Paul Davidson: “Lars, there is a difference between the uncertainty concept developed by Keynes and the one developed by Knight.

As I have pointed out, Keynes’s concept of uncertainty involves a nonergodic stochastic process . On the other hand, Knight’s uncertainty — like Taleb’s black swan — assumes an ergodic process. The difference is the for Knight (and Taleb) the uncertain outcome lies so far out in the tail of the unchanging (over time) probability distribution that it appears empirically to be [in Knight's terminology] “unique”. In other words, like Taleb’s black swan, the uncertain outcome already exists in the probability distribution but is so rarely observed that it may take several lifetimes for one observation — making that observation “unique”.

2) What’s Driving China’s Real Estate Rally? Part 3 by Patrick Chovanec

By anticipating future demand growth, investors effectively front-load that growth into the present. That’s great for developers, who get to sell more today, but it means that a great deal of future demand has already been provided for and priced into the market. We see this phenomenon in other markets as well. In the West, many investors want to buy into high-growth companies like Apple or Facebook. What they don’t realize is that, to the extent they’re paying a high price-to-earning (P/E) ratio, they’re paying for that growth up-front, with the benefit accruing to the present-day seller, not the new investor. Even a genuinely promising company can have an overpriced stock.

The imbalance in real income growth I mentioned earlier exacerbates this phenomenon. The proceeds of inflationary money creation are channeled to favored recipients, often in the form of “hidden” income. These high income earners, in need of a place to stash their cash, pour it into property, in anticipation of future demand. The more money is created through expansive credit, the more cash they have to stash. In the meantime, the inflation that is generated boosts the nominal wages of low-skill workers, but erodes their real income growth, which is the basis for growth in future housing demand. Excessive money growth inflates the price that investors are willing to pay today, and lengthens the amount of time it will take actual homebuyers to come to afford that price. In other words, it creates a bubble.

As I noted before, rising incomes mean that current housing prices will become gradually more affordable — but only if they stop rising. If the market has to depend solely on end-user demand, there is a catch-up period ahead, in which incomes gradually rise to meet anticipatory prices, and investors gradually sell their stockpiled apartments to actual residents. The only way to avoid this catch-up period would be for investors to continue fronting for future demand by expanding their holdings even further. Many believe this will happen. In fact, if you think about it, this is really the main rationale behind calls for the government to lift restrictions on multiple home purchases: only investment demand, in the form of renewed stockpiling, can save the day.”3) GM's Channel Stuffing Goes To Germany: Is Europe's Largest Economy A Fraud? by Tyler Durden

Via Reuters: “So while official figures show a 0.7 percent rise in German car sales for the half year, figures from auto market research firms Dataforce and BDW Automotive show private demand fell 5 percent in the period, which would mean all the growth had been manufactured by the manufacturers.”

…

"If you push at the end of one month, you start the next one in deficit because you've registered a car you still have to sell," he said. And when dealers can no longer keep it up, carmakers do it themselves. As a result, the two account for a combined 30 percent of the new car market, making the industry the second largest source of demand behind only private customers, who account for 39 percent.”

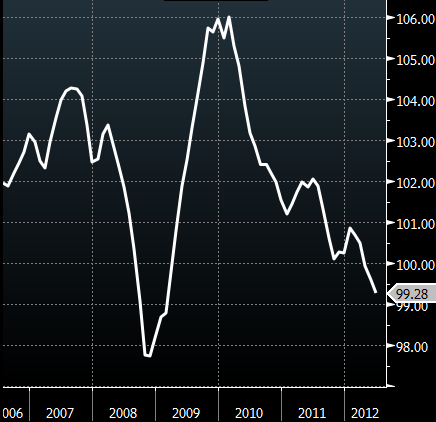

4) China's index of leading indicators points to further economic erosion by Walter Kurtz

The Index of Leading Indicators hit a post-2009 low today,

|

China National Bureau of Statistics Leading Indicators Index, 1996=100

|

*

*5) Imposed versus Adopted Monetary Rules by Steve Horwitz

Put differently, a policy-guiding rule is adopted by the central bank; a policy-constraining rule is imposed on the central bank. Their purposes are very different.

It is in this sense that Friedman opposed discretion and those in favor policy-guiding rules do not. Friedman’s rules are not changeable by the central bank itself; policy-guiding rules are. The central bank has discretion to pick its “rule.” That, Friedman thought, was the whole problem, hence his call for a rule to be imposed.Woj’s Thoughts: Horowitz hits on a key aspect of the rules vs. discretion debate by explaining that some “rules” intentionally leave open vast space for discretion. Applying a rule to fiscal or monetary policy, such as full employment, does not imply that Keynesians (or any other economists) prefer rules to discretion. On the contrary, the choice to allow policy makers substantial discretion in meeting such “rules” suggests discretion is preferable.

No comments:

Post a Comment