As an avid follower of new economic work being done in Post-Keynesianism, Modern Monetary Theory (MMT) and Modern Monetary Realism (MMR), I’ve often been perplexed by apparent inconsistencies in discussions regarding saving and leverage. My confusion stemmed, in part, from the notion that households are capable of saving and increasing leverage (debt as a share of GDP) at the same time. If you’re a bit confused at this point, don’t worry, I’ll explain the situation more simply in a moment.

Before moving on, it’s important to recognize that economic terminology often does not fit with typical usage of every day words. Here are some important economic terms to understand going forward:

Saving - The difference between disposable income and consumption.

Disposable Income - Income minus taxes.

Consumption - The amount spent on non-durable goods (e.g. food, clothing) plus the amount spent on durable goods (e.g. autos) spread over the item’s life span. (Note: Purchasing a home is an investment, for which an imputed rent is counted as consumption.)

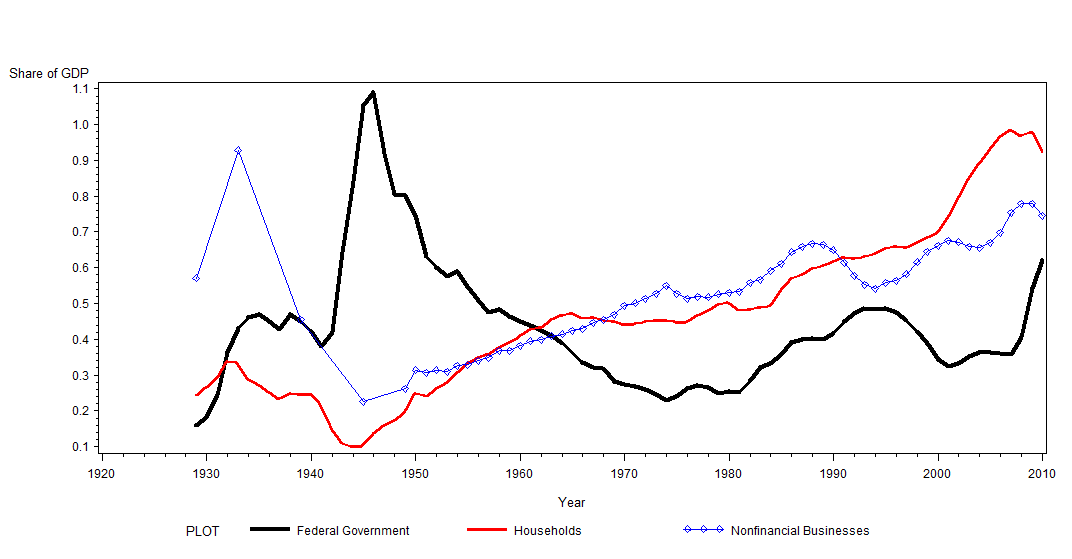

Using this definition of saving, it becomes clear that households can maintain a positive savings rate yet still be net borrowers, as long as that borrowing goes towards investments. Ramanan, a horizontalist, recently explained this concept in a wonderful post on Saving Net Of Investment [Updated]. From this perspective, the frequent comment that households must increase saving to reduce leverage is clearly false. The rise in household debt during the post-WWII period is apparently based on net borrowings, not the private savings rate.

This new found understanding has proved short-lived after reading the following Guest Post by JW Mason: The Dynamics of Household Debt over at Rortybomb. A new working paper finds

“that changes in borrowing behavior has played a smaller role in the growth of household leverage than is widely believed. Rather, most of the increase can be explained in terms of “Fisher dynamics” — the mechanical result of higher interest rates and lower inflation after 1980.”Put in simpler terms, interest rates on household debt since 1980 have been consistently higher than income growth. Under these conditions, even without increasing borrowing, household leverage will increase.

Over the past few years, household leverage has been decreasing largely due to debt write-downs. With this process slowing, the scenario mentioned above is likely to return. Even though interest rates remain at or near historical lows, income growth has been practically stagnant. Without a drastic change in these variables, the large burden of household debt is likely to continue suppressing consumer demand well in to the future. Attempts by households to increase saving may inadvertently decrease income, exaggerating the problem. Simply put, significant debt write-downs (a modern day debt-jubilee) may be necessary to restore the household sector to a stronger, more stable, financial position.

You wrote

ReplyDelete"Put in simpler terms, interest rates on household debt since 1980 have been consistently higher than income growth. Under these conditions, even without increasing borrowing, household leverage will increase."

Why speculate? Private sector borrowing increased at an average of 10%/year for the entire period of 1950-2008. While income grew at around 3%. Interest rates had very little effect on the rate of borrowing.

The comment/post was not meant to suggest that interest rates had altered the rate of private borrowing. The point is that, even without new borrowing (which is unlikely to occur), household debt as a percentage of GDP would continue to increase. The burden of this debt therefore continues to grow, which likely puts pressure on households to continue borrowing in spite of changes to interest rates.

ReplyDeleteNice & Informative Blog !

ReplyDeleteIn case you are searching for the best technical services for QuickBooks, call us at QuickBooks Error 2107 1-855-977-7463 and get impeccable technical services for QuickBooks. We make use of the best knowledge for solving your QuickBooks issues.