Here’s David [Schawel]’s comment:

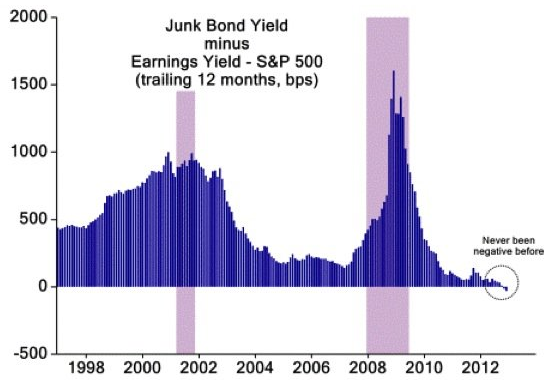

“The chart below shows the spread between the yield on junk bonds and the yield received from holding stocks. The spread recently turned negative for the first time ever, showing just how much the yields on high-risk bonds have come down as central banks keep benchmark borrowing rates depressed and investors search further out on the risk spectrum for yield.”

Woj’s Thoughts - This chart, more than almost any other, may highlight the potential harm induced by the Federal Reserve’s attempts to push private investors further out on the risk spectrum. Unless junk bond companies have truly become significantly less risky, when the next round of increasing defaults begins, investors will find that current yields fail to even remotely compensate for future losses. Stocks may currently be slightly overvalued from a historical perspective, but certainly not compared with junk bonds.

2) Too Much Faith, Not Too Little by Mungowitz @ Kids Prefer Cheese

I have long believed that the problem market economies have with statists is misunderstood.

Pro-market folks tend to think that statists just don't understand markets. And to some extent that's true. But the real problem is that statists have too much faith in markets.

Wait...too MUCH? How can that be? (More after the jump...)

3) Trickle-Down Monetary Policy by The Arthurian @ The New Arthurian Economics

The Fed buys the IOU from my lender. The lender gets cash. And I get to make the same payments I made before, except now I pay somebody else. That really doesn't do much for me. It doesn't do much for the economy, either.

Purchasing assets removes those assets from the economy, replacing them with money. But the liabilities remain as they were: draining income, depressing demand, hindering economic growth.Woj’s Thoughts - Art explains in a very straightforward manner the basic problems with QE. If the heart of the issue is excessive debt, asset swaps do basically nothing to reduce household liabilities while removing interest income from the private sector. I think Art goes a bit too far in suggesting the Fed cancel private liabilities outright since explicit fiscal policy should be left to elected officials.

No comments:

Post a Comment