His conclusion is:

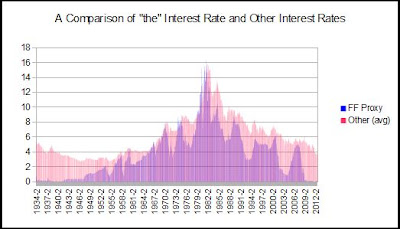

Wouldn't it be simpler to allow that maybe long rates are not, after all, set as "the sum of (a) an average of present and future short-term rates and (b) [relatively stable] term and risk premia," but that they follow their own independent course, set by conventional beliefs that the central bank can only shift slowly, unreliably and against considerable resistance? That's what Keynes thought.So apparently the Fed doesn’t control interest rates. Well, hold on a moment. Not long after Mason’s post, The New Arthurian Economics responded with But why, JW? Why "The past 25 years"?? As you’ll note, the above chart only considers rates back to 1987. Using some clever data mining and chart altering, Art comes up with the following historical look at the Fed Funds rate versus an average of other market interest rates:

Once again, it appears that rates are not following the Fed as closely as one might expect.

Responding to both Mason and Art, in the comments, I offered my own answer to the question. In short (you can read the full comments if you choose), market expectations of future Fed action are sticky. During the post-war period until about 1980, inflation was consistently rising despite mainstream economic views that suggested those conditions would not persist. Following a lengthy inter-war period of near rock-bottom interest rates, market participants were slow to adjust expectations to the actual height of interest rates that would occur before sustained disinflation began. Once disinflation began in the early 1980’s, market expectations were equally slow in recognizing how long disinflation could persist and therefore how low the Fed would ultimately take rates (and hold at zero).

Contrary to this expectations based view, Jazzbumpa, of Angry Bear, countered with a link to his previous post on Who Determines Short Term Interest Rates? His conclusion, supported by various graphs:

The Federal Funds Rate, which is set by the Fed, FOLLOWS 3 month T-Bill rates. It does not lead the economy.This leads to two important questions on the subject:

1) Does the Fed have any real power to influence interest rates?2) What would happen if they attempted to move counter to the market?These questions have plagued me for the past few weeks, but I think I’ve found the answer.

As I pointed out in one my comments:

The Fed acts in certain intervals and operates under a corridor system. In this manner, the Fed sets the target rate but permits fluctuations within a band between the discount rate and IOR rate.Now let’s imagine that during an interval between FOMC meetings, private credit expansion is causing banks to demand more reserves. Absent open market operations that increase the supply of reserves, the Fed Funds rate will move higher towards the upper bound of the targeted range. Witnessing this change, the Fed can choose to respond by either expanding the supply of reserves to maintain its current policy rate or by raising the rate to match the “market-determined” interest rate. The same principle would apply in reverse to a decline in demand for reserves. In this manner, the Fed FOLLOWS the market in supplying reserves and setting the Fed Funds rate.

Not surprisingly, the story above complements the paper by Scott Fullwiler “Interest Rates and Fiscal Sustainability”, which notes:

“More recently, Fullwiler (2003) and Lavoie (2005) have demonstrated that the central bank’s obligation to promote the smooth operation of the payments system means that the provision of reserve balances are necessarily non-discretionary. (p.12)”After much thought, I’m willing to concede that the Fed primarily acts (or has acted) passively in setting short-term rates. This view, however, does not entirely undermine the expectations theory for long-term interest rates or the Fed’s ability to control interest rates. If market participants are aware that the Fed reacts to market moves, then future expectations regarding a “market-determined” interest rate provides a reasonable proxy for the Fed Funds rate. Separately, the Fed could announce a ceiling on long-term Treasury rates and dare the market to test its resolve. Therefore, I accept that in practice the market determines interest rates, but retain the view that operationally the Fed could control interest rates.

A real test of the Fed’s power to manipulate interest rates would require the Fed to either act counter to the market or cap specific rates along the curve. Although the latter seems more likely than the former, I don't expect either action to occur anytime in the near future. Considering central banks outside of the Fed, the ECB may soon provide a real-world experiment by setting a ceiling on rates. Though the EMU holds stark differences with the US monetary system, it will be enlightening to witness a central bank truly take on the markets. This debate is far from over...

Note the difference between suggesting that the Fed can set rates where it wants and whether or not it does. It most definitely CAN set the rate given that it has an unlimited capacity to purchase, or that it can enter into any market of any maturity and offer to borrow/lend at a rate (or a spread, where applicable) that it names. Obviously, aside from the fed funds rate it hasn't chosen to actually set a rate directly.

ReplyDeleteNonetheless, I still think that the expectations framework with a premium and a few technicals (convexity, etc.) explains long-term Tsy's the best (and obviously there are some other factors at work in the non-Tsy markets)--and Kregel has shown a few times this is quite consistent with Keynes--not to mention that finding that the fed funds rate lags the tbill is exactly what the expectations theory would say happens (tbill's a longer maturity, after all). (Note also that in your graph, the only time there is a significant difference b/n fed funds rate and longer rates (and I don't know if the longer rates are only Tsy's or not, and if not then the point is moot) is before the early 1950s, during which time the Fed did directly set long-term Tsy rates until the Tsy/Fed Accord relieved the Fed from this duty.)

Regarding the fed funds rate, one must recognize that there is no role at all of price discovery in the market for central bank balances--this is not a controversial point at all in the literature on the details of central bank operations. So, even if it is the fed funds rate following the lead of the tbill, it's because the Fed chooses to do it that way (and it wouldn't surprise me if that were how the Fed made its choice, but that doesn't mean it has to).

Best,

Scott Fullwiler

I agree with Scott F.'s first paragraph. It's important to distinguish between the capability of central banks *in principle* to control interest rates on debt denominated in their own currency, and the extent to which conventional monetary policy has actually done so.

ReplyDeleteI am not sure about the second paragraph. In particular, while I'm not sure what specific article of Kregel is being referred to, I think the claim that Keynes believed that the central bank could control market long rates by setting short-term risk-free rates is unambiguously false. in fact, the relative inelasticity of long rates with respect to the policy rate was central to Keynes' thought, and arguably *the* motivation for fiscal policy in his theory. I follow Leijonhufvud in this, but it's enough to read Keynes.

I agree that central banks can in principle exercise much more control over the whole rate structure than they have historically done in practice. (Except in wartime, when the problems are different.) And that more influence wouldn't come without costs. I suspect that there is a floor on long rates -- perhaps not so much lower than current rates -- that if the Fed wanted to lower rates below, given the current institutional structure of the financial system, it could only do so by displacing all private intermediaries from the credit market, i.e. by buying up essentially all private debt.

(in other news the anti-spam filter here almost defeated my human pattern-recognition capacities. On my own blog I don't use these, I just accept that part of my job as blog-owner is to delete occasional spam comments.)

ReplyDeleteSTF and JW - Thanks for the comments...your input is greatly appreciated! (Also, I have removed the filter).

ReplyDeleteUnfortunately I am not enough of an expert on Keynes to know which way he leaned on this issue. If I'm not mistaken, I could envision a middle ground whereby Keynes believed that long-run functioned based on short-term expectations but were highly "sticky down." This would imply ineffective monetary policy during times of crisis and the motivation for fiscal policy. (Hopefully I haven't completely misinterpreted each of your views).

"I think the claim that Keynes believed that the central bank could control market long rates by setting short-term risk-free rates is unambiguously false."

ReplyDeleteNot what I said. What I said was that the expectations theory as I suggested should be adjusted (term premia plus technicals like convexity, etc.) is a good explanation of long-term Tsys (Mason's graph has far more than that as it includes non-Tsys) is consistent with Keynes (I said "quite consistent" but more appropriately should have said at least partly consistent--apologies for that, as Keynes's explanation was more conditional and his TOM was also written in a gold-standard setting). Note that there's nothing in there that should suggest I argued that "the central bank could control long rates by setting short-term risk free rates."

"in fact, the relative inelasticity of long rates with respect to the policy rate was central to Keynes' thought, "

Again, that's conditionally consistent with the expectations approach I'm suggesting, at least for long-term default risk free.

Bad economic conditions is getting worse because of Obama monetary policy as discussed by Ed Butowsky in Fox Business.

ReplyDelete

ReplyDeleteتعد شركتنا افضل شركة صيانة مكيفات بمدينة جدة حيث توفر لكم الشركة خدمات ممتازة وراقية

شركة صيانة مكيفات بجدة

بالاضافة الي قيام الشركة بعمليات التنظيف علي اكمل وجه ونقدم لكم خدمة تنظيف المكيفات بشكل راقي جدا

شركة تنظيف مكيفات بجدة

ونحن كاسم كبير نقوم بخدمات كشف التسربات بمكة ونقوم بالعمل بافضل الاجهزة ونمتلك افضل الفنيين المتخصصين

شركة كشف تسربات بمكة

كما يتوافر في الشركة خدمات العزل بكل انواعها واحجامها وتعد ايوان افضل شركة عوازل بجدة لما توفره لعملائها من خدمات علي مستوي عالي وراقي جدا

شركة عوازل بجدة

فى شركة العربى نقدم خدمة شركة تنظيف بحائل ان النظافه هى من اكثر واهم الامور التى قد تعفى الانسان من الامراض الكثيره لذلك شركة العربى تسعى دائما ان تقدم جميع اعمال التنظيف الى عملائها الذين يثقون بها

ReplyDeleteشركة تنظيف بحائل

كما تقدم افضل الطرق الحديثه وتوفر لهم الراحه التامه وعدم المشقه فان شركتنا تسعد ان تقدم لحضراتكم افضل انواع النظافه العامه

شركة تنظيف فلل بحائل

وتحب ان تقدمها على اعلى مستوى من المستويات وفى نفس الوقت ان شركتنا لا تقبل المنافسه فى الاسعار حيث ان شركة العربى تعمل فى جميع اعمال النظافه فى حائل بارخص الاسعار وتقدم افضل العروض دائما لعملائها الكرام

شركة تنظيف مجالس بحائل

من أهم أسباب سعادة الانسان وبالأخص عندما يتعلق الأمر بكيف يبدو منزلك, فإن تطلعاتك وأحلامك تصبح كبيرة، فمنزلك هو انعكاس لك، ولهذا السبب أنت بحاجة إلى

شركة تنظيف منازل بحائل

شركة تنظيف رخيصة ومجربة وثبتت انها الافضل بين الشركات فنحن نقدم افضل خدمات التنظيف فى شركة العربى حيث نضمن لك عملية التنظيف بدون اى اخطاء لاننا نسعى دائما لنكون افضل

شركة تنظيف كنب بحائل

وهدفنا هو الوصول الى القمه وكل ذلك عن طريق ارضاء عملائنا وتحسين ثقتهم بنا والقيام بعملنا على احسن وجه ولدينا فروع اخرى فى مدينة جازان مثل

شركة تنظيف بجازان

فنحن نقدم لكم شركة العربى من الشركات المميزه والرائده فى جازان وهى تقدم تنظيف البيوت على احسن وجه كما تقدم تنظيف فلل وتنظيف شقق وتنظيف مجالس وتنظيف واجهات وتنظيف مسابح وتنظيف خزانات

شركة تنظيف منازل بجازان

وتقوم شركتنا بالاعتماد على احدث الالات وعلى افضل انواع المنظفات العالميه التى تعمل على ازالة البقع كما تعمل على ازالة الاوساخ بسرعه كبيره وتقوم بخدمات اخرى كثيره

شركة تنظيف مجالس بجازان

وكل ذلك نقوم به من خلال شركتنا شركة العربى بافضل الاسعار وارخصها التى تتناسب مع جميع الطبقات من العملاء والموظفين وغيرهم من الذين يقيمون فى جازان

شركة تنظيف كنب بجازان

Call +9711199012 Delhi VIP Escorts, Our Independent Female Escorts Services in delhi Will Make Your Every Moment Erotic With 100% Confidential. Book Celebrity delhi Call Girls

ReplyDeleteaerocity escorts

airport escorts

chanakyapuri escorts

charmwood village escorts

chattarpur escorts

chittaranjan park escorts

civil lines escorts

connaught place escorts

cr park escorts

defence colony escorts

green park escorts

ReplyDeletegtb nagar escorts

hari nagar escorts

hauz khas escorts

chirag delhi escorts

crossings republik escorts

indirapuram escorts

Noida Escorts, High Profile Call Girls In Noida For Unlimited Fun With Russian girls, Air Hostess,HiTech Co. Girls/Women,House Wife.

ReplyDeletepari chowk escorts

follow my twitter

noida city center escorts

botanical garden escorts

noida golf course escorts

noida film city escorts

atta market escorts

new ashok nagar escorts

noida sector 93 escorts

noida sector 137 escorts

Independent call girls in noida providing.The girls come from elite & high society; they highly trained to make much more pleasure.

ReplyDeletenoida city centre escorts

noida sector 15 escorts

noida sector 16 escorts

noida sector 18 escorts

independent noida call girls

russain escort in noida

follow my twitter

Full enjoyment with Saket escorts service,We are offer only for you Russian call girls Saket at variable price.If you want spend your best movement with our call girls.

ReplyDeletegreater noida escorts service **

saket escorts service **

rohini escorts service **

mehrauli escorts service **

vikas puri escorts service **

kapashera escorts service **

greater kailash escorts service **

uttam nagar escorts service **

janakpuri escorts service **

paschim vihar escorts service **

ReplyDeletenoida escorts $$$

call girls noida $$$

call girls delhi $$$

call girls udaipur $$$

call girls jpdhpur $$$

call girls indore $$$

https://sites.google.com/view/call-girls-service-near-hotel-/ ##

ReplyDeletehttps://sites.google.com/view/escorts-service-near-the-or/ ##

https://sites.google.com/view/call-girls-near-the-st-regis-m/ ##

https://sites.google.com/view/escortneartrident/ ##

https://sites.google.com/view/escortsnearhotelhiltopmumbai/ ##

https://sites.google.com/view/call-girls-near-itc-grand-cent/ ##

https://sites.google.com/view/escorts-near-itc-maratha-a-lux/ ##

https://sites.google.com/view/escorts-near-inter/ ##

https://sites.google.com/view/call-girls-near-hotel-bawa-con/ ##

https://sites.google.com/view/callgirlsnearjwmarriottmumbais/ ##