Whatever the case, we noted in May that while the pace of car sales in the US has picked up this year, it’s still much slower than for most of the past decade. More and more it’s clear that this is an ongoing rebound following the end of a depreciation cycle. (The pickup in lending activity is at least a sign of expected sustained demand in this sector, so there’s that.)This sounds plausible enough but my nature involves being skeptical. Let's consider a different thesis on the rise in subprime lending.

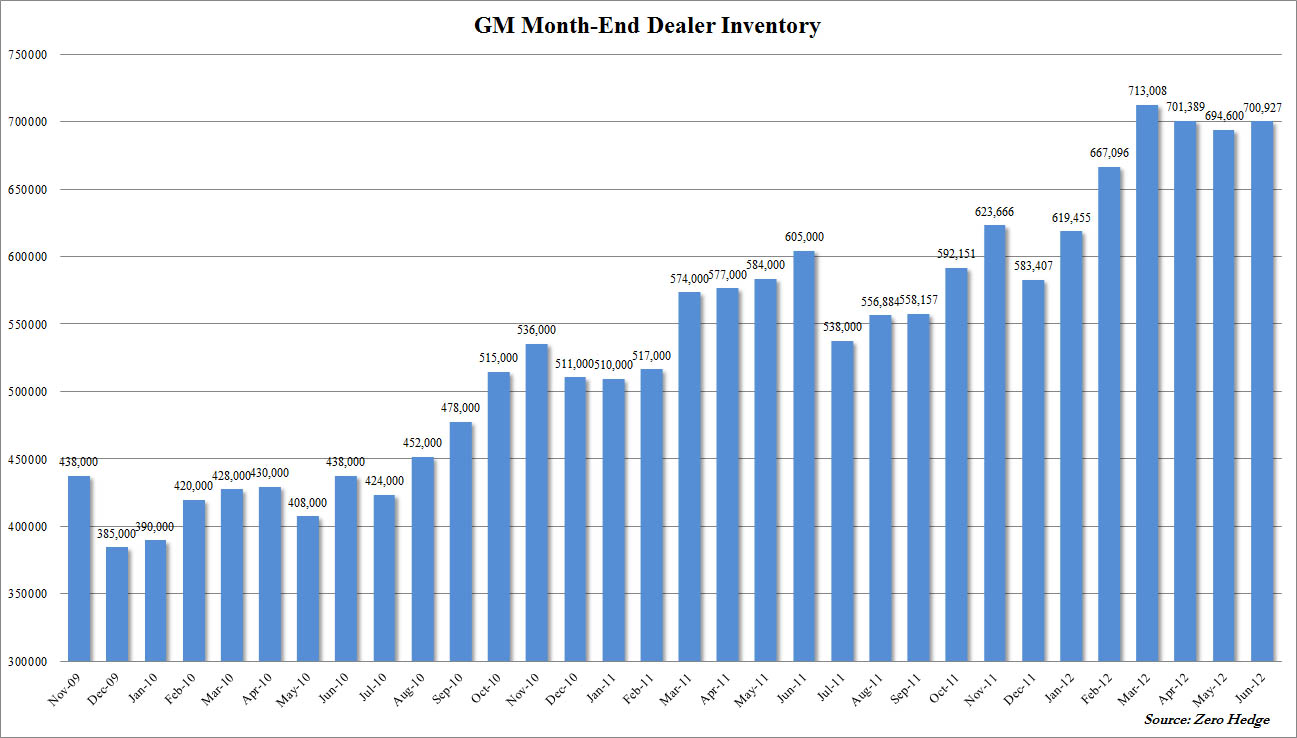

Over the past couple years auto manufacturers, namely GM, have been loading up dealer inventories to falsely promote higher sales. What many people may not realize, is that sales are booked when the cars are “sold” to dealers regardless of whether the dealers are able to sell the vehicle to end users. Here is a chart from Zero Hedge depicting the rise in GM dealer inventory:

This practice, known as “channel stuffing”, is actually part of a recent class action lawsuit filed against GM by investors. As the dealers are left with increasing unsold inventory, costs of storage are certainly rising. If sales to end users are not keeping pace with the desire of GM to unload inventory (clearly the case), one way to spur increasing end sales would clearly be lowering lending standards. The pickup in lending is therefore not a sign of expected demand but rather a means to increase demand. Is it possible the decline in credit quality of auto loans is a means to cover-up “channel stuffing” practices? If so, when subprime defaults eventually rise, who will be left with the losses?

No comments:

Post a Comment