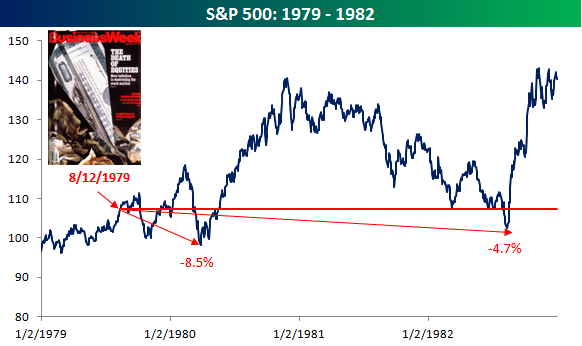

Just how good of a buying indicator was the BusinessWeek cover from 1979, though? If you ask most investors about that cover story, they seem to remember that the market almost immediateley took off after the issue was published. The reality, however, is that nearly eight months after the cover story was published, the S&P 500 was down 8.5%. While the market did rally from that level, three years after the infamous BusinessWeek cover, the S&P 500 was still down nearly 5%. It wasn't until 8/12/82 that the S&P 500 really took off and the bull market began in earnest. Granted, time horizons have gotten a lot shorter in the last thirty years, but three years is an eternity in this market.

Woj’s Thoughts - Our memories can deceive us by filling in stories with logical steps. Cover stories often do mark extremes in sentiment, yet those extremes may persist for quite some time. As a signal for contrarian investors, recognizing this reality is critical.

2) Why I don’t believe housing has put in a secular bottom by Edward Harrison

For the bottom to be in you have to believe two things from a macro perspective. First, you have to believe that the overshoot phase to the downside has been arrested. Most bubbles end with a significant overshoot that makes it a no-brainer to tip a toe in the market. I think we are approaching those levels in markets like Phoenix. But we never really got down to reasonable levels in places like Washington or New York. Second, you have to believe any US recession is both remote in time and mild in duration/severity. I question this. I think any US recession will re-start the house price decline dynamic because consumers are still overindebted, interest rates are at zero percent, and mortgage rates are as low as they can get. My point is that from a cyclical perspective 2012 is as good as its going to get. Calling a bottom at the top of a cyclical bull market in asset prices and the economy is folly. Wait until the bottom of the cycle to make those calls.Woj’s Thoughts - Early this year I made the claim, Don't Rush to Buy a Home! At the end of May I was Still Not Buying A Housing Recovery. Edward lays out many/most of the reasons for my continued lack of optimism on housing prices over the next couple years.

3) The Evolution of Treasury and Muni Bond Yields by Cullen Roche

I’ve discussed this in detail over the years and why the analysts crying for mass US state insolvencies were likely to be wrong, but now we have some interesting new analysis via VOX. What’s depicted below is the 10 year US Treasury versus the 10 year muni bond index. As you can see, the yields have an extremely high correlation – muni bonds practically ARE treasury bonds. So why are yields surging in Italy, Spain, Greece and Portugal, but they’re remaining so tame in the muni market? Simple – the US government, which can always procure funds via taxes and bond sales therefore making solvency a non-issue, provides substantial federal aid to the states every year. While this doesn’t eliminate the solvency issue at the state level it certainly helps reduce it substantially. Europe has no such mechanism in place so what you basically have is a bunch of US states in an environment where they’re left to fend for themselves. They can’t print their own currency, they can’t devalue their own currency and they can certainly run out of Euros. The result is bond investors who are terrified about default and end up selling bonds which only exacerbates the budgeting process.*4) Microfoundations and the capital debates by Matias Vernengo

In that sense, heterodox (classical-Keynesian, by which I mean Sraffa’s prices cum Keynes/Kalecki’s effective demand) does have a coherent determination of long run prices, based on rational behavior, as the foundation of the macroeconomic theory. Markets do not produce optimal outcomes and unemployment of productive resources is the normal, long run, position of the economy. In fact, the capital debates not only say that classical political economy (the surplus approach) provides sound microfoundations, but also that it is NOT possible to do so within the neoclassical/marginalist paradigm.Woj’s Thoughts - Previously I’ve argued against microfoundations in macroeconomics, but Matias places an interesting spin on the discussion. Quite possibly the issue is not the use of microfoundations but rather the poor choice of microfoundations.

5) Another Summer of Discontent: The Four Factors that Explain Why What We’re Doing Isn’t Working by Daniel Alpert

We must move from stabilize and reflate, to stabilize and recalibrate:

- It is time for creditors throughout the developed world to finally take the write downs that have long been coming their way in connection with the trillions of dollars of truly un-payable household and sovereign debts that resulted from the credit bubble of the 2000s. Yes, this will pressure lenders and, yes, they will need to be recapitalized to the detriment of their existing stakeholders. But there is presently no shortage of capital seeking reasonable risk-adjusted returns, and I have every confidence that it will flow eagerly into the financial sector—if only the balance sheets of our institutions were honestly reckoned by having the currently unrecoverable carrying value of assets written down to that which can be recovered today from borrowers and/or underlying collateral.

- As I have been saying and writing about for years, we must accept the reality of what the credit markets are telling the planet’s most creditworthy governments, particularly that of the U.S. The message is “please, here, take our money…take it cheaply and keep it safe…we have no fear of lost purchasing power, the trend is not inflationary…now take it (and use it to fix your economy).” And that is what we must do. We must take as much 30-year money at these depression level interest rates as we need to re-employ our underemployed workers directly, on public infrastructure projects that return benefits to the economy more than sufficient to repay the sums borrowed when the time comes. The private sector will not hire until it sees a recovery in demand—so the only agent for re-employment of workers and regeneration of demand may, for an extended time until the imbalances at least decline somewhat, be our governments. It is long past time to pack away austerity agendas.

- And yes, we must address and manage the process of nominal price, wage and asset value declines. The advanced economies are experiencing the effects of a supply glut, a debt overhang, massive technology-induced productivity (soon to transfer to the emerging economies, worsening the glut), and aging populations. These are all disinflationary factors. And the aggregate effect of their contemporaneous existence is deflationary—full stop. Yet in relying on monetary intervention alone we are fighting the battle to control the pace of deflation (forget about reflation) with one hand tied behind our back.n Instead of targeting growth in nominal GDP, which I am proclaiming here to be a futile endeavor, we must target renewed global competitiveness and, at the very least, growth in real GDP. That means both allowing our price and wage structures to align themselves with global supply and demand and, more importantly, feeding and nurturing investment in those areas of the private sector that can employ large numbers of people at market clearing wage rates. Especially in those sectors that are more readily protected by geography from global competition.

No comments:

Post a Comment