While the implementation of capital controls presents an interesting storyline, Paul Krugman has raised a much bigger question into the public spotlight. After being challenged to expand the boundaries of political possibility, Krugman offered the following recommendation (emphasis added):

So here it is: yes, Cyprus should leave the euro. Now.

The reason is straightforward: staying in the euro means an incredibly severe depression, which will last for many years while Cyprus tries to build a new export sector. Leaving the euro, and letting the new currency fall sharply, would greatly accelerate that rebuilding.

The question for Cyprus is therefore whether “internal” or “external” devaluation offers the best prospects for the future? Let’s consider both of the options...

“Internal devaluation” (i.e. income deflation) - In return for continued assistance from the Troika (EU/ECB/IMF), Cyprus has agreed to impose losses on equity and debt holders, as well as uninsured depositors, of the two largest banks (Bank of Cyprus and Laiki Bank). This marks a distinct change in policy, especially with regard to the latter two groups.* Since uninsured depositors held a majority of those banks’ liabilities, the focus has naturally been on that group. Based on recent estimates uninsured depositors in the Bank of Cyprus may lose approximately 40%, while Laiki Bank’s uninsured depositors will be entirely wiped out.

The sharp reduction in (perceived) wealth stemming from these actions will put severe downward pressure on national income. Individuals and businesses experiencing losses will try to increase saving by reducing spending. Banks fearing deposit flight and falling asset prices will try build a stronger base of capital by restricting the supply of credit and possibly selling assets. Adding to the fall, the government will be forced to accept a MoU (Memorandum of Understanding) that establishes policies to increase taxes and reduce spending. Combining these deflationary pressures, the overall economic results may rival (or exceed) Greece’s recent history.

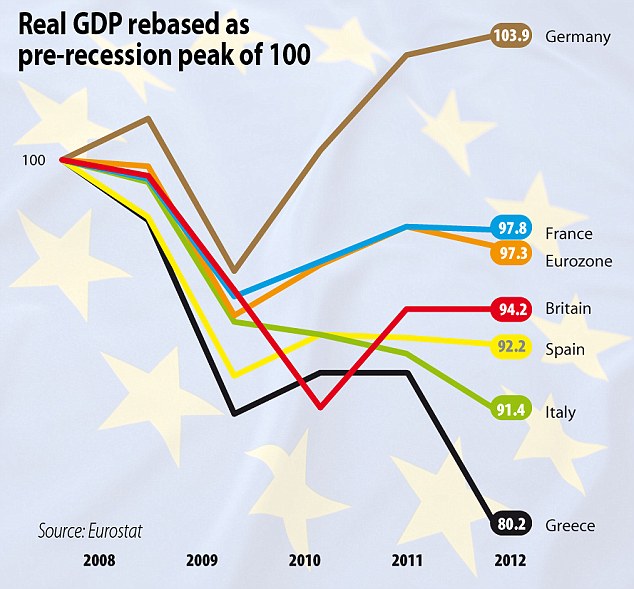

During the past 5 years Greece’s real GDP has declined by 20%

and unemployment has nearly quadrupled from ~7% to ~27%.

To offer some historical perspective, US unemployment during the Great Depression peaked at 25% and real GDP loss only exceeded 16% for one major European nation (Austria). Perhaps even more disheartening than the current data is recognition that output and unemployment appear unlikely to improve anytime soon.

Returning to Cyprus, unemployment has already quadrupled over the past 5 years (~3.5% to ~14%; shown above). Based on current estimates of a 20-30% drop in real GDP, Cyprus’ unemployment rate could easily approach or eclipse Greece’s in the next few years.

“External devaluation” (i.e. new currency) - If Cyprus were to leave the Eurozone, one of the first actions would be re-introducing the Cypriot pound at a heavily devalued rate against the euro. Not unlike the imposed losses on uninsured depositors, currency devaluation immediately imposes significant losses on all depositors. In this sense the impact on private demand would still be extremely deflationary, perhaps even more so. Though output and employment would fall dramatically, external devaluation presents reasons for potential optimism on both the foreign trade and government fronts.

Based on the recent bank losses and capital controls, Cyprus can no longer rely on its financial sector to support exports. By heavily devaluing its currency, Cyprus would be increasing its price competitiveness on the foreign market. However, as Barkley Rosser points out:

even with large elasticities [of trade relative to the exchange rate], there is the J-curve effect. Exports do not increase immediately, whereas the value of imports tends to jump up immediately with their price increases.Aside from these timing issues, there is also a concern regarding the certainty of each effect. A large devaluation will definitely raise the cost of living for Cypriots but as JW Mason comments, it:

might not lead to higher net exports in the next few years, or ever. That’s the question -- not how big the devaluation would be, but how strongly it will affect trade flows.

As for the government sector, returning to the Cypriot pound would remove some of the current fiscal constraints. This would permit the government to increase spending (ideally investment in a new export sector) and not raise taxes, raising private sector income. While these adjustments will not come remotely close to overcoming the other deflationary effects in the short-run, the counterbalance provided will be a significant improvement over current policy.

While this devaluation might make it easier for Cyprus to recover several years down the road, that recovery would indeed be several years down the road, and in the meantime there would be a lot of pain for the entire citizenry that will not happen if they stay with the euro.

If Greece has taught us anything about remaining with the euro, it’s that a lot of pain for the entire citizenry will happen regardless and a recovery may be decades down the road.

Cyprus is therefore faced with a choice between two terrible outcomes:

1) Remain in the Eurozone and experience a relatively slower “internal devaluation” whereby real output and employment experience large declines spread out over several years. A potential recovery is pushed even further into the future.

2) Leave the Eurozone and experience a quick “external devaluation” whereby real output and employment fall dramatically in the next year or two, but a recovery several years down the road becomes far more probable.

is that the real real issue here has to do with time preferences. It may get down to hyperbolic discounting. People do not want to have pain in the near term. So, the fear by the whole population of near term pain in terms of standard of living may outweigh fear of a more gradual decline with rising unemployment, even though the shorter term sharp pain is likely to lead to a sooner turnaround to growth.

Although this psychological tendency is very normal, it can at times be detrimental to achieving longer-term goals. The cases of Greece, Spain, Italy, Portugal, Ireland, and now Cyprus are examples of such times. The severe pain of reduced standards of living and high unemployment will be felt one way or another, but the option of “external devaluation” offers potential for a better future five and ten years down the road. Therefore I concur with Krugman, “Cyprus should leave the euro. Now.”

* From my perspective, imposing losses on debt holders should have been done from the outset in the US and Europe. The apparent change in policy may raise costs of debt financing for the largest banks, but that should be a welcome change after years of enjoying a TBTF subsidy.

"The severe pain of reduced standards of living and high unemployment will be felt one way or another, but the option of "external devaluation" offers potential for a better future five and ten years down the road."

ReplyDeleteI think Cypriots would also want to consider not just the near term and 5-10 year time frames, but also what might be best for their children and children's children. No clean and simple answers here.

Completely agree. I didn't mention that aspect primarily because I think it's too difficult to even make judgments regarding that long of a time period given the current circumstances. It should definitely be kept in mind though.

DeleteSo the better choice is probably leaving but our desire to avoid immediate sharp pain may get in the way of them making the optimum choice.

ReplyDeleteI tend to agree that this is a better outcome in making debtholders take losses than the US and Europe. Yet doing the kind of analysis you did for staying in the Euro or leaving would we Americans for example have felt more or less pain going the Cyrprian way and wiping out the debtholders-aside from the ethical pleasure that they got what they deserved?

I think the US would be much better off today if the insolvent banks had been taken over, written off the bad debt and then been sold off (so basically FDIC resolution authority). Unlike the Cypriot banks, even Citibank and Bank of America had enough good assets to cover practically all depositors (both insured and uninsured). The banks did not have the funds to cover a large chunk of outstanding debt. Had this happened, the govt could have written down mortgages to reasonable levels as a form of middle class stimulus. Then, when the banks returned to the market, the capital position would have been much stronger, making the banks more likely to lend. By recapitalizing "zombie" banks, mortgage debt remains high and new lending remains low.

DeleteWhat's not clear to me is why are capital controls required? Has the ECB already hinted that they will not provide liquidity (i.e. the banks are deeply insolvent)? Is the Cypriot government just biding time until they are forced to exit (and trying not to make matters worse by having to default on Target2 debits as well)? Are the banks in worse shape than recognized?

ReplyDeleteThe reason the crisis came to head at this time is because the ECB claimed it would no longer provide liquidity via the ELA to the Bank of Cyprus and Laiki bank (they were insolvent for a while but apparently the ECB reached its limit around ~10 billion euros). The reality is that many other Cypriot banks are sitting on large sums of Cypriot sovereign debt and Greek assets. The banks will eventually take substantial losses on these investments which brings their solvency into question. If the ECB will not provide unlimited liquidity than depositors are better off pulling their money and asking questions later. This is precisely why capital controls are currently necessary.

DeleteWithout controls there would be a massive run on the banks. Since neither the govt or central bank can print euros, the capacity to provide liquidity or bank insured deposits basically falls on the troika.

A good question is whether or not the ECB would follow through on not providing liquidity were bank runs to occur. My guess is they're bluffing, but its certainly a high stakes game of chicken. In previous instances it may have been beneficial for a govt to wait for more bailout funds before leaving but I think Cyprus is different. The losses sustained by depositors are enormous compared to GDP, which means the drop in employment will likely be massive. Therefore, for Cyprus, it may be better to get out sooner rather than later.

Hi Woj. I ran across this post at Fictional Reserve Barking, and I just have to ask: is Albert Wojnilower any relation to you?

ReplyDeleteI hope you are well.

Art

Hey Art,

DeleteYes. Al Wojnilower is my grandfather. There was an article in the FT "Last Word" column two days ago discussing a 1980 paper of his as well. In the future I hope to discuss some more of his work.

Separately, sorry for being away from blogging and commenting for a while (though I have been reading your stellar work!). School, work, and getting married, among other things, have taken up most of my free time. I hope to be back this fall though.

Take care,

Woj

In US there are a lot of people who have debts and the finance situation is unstable. People don’t have enough money for living. On Cyprus there are many unemployed people. And it isn’t possible to take out small loans for people with limited income. Poor cypresses have no opportunity to be sure that tomorrow all will be fine. I hope that in future the finance situation will flatten out and the countries won’t leave the euro. There are a lot of countries what are on the measure of leaving EU and which need the help, cause leaving EU is the crash for every country.

ReplyDelete

ReplyDeleteGOOD

Nice Post thanks for sharing with us....For more informattion click here-

ReplyDeleteSBCGlobal password reset

forgot SBCGlobal password

reset SBCGlobal password

recover SBCGlobal password

reset SBCGlobal email password

recover SBCGlobal email password

reset SBCGlobal mail password

forgot SBCGlobal email password

Brighthouse password reset

forgot Brighthouse password

reset Brighthouse password

recoverBrighthouse password

recover Brighthouse password

reset Brighthouse email password

recover Brighthouse email password

reset Brighthouse mail password

forgot Brighthouse email password

aol password reset

forgot aol password

reset aol password

recover aol password

reset aol email password

recover aol email password

reset aol mail password

forgot aol email password

Bellsouth password reset

forgot Bellsouth password

reset Bellsouth password

recover Bellsouth password

reset Bellsouth email password

recover Bellsouth email password

Thank you very much for writing such an interesting article on this topic. This has really made me think and I hope to read more.@ Packers and Movers Ahmedabad

ReplyDeleteI'm so gobbling up this stuff is mulling over the web, and your post truly persuaded me. You ought to get the bearing you gave at home. Possibly the guest presence will be a boggling one. If you have some problem with Hp Printer Offline click the link.

ReplyDeleteExcellent article. Keep writing such kind of information.

ReplyDeleteIf you have any issues related QuickBooks like Change QuickBooks Password, Download QuickBooks File Doctor, and QuickBooks

Error Code then click here

Change QuickBooks Password Online

Change QuickBooks Password

Forgot QuickBooks Password

Reset QuickBooks Password

Recover Forgot QuickBooks Password

QuickBooks Error Code 9000

QuickBooks Error 9000

QuickBooks Payroll Error 9000

QuickBooks Payroll Connection Server Error 9000

QuickBooks Payroll Error Code 9000

to resolve all the issues related QuickBooks.

Hi,

ReplyDeleteIt was a beautifully drafted travelogue, I want through. The craft of words impressed me thoroughly. Three cheers! If you want to have a look at a Free Daily Horoscope, click here.

Nice Blog , get more information about QuickBooks solution at

ReplyDeleteQuickBooks Customer Service

Thanks for the Post. It was very helpful and informative. Keep it up.

ReplyDeleteWith AT&T Customer Service, users can remove all their technical glitches without any issue. The techies solve the issues of ATT Mail Login, account recovery, etc with ease. Make sure to speak to the ATT team via the helpline number to get precise technical solutions. Get in touch with the techies any time of the day.