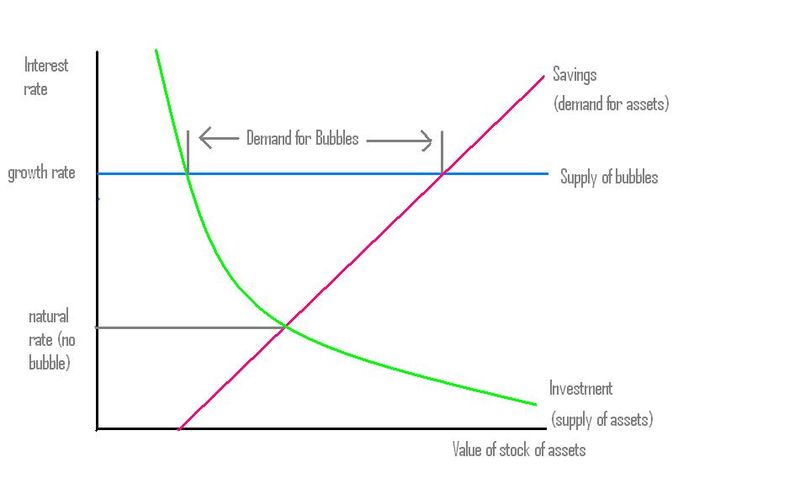

During these supposedly abnormal periods the demand for money is high. If this demand is not met with supply(e.g. through government deficits) or reduced (e.g. increased taxes), than people will seek out money-like instruments. Michael Sankowski notes that money-like instruments can be as simple as “stocks being used to purchase real world goods, or using the paper value of real estate as collateral to purchase real world goods.” Increasing demand for these instruments drives prices higher, which in turn, boosts their value as money-like instruments. This creates a self-fulfilling upward cycle in both demand and price. Therefore, “as long as the real growth rate is higher than the real interest rate, the economy will demand bubbles.” (Graph below from The supply and demand for bubbles (in pictures))

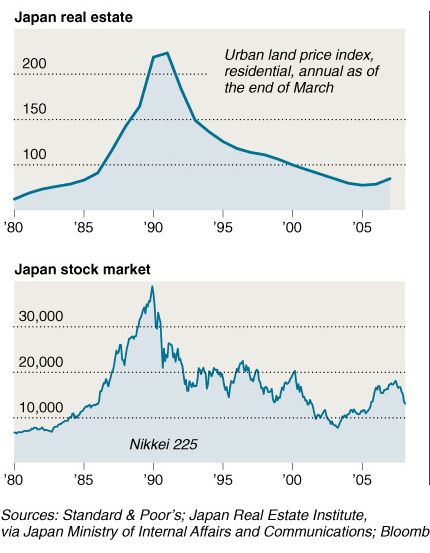

Americans experience during the past 20 years should bear out this fact since the economy has seemingly moved from one bubble to the next (e.g. dot-com, real estate, commodities). As we speak, stocks and commodities may once again be providing the bubble our economy desires. In contrast to the US experience, Japan’s economy has resembled a ‘normal’ world for much of the past 20 years. Deflation has largely kept the real interest rate (using 10-year JGB yields) in the 1-2% range, while real growth rates were frequently between 0-1%. This environment encourages reduced borrowing and, by extension, less desire for money-like instruments. The result has been real estate and equity markets that dropped over the entire period. (Graph from Dr. Housing Bubble)

While the economy may frequently desire bubbles, these are a sign of private sector waste (inefficiency) that always results in wealth destroying busts. Within Post-Keynesian schools of economic thought, both the interest rate and inflation can be controlled, to a degree, by the combination of fiscal and monetary policy. Accepting that our economy is often in an abnormal state is the first step to alleviating the economy’s need for a bubble.

Interesting post. Something I never thought of before.

ReplyDeleteDunno about the Nick Rowe post, however. I always went with what Keynes said, that low interest rates are good for growth. Because, as you say, "When growth outpaces interest rates, the environment is ripe for borrowing money to invest and consume."

As far as "needing a bubble" ...

We've been getting those unsustainable financial bubbles since the 1980s, because finance is more profitable than the productive sector. There was lots of borrowing in the 1950s and '60s, but we didn't get bubbles then, because the productive sector was more profitable than finance. We got output.

Something like that.

That's a fair point. Borrowed money need not go to financial asset investments or consumption. As you've pointed out, it seems that many public policies over the past few decades have attempted to push individuals towards using credit for consumption or financial assets. In my view, these policy decisions almost certainly played a role in the appearance that finance is more profitable than the productive sector (I'm not convinced it actually has been in the aggregate).

DeleteIf this is correct, the goal of policy going forward should be to reduce the reliance on credit versus money while realigning incentives toward the productive sector and away from finance. Reducing corporate tax loop hopes/expenditures and lowering the marginal rate may be one way to promote firms to re-invest rather than pay out higher salaries or bonuses.