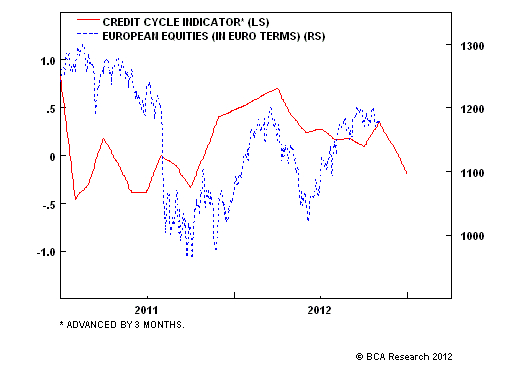

The credit impulses in all three major economies – the euro area, the U.S. and China – are now negative, albeit very slightly in the case of China. This is the first time in three years that all three components have been simultaneously negative. And after hovering at a point of inflection the combined credit cycle indicator has lurched down again.Woj’s Thoughts - As I have argued repeatedly on this blog, credit (especially private) is now the main driver of economic cycles. If broad measures of credit contract in all three major economies, it becomes increasingly unlikely that current fiscal deficits will be large enough to maintain current levels of growth (or decline in Europe’s case).

2) The US election and the fiscal cliff by Edward Harrison @ Credit Writedowns

What these three things tell me is that recession is what results from trying to reduce government deficits when the root cause of the deficits lie in private sector debt distress. When the government raises taxes or cuts spending in that situation, the result is less income in the private sector. And to the degree debt distress still exists, the result of less income is less spending and private defaults, also known as recession and credit writedowns. The larger the recession and the credit writedowns, the greater the possibility of bank failure, financial panic and debt deflation.Woj’s Thoughts - Many pundits are currently arguing that the “fiscal cliff” is over-hyped, or simply non-existent. I think they’re wrong and, similar to Harrison, believe any compromise will still result in marginal tax increases. As noted above, the credit impulse is now negative in the US, suggesting private sector debt distress persists. The fiscal situation should be watched very closely going forward.

3) Nicholas Kaldor On European Political Union by Ramanan @ The Case for Concerted Action

From Kaldor’s essay (pp. 202-207):

THE CONSEQUENCES OF A FULL ECONOMIC

AND MONETARY UNION

This is only another way of saying that the objective of a full monetary and economic union is unattainable without a political union; and the latter pre-supposes fiscal integration, and not just fiscal harmonisation. It requires the creation of a Community Government and Parliament which takes over the responsibility for at least the major part of the expenditure now provided by national governments and finances it by taxes raised at uniform rates throughout the Community. With an integrated system of this kind, the prosperous areas automatically subside the poorer areas; and the areas whose exports are declining obtain automatic relief by paying in less, and receiving more, from the central Exchequer. The cumulative tendencies to progress and decline are thus held in check by a “built-in” fiscal stabiliser which makes the “surplus” areas provide automatic fiscal aid to the “deficit” areas.

...

Some day the nations of Europe may be ready to merge their national identities and create a new European Union – the United States of Europe. If and when they do, a European Government will take over all the functions which the Federal government now provides in the U.S., or in Canada or Australia. This will involve the creation of a “full economic and monetary union”. But it is a dangerous error to believe that monetary and economic union can precede a political union or that it will act (in the words of the Werner report) “as a leaven for the evolvement of a political union which in the long run it will in any case be unable to do without”. For if the creation of a monetary union and Community control over national budgets generates pressures which lead to a breakdown of the whole system it will prevent the development of a political union, not promote it.Woj’s Thoughts - Although Kaldor espoused these opinions more than 40 years ago, there are still countless people today holding out hope that Europe creates a full fiscal union on the road to political union and ultimately becoming the United States of Europe. In my opinion, U.S. of Europe optimists continually overestimate the ease with which fiscal integration, not only harmonisation, is achievable. Convincing various populations to accept a common social welfare scheme, uniform tax rates and indefinite transfers is likely not achievable within the next decade, if at all. Democracies in Europe are already falling due to the strain of economic depression and widespread unemployment. Relative stability may persist for a few more years, but the political crisis will come to a head well before fiscal and/or political integration is possible.

No comments:

Post a Comment