A steady state is characterized by the economy having a constant rate of growth. I here select a number of expositions of analyses of steady state I have made on this blog:

- The Harrod-Domar model of warranted and natural rates of growth.

- Karl Marx's volume 2 model of simple and expanded reproduction.

- Explanations of aspects of the non-substitution theorem.

- Neoclassical Overlapping Generations (OLG) models with intertemporal utility maximization.

2) The “Liquidity Trap” Theory Was Never Right…. by Cullen Roche @ Pragmatic Capitalism

Anyhow, most of the mainstream has been working under some form of the “liquidity preference” theory or “liquidity trap” theory to explain why rates have remained low in the USA. This was the thinking that economic agents were choosing to just sit on the excess liquidity provided via the government and the Fed. It sounds right in theory, but it’s wrong in reality.

First, the government doesn’t increase the money supply through government spending (already confused? See here). It redistributes inside money (bank money) and adds a net financial asset in the form of a government bond. This improves private balance sheets and is particularly useful during a balance sheet recession, but it’s not the equivalent of firing dollar bills out into the economy (though it does increase the velocity of spending as the government becomes the “spender of last resort” when an economy is stagnant for whatever reason). Second, when the Fed implements QE they swap reserves for bonds. No change in net financial assets. And since banks don’t lend reserves there is no firm transmission mechanism through which this policy can impact the money supply. In short, fiscal policy hasn’t been the equivalent of increasing the money supply in the traditional “money printing” sense that most believe and QE has most certainly not resulted in an increase in the money supply because the primary transmission mechanism is busted (the lending channel).Woj’s Thoughts - Paul Krugman has recently changed his views to acknowledge that bond vigilantes are not an issue for the US. While he should be commended for taking this step away from the typical mainstream position (which he held prior to the crisis), his views remain tied to “liquidity trap” models. Although these models will, in some instances, come to correct conclusions, that may be due to chance rather than logic.

3) Macroeconomics and the financial cycle by Matias Vernengo @ Naked Keynesianism

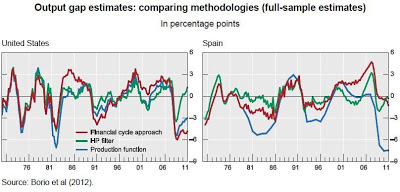

Claudio Borio from the BIS has written a widely cited paper.

…

The new output gap measure would include financial variables. He correctly notes that output gap measures take into consideration only inflation, when ascertaining whether the economy is above the potential or not, and that "it is quite possible for inflation to remain stable while output is on an unsustainable path" [and you can have inflation without being at full employment too, I would add]. His measure of the output gap would include information about asset price inflation too (property prices and measures of credit booms) and is shown for the US and Spain as the red line below.

…

I have several problems with these views, even if there are some good things, beyond good intentions, in Borio's paper. In fact, I think that there is significant evidence for the notion that potential output varies with demand expansion (Kaldor-Verdoorn Law), so that if a revision of the way potential output is measured it would be in the opposite direction.Woj’s Thoughts - An accurate measure of the output gap would be very beneficial in demonstrating the periods when macroeconomic smoothing is necessary. Unfortunately trying to create that measure is no easy task and previous efforts have likely led to false policy prescriptions. Given the substantial variation based on methodology, as shown above, the current benefit of such measures to policy making seems limited.

No comments:

Post a Comment