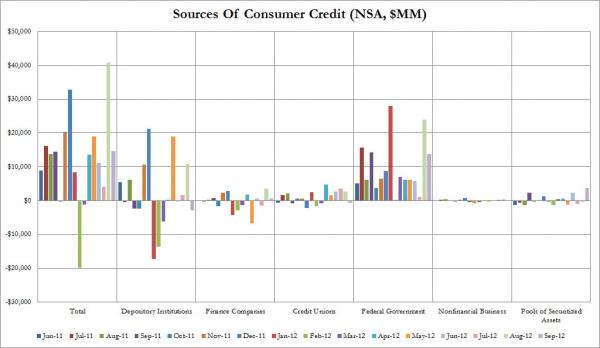

As the just released G.19 confirmed, in September, households once again reduced their credit card debt, which declined by $2.9 billion to $852 billion. This was the fourth such decline in six months, confirming that at the discretionary level where banks have supervision over borrowings, the consumer is still nowhere near willing to relever. Where, there was leverage, a lot of it, was once again in the government sector, which funded $13.8 billion of the total $14.6 billion rise in NSA credit, and where non-revolving credit: read loans for Government Motors, at least those that have not been record channel stuffed (as reported previously) and Federal Student Loans, which are now over $1 trillion, rose by $14.3 billion in one month. Of course, the difference between revolving and non-revolving credit is that while banks expect the former to be paid off eventually, Uncle Sam has no such illusions on any low APR debt it hands out to anyone who asks for it (and if the proceeds from student loans are used to purchase iPads, so be it).Aside from the notion that most new credit growth stems from the federal government (e.g. student loans), the degree to which credit is extended for car purchases/leases remains troubling. When one considers the extension of credit for housing, investments or education, there is a clear path by which that investment could generate positive returns and make future repayment of principal and interest easier. However, when it comes to spending on automobiles (or consumption goods) there is presumably no expectation for a positive return since cars lose a significant portion of their “value” once driven off the lot. Hence auto loans are seemingly granted on the basis that borrowers face short-term liquidity issues or will experience increased future returns from other investments.

Assuming the above mentioned reasons for providing auto loans are largely correct, there is clearly an opportunity for market participants with excess liquidity (e.g banks) to offer loans in hopes of earning a profit. In doing so, the private participants (ideally) also accept the risk of losses stemming from non-repayment. The market price (again, ideally) adjusts to reflect the most current expectations of risk and reward, as seen through supply and demand.

How does this relate back to the government? As most people know, during the financial crisis, the U.S. government took control over General Motors (GM) and placed it through a managed bankruptcy. What many may not be aware of, is that the U.S. government also bailed out and took a controlling stake in Ally Financial Inc., formerly known as GMAC (General Motors Acceptance Corporation). Today that stake remains at ~74% and is even higher if one includes GM’s nearly 10% stake. To demonstrate the importance of Ally to GM, and now Chrysler (the other bailed out auto company), here is a pertinent portion of the 2011 Annual Report:

We financed 79% and 65% of GM's and Chrysler's North American dealer inventory, respectively, during 2011, and 78% of GM's international dealer inventory in countries where GM operates and we provide dealer inventory financing, excluding China.Given the enormous percentage, it appears Ally’s terms of credit are well below other market participants. While this strategy implicitly held a government backing prior to the crisis, it’s failure has now resulted in an explicit backing from the government (i.e. the public bears the risk).

We could argue over whether or not the federal government should be subsidizing credit at all, but I want to put that debate aside for the moment. If governments are set on encouraging investment and/or consumption through extension of credit at below-market prices, is the auto sector really the most productive use? Is it even close?

Whether or not the auto bailouts were a success, remains an open question for many. Unfortunately the costs associated with Ally Financial, especially the opportunity costs of credit, are often overlooked. Going forward, consideration of the success or failure of the auto bailouts must account for the ongoing costs of directing scarce resources towards that sector and future losses on loans. Hopefully these factors will also play a role in determining how long the current environment is allowed to persist.

Related posts:

Is the Return of Auto Subprime Lending and GM "Channel Stuffing" Connected?

Liberals Demonstrate Conservative Bias for Manufacturing

An American Icon Returns

What exactly does non-revolving credit mean in terms of not paying it off eventually. The quote seems to suggest that the Federal Government can not really expect the non-revolving debt to be paid off, which seems to imply the car and student loans are effectively a gift that doesn't need to be repaid. Am I missing something there?

ReplyDeleteThe short answer is nothing. From investopedia:

DeleteThe two classes of credit covered are revolving and non-revolving credit; revolving credit can be increased by the consumer up to a limit without contacting the creditor (as in credit cards), while non-revolving terms are fixed at the time the loan (as with an auto loan).

To date, the government has been reluctant to provide revolving credit (although one might argue the FHA, Fannie Mae and Freddie Mac have revolving credit lines). So the focus on non-revolving credit is mainly used as a distinction of government lending currently.

The aspect of non-repayment is not directly related to non-revolving versus revolving types of credit but rather stems from an assumption about markets. Any market participant, private or public, willing to provide credit (loans) at prices below most (all) others across the credit-worthiness spectrum is likely to experience larger losses than would otherwise be the case. Default rates are highly pro-cyclical, so when the next downturn occurs, one should expect Ally Financial (the government) to experience massive loan losses.

Not to delve too far into the topic currently, but student loans present a different type of dilemma since default is virtually impossible. On Facebook yesterday a friend was ecstatic about having the start of her student loan payments pushed out a year and the length of repayment extended. In real terms, the government is taking a small loss based on these actions. Multiply the loss over millions and the sum is no longer insignificant. There are potential benefits from these actions too, as well as distributional issues, but I'll leave those for another day.