considering the actions of European banks purchasing large quantities of sovereign debt. Based on current market prices for sovereign and mortgage debt, many large European banks are likely insolvent. Thanks to lax accounting requirements and massive balance sheet expansion by the ECB (and other Eurozone central banks), these banks have been able to continue operating. Unless the European economy picks up dramatically across the board, the only chance to return to solvency is through earning substantial profits.

Faced with this troublesome predicament, the best option for European banks may be to vastly increase risk by loading up on European sovereign debt. Private investors in Greek and Portuguese debt will almost certainly face write-downs, however greater effort is being made to ensure Italy and Spain’s creditors are bailed out. By investing in shorter-term Spanish and Italian debt, banks have the potential for sizable profits if the bailout mechanisms are successful for at least a couple years. Even if these profits fail to return the banks to solvency, the returns can be used to continue paying large bonuses over the coming years. If these bets on sovereign debt fail, but enough troubled banks are playing the game, the ECB and EU will almost certainly be pressured to bailout the banks. Although risk may appear to be subsiding, systemic risk may actually be building in the background.

Sunday, February 5, 2012

Points of Public Interest

- THE UNLIKELY BULL MARKET - Niels Jensen, a top portfolio manager, offers his assessment of the current bull market. Remarking on his recent trip to Spain and dabbling in Post-Keynesian economics, Jensen acknowledges the myriad of fears present today but believes the cyclical (not structural) bull market remains intact for now. (h/t Cullen Roche at Pragmatic Capitalism)

- John Taylor's Open Letter To Greece: "Get Out Greece! Get Out Right Now!" - John Taylor, the CIO of FX Concepts, explains to Greece why life outside the EU will be better than within. While I agree with this view, Greece may be best off waiting for the next bailout installment before jumping ship. (h/t Zero Hedge)

- Our Counterfeit Economy - Charles Hugh Smith reveals how calculations of GDP ignore the possibility of mal-investment, both public and private. For further insight on the flaws of GDP, I recommend reading Mismeasuring Our Lives: Why GDP Doesn't Add Up by Joseph Stiglitz, Amartya Sen and Jean-Paul Fitoussi.

- How Much Does the Safety Net Help the “Very Poor”? - Anthony Gregory responds to Mitt Romney’s, somewhat out of context, claim that “I’m not concerned about the very poor” because “We have a safety net there.” Gregory points out that benefits of the welfare system (“safety net”) primarily accrue to the broad middle class. This is another good example of common misperceptions about which class(es) actually benefit from certain government programs.

- A Crisis in Two Narratives - Former IMF chief, Raghuram Rajan, counters typical Keynesian thinking with a different historical explanation of our current economic woes. In Rajan’s eyes, “pre-crisis GDP was unsustainable, bolstered by borrowing and unproductive make-work jobs.” Many proponents of the first narrative make claims about how far below potential GDP the US is currently. These estimates of potential GDP or output often assume that the previous trend is/was sustainable. Before making public policy or investment decisions, it’s always important to understand the assumptions underlying one’s reasoning.

- What future for economics? - (MUST READ) Martin Wolf summarizes a recent panel on “The Future of Economics” with ten outstanding highlights. (h/t Pete Boettke of Coordination Problem)

- No Need to Panic About Global Warming - Sixteen world-renowned scientists debate the need for dramatic action, especially the cost-benefit analysis of ‘decarbonzing’ the global economy. My science background is not nearly strong enough to know if these claims are valid, but my skeptical side is always wary of supposedly “incontrovertible” evidence about future outcomes involving human action. (h/t David Theroux of The Beacon)

Subscribe to:

Posts (Atom)