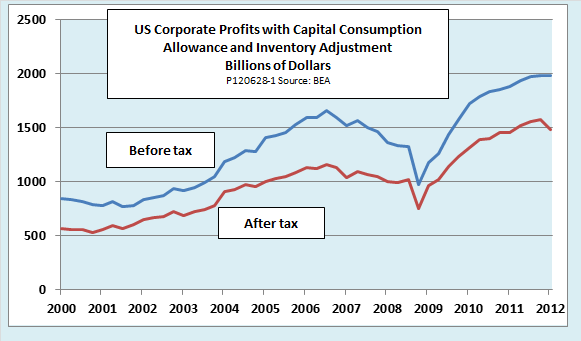

The BEA also released revised data showing that corporate profits in Q1 were weaker than previously thought. The broadest measure, corporate profits before tax with capital consumption allowance and inventory adjustment, decreased by 0.3 percent compared with Q4 2011. As the chart shows, that was the first decrease since profits hit their cyclical low in mid-2008. After tax profits with adjustments decreased much more sharply, by 5.9 percent. The difference reflected a whopping 20 percent increase in corporate profits taxes for Q1 2012 compared with Q4 2011.

The drop in corporate profits was largely due to weakness in the global economy. Domestic profits of U.S. corporations rose by a healthy 2.6 percent in Q1 2012 compared with Q4 2011 (5.7 percent for the financial sector and 1.4 percent for the nonfinancial sector). However, foreign profits fell by 12 percent, more than wiping out the increase in domestic profits, as receipts from the rest of the world fell and payments rose. (my emphasis)Read it at EconoMonitor

Latest Data Show U.S. Corporate Profits Falling Due to Global Woes while GDP Growth Remains Sluggish

By Ed Dolan

When the US housing decline began to create broader problems for developed economies, many people were quick to suggest that emerging markets had decoupled and would not be impacted by the developed world’s crisis. Despite those predictions being proven terribly wrong, as the current Eurozone crisis has picked up speed, the same individuals have been projecting the US will decouple and growth will be unaffected. Given the sharp decline in corporate profits, it appears decoupling proponents will once again prove mistaken. With S&P 500 earnings set to decline in the second quarter, this data suggests that current expectations of a minimal drop may still be optimistic. As Europe and China continue to slow, a turnaround in foreign profits is increasingly unlikely. It appears the US may already be in the midst of a profit recession.

Hi Woj! This is Mike Sax from Diary of a Republican Hater you commented on my blog yesterday.

ReplyDeleteAnyway I defintely like your blog and see it's going to be a great resrouce for me to better get my arms around monetary policy.

I read your piece about Operation Twist-hope the Fed isn't going to rest here but sounds plausible. Romney and company don't want anything that's for sure.

I'm really interested on your criticisms of Sumner's NGDP targeting regime. While I find him interesting I'm also skeptical of him. He's Friedman 2.0 as I like to say-but the first one was a sophist as well.

What I'm trying to figure out though is where you guys-the MMT/MMR PK crowd are relative to MM.

I mean I saw your piece about IOR being anti-growth and causing banks to hoard. I think it's true but this is also something Sumner never tires of arguing. So on this you actaully appear to agree with him and the MMers.

He also claims to not believe in the money multiplier either.

However, if I read you write in a post you wrote back in 2010 you seem to be saying that for the Fed to end IOR could be dangerously inflationary now. Do I have that right?

This is the link I'm referring to

http://bubblesandbusts.blogspot.com/2010/11/fed-stands-in-own-way-on-monetary.html

Here is the direct quote:

"As for the Fed, one has to question if the Fed will ever stop paying interest on reserves in the future. Doing so with current interest rates would likely spark a quick and enormous increase in the flow of funds throughout the global economy. Although this would likely spur economic growth it could also be expected to unleash painfully high inflation. If the Fed continues paying interest on reserves, future decisions to raise the Fed Funds rate above that paid on reserves may risk creating the same problems. For better or worse, the Fed must now consider a new set of variables when making policy decisions for the foreseeable future."

Are you saying the Fed shouldn't stop now? Is inflation really worse than the current status quo of stagnation and hoarding?

On the other hand the areas I see some difference with you and Sumner so far is QE. He seems to agree that it doesn't do much-he may even admit it's just swapping assets that are perfect substittues.

Yet he still seesm to think QE is very powerful via-you guessed it-the expectational channel and Nicl Rowe's "Chuck Norris Effect"

If you could explain your view about expectations-where the MMers say the markets "do most of the heavy lifitng"

Again like your blog and will visit often.

Mike,

DeleteThanks for the comments and kind words about my blog! I've been on vacation the past 10 days, so apologies for the delayed reply.

You read the post from 2010 correctly, although I think it's fair to say my views have changed and become more-informed since that time. As this point, I think that removing IOR would be practically the equivalent of a 25 basis point reduction in the Fed Funds rate. The profit/loss calculations for banks would change as shorter-term Treasuries would then pay slightly higher rates, albeit with slightly added risk. This could push banks to rotate into Treasuries until shorter-term rates become effectively zero, or even negative (similar to countries in Europe).

I haven't fully thought through this course of action, but ending IOR could put upwards pressure on interbank rates since parties would be less inclined to hold excess reserves. This could force the Fed to step in and actually reverse QE, providing banks with Treasuries (now in demand) and removing excess reserves (no longer demanded).

Based on this view, my expectation (now) is that ending IOR is unlikely to cause much, if any, inflation. In fact, if the above scenario played out, based on market expectations the Fed's actions might be viewed as contractionary.

As for where I stray from MMers on the expectations channel:

In my mind the expectations channel does exist, but is relatively weak and is especially ineffective when economic troubles stem from excessive private debt (balance sheet recession). Consumers have been relying on credit for spending, instead of cash, for several decades. The cost of money has therefore increased, due to interest costs, and household debt has continued to rise despite constant (low) positive savings rates.

By altering expectations for higher inflation, consumers are encouraged to spend/invest more money. This would be good if the extra spending flowed largely to incomes. Unfortunately, with high unemployment and a declining percentage of profits going to labor, most households will not see incomes rise nearly enough to cover the extra spending.

Separately, changing expectations has altered the price of net private financial assets, but not the quantity. As interest costs accumulate and debt rises, people will be forced to cut back on spending/investing in order to pay off the debt. This will reverse the asset price rises and shift greater sums of income to the financial sector (which thrives off the extension of credit/debt).

The result is that expectations for higher inflation (or NGDP) do not become self-fulfilling but actually fail to be met. IMO, this helps further the disparity in income and distribution of debt within our society as well.

Hopefully this helps clarify, to some degree, my views on these topics. The concepts have taken me thousands of hours of reading to grasp and my views/understanding still changes slightly most days/weeks.

PS - I'll respond to your other previous comment soon.

Thanks for the insights Woj! You are certainly a helpful resource for me who is also trying to grasp.

ReplyDeleteI think you're right that a negative IOR is nothing special and will have no effect. The key is the MMT insight that banks don't lend reserves so why would placing a tax on them make them lend them out-as they don't lend them out? Last week Europe took of it's IOR on deposits taking it to zero and there was no impact.

Sumner had to admit it didn't do anything but explained this by claiming the market didn't believe in it-that it failed to meet expectations for future policy moves.

I was not sure about MMT at first wondering if it were a cult. I don't like the attutide of all of them-some can be a bit snarky or strident. But I do think they have some important insights as does their offshott MR. I think Cullen Roche does a great job explaining this stuff about the modern monetary system.

Woj,

ReplyDeleteI'm not sure what the effects of suspending IOR's would be. It seems to me that the intent of the policy has been to allow banks to repair balance sheets with "free money." The problem is that balance sheets are not truly stated with the suspension of MTM (mark to market), regulations. There appears to be this conundrum with respect to interest rates and willingness by banks to lend: Rates are at such low levels, that banks don't think there is enough of a risk premium to lend, vs. taking the float on IOR's.

It is important for policy makers to be focused on restoring the health of the financial sector of the economy. The problem is that the policy seems to be all one sided. All the help is concentrated on the sector that caused the problem, with no relief for the sector that is suffering as a result of the bad behavior. I'm not optimistic that private sector debt will get a fair shot at redemption, (debt forgiveness), if Republicans gain the upper hand politically, in November.

Mike - I went through the same experience with MMT, as have many others. Personally I think the key is to recognize that various schools of economics can offer value and to figure out which aspects of each add to my understanding and ability to forecast/explain what actually happens.

ReplyDeletenanute - You make some good points on IOR and MTM that I certainly agree with. As it relates to MTM, my view remains that the TBTF banks are still holding hundreds of billions (maybe trillions?) in market losses on mortgages and mortgage related securities. These losses, if recognized, would cause rating downgrades, followed by calls for capital and could quickly put several of the banks in liquidity/solvency troubles.

As you mention, IOR's are a means of repairing bank balance sheets, albeit very slowly. One stark advantage occurs if deflation occurs or short-term rates go negative (e.g. Germany). In that case, US banks would still be able to earn a positive nominal return and even greater real returns from IOR. European banks no longer hold this option, although I imagine excess reserves are still more valuable than short-term sovereign debt paying negative rates.

As for the decision to lend, I don't believe the 25 basis points is a significant factor for banks. My view continues to be that private demand for credit is weak because households still hold too much debt relative to income. Banks may be cautious because of their weak balance sheets, but with bonuses and jobs tied to profits, there remains a huge incentive to lend if demand is there.

Lastly, I completely agree that if Republicans win the policies will likely still favor the financial sector. Where I take a lightly different view is that I'm not convinced it will be any different with the Democrats. Both parties have shown commitment to the view that health of the large banks come first. I remain hopeful that eventually some party will begin to accept the theories/policy approach linked to aspects of heterodox economics (that we're discussing here).