This does boil down to a household income issue and consequently an employment issue (it always did). From 1997 to 2007 the bubble in home values did not reflect solid wage increases but a flood of easy to get loans where a pulse was the only requirement to buy. With all of that removed, we have had 5 million completed foreclosures and trillions of dollars of faux equity evaporated into thin air. Prices are back to levels last seen a decade ago and 10,000,000 homes are underwater with another 5.8 million in foreclosure or with at least one missed payment. All of this in spite of historically low interest rates and low down payment products like FHA insured loans.

Read it at Dr. Housing Bubble

What if housing doesn’t recover for another decade? When the young cannot afford to buy a home from their parents. The reemerging trend between the US and Japan housing bubbles.

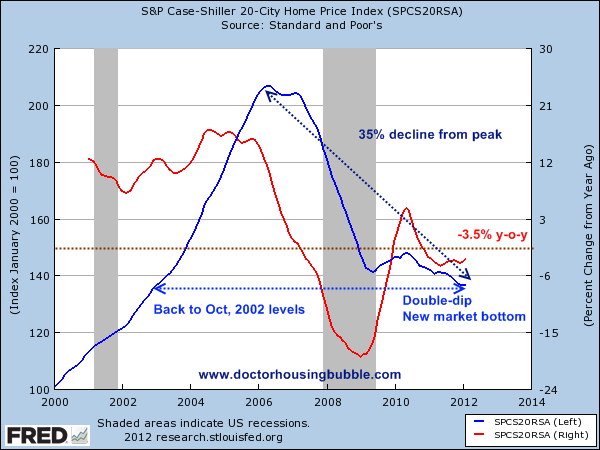

Three months ago I remarked, Don't Rush to Buy a Home! Today, prices are once again declining and mortgage rates have hit a new record-low. With the employment to population rate hovering at multi-decade lows, while wages and work hours stagnate, the picture for the next couple years isn’t looking any brighter.

When will be a good time to buy a home?

ReplyDeleteObviously much of that decisions depends on each individual's current financial situation and location. That being said, my base case is still another 10-20% decline in national housing prices. As for interest/mortgage rates, I expect rates to remain at or near current levels for at least a couple years. Mortgage rates could decline as low as 3-3.5% in the next couple years. Given those expectations, I think a better opportunity will present itself in 2-3 years.

DeleteThe big caveat in these expectations is government policy. If policy changed to either write-down significant mortgage debt or provide far more stimulus, the timeline would certainly change.