From the perspective of improving sentiment, the stress tests are clearly a roaring success. However, investors should remember that the purpose of the stress tests was to inspire confidence and NOT to test the liquidity or solvency of banks in a crisis. As Bloomberg’s Jonathan Weil highlights in Class Dunce Passes Fed’s Stress Test Without a Sweat:

“Citigroup Inc. (C) was deemed well capitalized under the government’s methodology when it got bailed out in 2008. So was CIT Group Inc. when it filed for bankruptcy in 2009.”The stress tests then and now continue to use Tier 1 Capital ratios, which is simply the amount of Tier 1 capital divided by a firm’s risk-weighted assets. Risk-weightings are often decided by the regulator based on credit ratings. Many AAA-rated securities are assigned 0% risk and removed from the calculation. As various assets are downgraded during a crisis, total risk-weighted assets rise and the Tier 1 Capital ratio declines. Rating changes, which played a major role in both the financial and European debt crisis, depict one of many flaws in using Tier 1 Capital Ratios to assess a bank’s health.

Although the Fed continues to use this poor indicator, Weil notes that:

“Tangible common equity became the capital benchmark of choice for many investors during the last U.S. banking crisis, because the government’s main capital measures lost credibility.”Expanding his investigation into the current realistic health of banks, Weil found that:

“if it weren’t for the inflated loan values, [Regions Financial’s] tangible common equity would have been less than zero, with liabilities exceeding hard assets.”Despite still not having paid back TARP funds and potentially being insolvent, Regions passed the stress tests.

Apart from testing somewhat irrelevant capital measures, the stress tests also provided an estimate of bank losses during the projection period (Q3 2011-Q4 2013). During that year and a half the Fed projects these 19 banks will, on net, lose nearly $250 billion. These estimates are almost surely optimistic and don’t account for future losses on these assets, among other things. Daniel Alpert of Westwood Capital, LLC has great, detailed report on the expected losses over time, Deconstructing the Federal Reserve’s 2012 Comprehensive Capital Analysis and Review: What Does the CCAR Really Tell Us About the Big 4 Commercial Banks? As the title suggests, the Big 4 banks may be significantly more vulnerable than many expect.

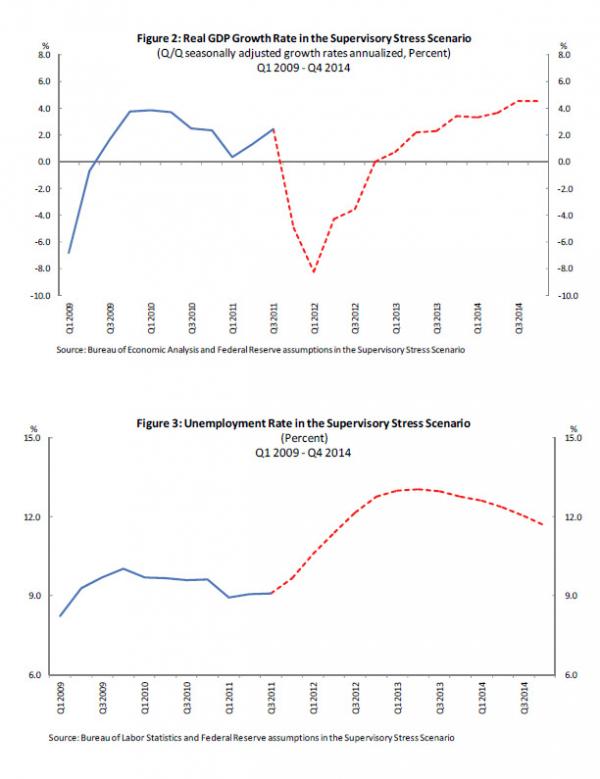

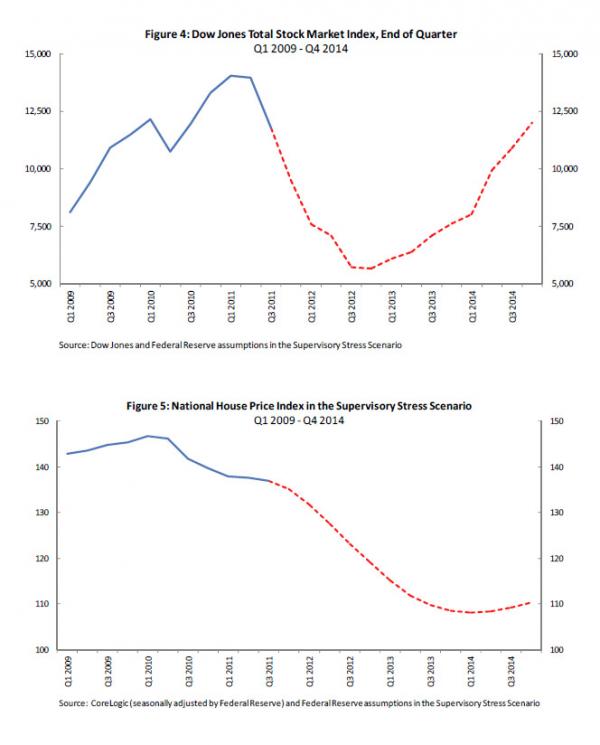

One final point of interest regarding the stress tests relates to the underlying assumptions made by the Fed. The following graphs outline the assumptions made (courtesy of Zero Hedge):

Reflecting similarities to the most recent crisis, GDP and the stock market move sharply upward after the initial decline, while unemployment and housing prices languish. The aspect I’ve yet to see mentioned with these assumptions is that the bailouts (Fed and TARP) along with stimulus measures are supposedly the reason behind the rebound. One might then infer that the Fed’s stress tests assume future bailouts and stimulus measures, of similar proportions, to achieve comparable results.

Overall the Fed’s stress tests have been wildly successful as a promotional tool for the largest banks. Many of these banks are now increasing the return of capital to shareholders that will prove critical in the next crisis. Maybe after the next round of bailouts regulators will be forced to change their approach.

No comments:

Post a Comment