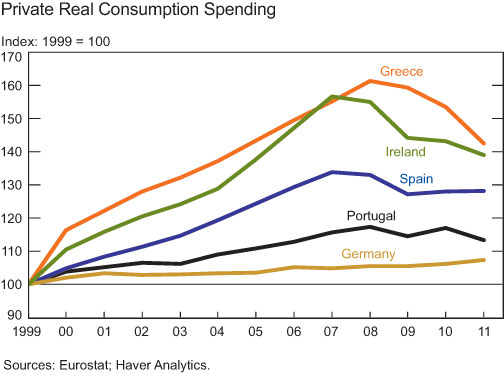

Real consumption spending in Ireland and Greece increased roughly 55 percent from 1999 to 2007 (chart below). In Spain, the corresponding figure was around 35 percent. Again, Germany stands at the other extreme. Consumption remained essentially flat after 2001, leaving the country with ample funds to lend abroad. Similarly, household liabilities ballooned in the periphery countries, far outpacing growth in disposable income, while liabilities declined relative to disposable income in Germany. These divergent consumer spending trends were a key driver of euro area imbalances.

Read it at Liberty Street Economics

Euro Area Spending Imbalances and the Sovereign Debt Crisis

By Matthew Higgins and Thomas Klitgaard

The New York Fed’s research arm has been producing a number of good articles recently, occasionally even straying from mainstream economic thinking. While most discussion of Europe has focused on sovereign debt and the financial sector, private sector debt imbalances remain critical to understanding both the causes of the crisis and potential policy solutions.

The authors note that

Foreign borrowing to finance productive investment projects raises national income and should result in a surplus over debt service costs. Foreign borrowing undertaken because of lower levels of saving, in contrast, supports current consumption while building up a debt burden on future income. The composition of investment can also matter. For example, foreign borrowing to support investment in nontradable sectors such as housing generates no foreign income stream to support repayment.Acting in a similar manner as the US private sector during the previous decade, the private sector in peripheral Europe largely borrowed from abroad to support current consumption and investment in housing. Rising debt levels were manageable, for a time, without an increase in incomes as long as asset prices were rising and new credit was available to service current debts (Minsky considered this stage “ponzi” finance). When asset prices stopped rising and credit became more restricted (which must always happen), the private sector was forced to reduce consumption and investment to pay debt servicing fees and attempt to deleverage.

This above dynamic is especially important for understanding Spain, where sovereign debt levels (at least those officially reported) are not particularly high. Spain’s housing bubble, however, continues to decline putting further pressure on private sector balance sheets. The public and private sectors cannot both successfully deleverage, in tandem, without destroying incomes and growth. Debts that cannot be repaid, will not be repaid.

Private sector debts in periphery Europe, as well as the US and UK, must be brought back in line with incomes to support any sustainable future growth. The options for achieving this are either nominal income growth above debt servicing costs, debt write-downs, or a combination of the two. So far, policy in Europe seems to be attempting neither and the situation continues to worsen (unemployment is currently at a 15-year high). If there is any hope for a peaceful resolution of the Eurozone crisis, policy makers must begin to focus on correcting private sector debt imbalances.

Good point!

ReplyDeleteHowever, why private debt expansion in Europe, that has increased the total money ciculating in the economy, has not caused inflation in Spain, Greece, Ireland?

Inflation for those countries from 200-2008 was averaging close to 4%/year. This data also obscures the asset price inflation most notable in housing during that period.

Delete