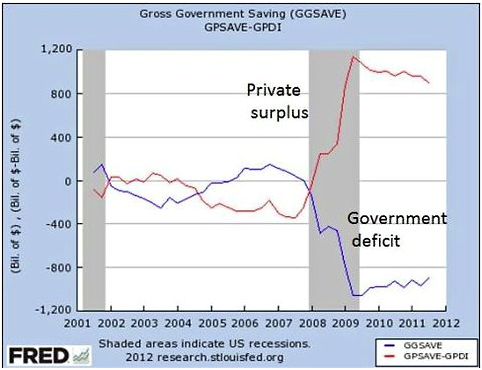

In any event, we’re in a balance sheet recession. We should be encouraging the private sector to borrow less, not taunting people with negative interest rates and encouraging them to leverage up. And we should recognize that the government’s deficit is the key to helping the private sector de-leverage.

Reducing the government’s deficit means cutting the non-government’s surplus, which frustrates their efforts to pay down debt.

We need rising incomes to support a recovery that can be sustained by private sector spending, and the Fed isn’t the agency we should be looking to for help on this front.Read it at Naked Capitalism

Can the Fed Really Do More?

By Stephanie Kelton

Kelton expresses her frustration, which I share, with the unrelenting calls for further “stimulus” from the Fed. As I’ve mentioned repeatedly on this blog (see here, here, and here for examples), the mechanism by which monetary policy can induce real growth is weak, at best, especially when the private sector is deleveraging. Despite the efforts of Kelton and many others with an MMT/MMR/Post-Keynesian background, this message has still not gotten through to the mainstream media. Hopefully our experimentation with monetary policy will not cause too much damage before its ineffectiveness is finally understood.

I feel really nice reading these articles I mean there are writers that can write good material more information

ReplyDelete