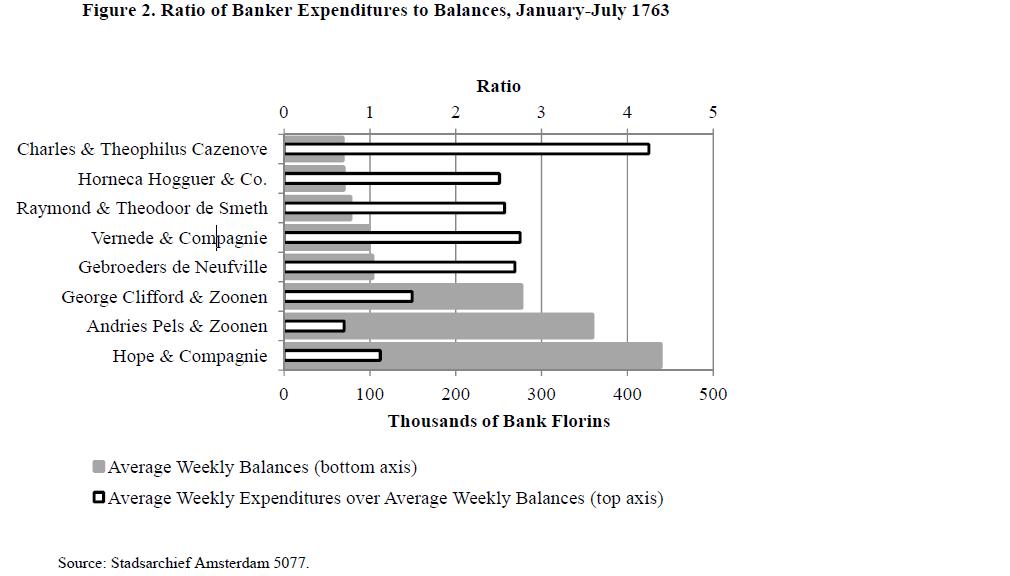

In Responding to a Shadow Banking Crisis: the Lessons of 1763, Stephen Quinn and William Roberds guide us through events leading up to Amsterdam’s banking panic and analyze the central bank’s corresponding actions. There are numerous similarities between the different periods ranging from “the Lehman-like failure of the banking house Gebroeders de Neufville (p. 3)” to the expansion of central bank liquidity “in an unprecedented and ad hoc basis. (p. 3)” Leverage also played an important role in both crises. The following chart compares the average weekly starting balances of the eight largest banks in 1763 with their average weekly turnover (i.e. the amount of borrowing necessary to fund their positions):

While credit was initially accepted from and provided to these institutions equally, those banks most highly leveraged and reliant on short-term funding found themselves in the most precarious positions following the first bank failure. It should be no surprise then that the fall of Bear Stearns, Merrill Lynch, Lehman Brothers, and potential others preceded in a similar order.

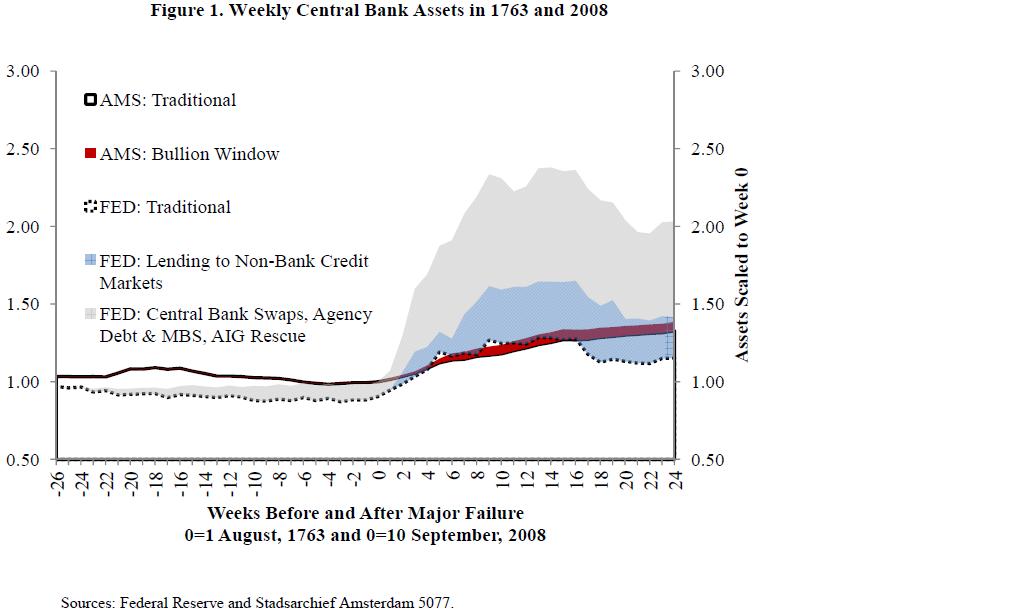

Seeking to stem the crisis, the Bank of Amsterdam (the central bank) initially allowed its balance sheet to respond endogenously to market demand through its coin window. As the stock of eligible collateral grew thin, the Bank of Amsterdam relaxed its eligibility constraints to include silver bullion. The following chart compares the rise in central bank balance sheets through various measures in each of the crises:

In 1763 and 2008, under highly different regulatory constructs, the largest banks were highly leveraged and increasingly reliant on short-term funding. Although these factors were of little concern while markets remained liquid, a sudden dearth of liquidity nearly caused numerous large bank failures and led to severe economic fallout in the surrounding areas. Responding to the crisis in 1763, notable differences were the lack of federal bailouts and the central bank’s decision to only lend against good collateral at above market rates.

The crisis of 1763 teaches us that shadow banking is not necessarily a function of eluding regulations but rather an effective means for banks to increase their extension of credit and disperse the associated risks. Unlike the measures taken in 1763, responses to the 2008 financial crisis have further reduced the incentives of bank creditors and managers to worry about leverage or liquidity. Shadow banking has a long history and will probably have a long future as well. If we are to either avoid more frequent recurrences of these crises or reduce their impact on the broader economy, we must learn and practice the lessons from history.

I knew immediately (from the dates) that this is an important topic. But I had to read it three times because, well, just because.

ReplyDeleteGood post.

The crisis of 1763 teaches us that shadow banking is not necessarily a function of eluding regulations but rather an effective means for banks to increase their extension of credit and disperse the associated risks

Then perhaps it is the excessive "extension of credit" that is the problem, and "dispersion of risks" is a warning sign.

My way of thinking about the extension of credit is that you want to encourage the dispersion of risk while providing a means for the diverging levels of risk to be reflected. Currently I believe we have successfully done the former while creating various means to restrict the latter. This implies that extension of credit is readily available during the boom and far less so when the true levels of risk are realized (which always happens).

DeleteOn a related note, I've recently been thinking about the relationship between inflation and extension of credit. When inflation is positive, companies with significant debt appear favorable due to higher returns on equity. Meanwhile, if inflation is maintained at a low level, debtors will feel increasingly confident in lending. A low, but positive inflation target (if maintained) therefore promotes rising demand and supply for credit. (I'm hoping to write up these thoughts when I have a moment).