Case in point, the $80 bln in profits that the Fed earned and turned over to the Treasury last year, was from income earned on the assets it bought. That was income that would have been earned by the private sector if it still had those bonds and securities.

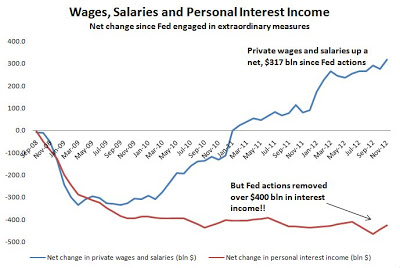

So while the net change in wages and salaries since 2008 has been an increase of $317 bln, personal interest income dropped by $425 bln. That's not a stimulus by any means. It's mind boggling that the mainstream economics community and the Fed itself, doesn't understand this when they incessantly call for more "stimulus."

Unlike the Market Monetarists and New Keynesians, who have been constantly begging for the Fed to “do more”, this is why myself and many others have been wishing the Fed would do far less. While stimulating present paper profits in the stock market through negative real yields, the Fed’s actions are actually removing income from the private sector. Instead of stimulating the economy, ZIRP and QE help ensure the economic recovery remains weak. These actions will only further the reliance on credit and exacerbate downturns going forward.

I agree with your perspective on MM but if interest rates were allowed to rise would the increase in personal interest income offset the increased cost of debt servicing. Seems to me that QE slows down the deflation of a distorted debt structure at the expense of savers and those on low incomes, at some point the hope being that releveraging can restart, i.e., it's all about preserving the broken world view that got us here.

ReplyDeleteIf interest rates were allowed to rise, it's hard to say whether the cost of debt servicing or interest income would be larger. QE, however, reduces interest income without any offsetting reduction in debt service costs. So I'm less convinced that raising interest rates is beneficial, which some MMTers suggest, but do think QE is a generally poor policy.

DeleteA side note, I've been wondering how much of the recent reduction in debt servicing costs stems from low rates and re-financing versus new auto and student loans that have no or low payments for the first few years.

OK, so my question was based on the view that current low interest rates were at least in some part due to QE but you think this isn't the case?

DeleteAh. Well I would agree that QE played some role in lowering interest rates, but the question is by what channel and how much? The reduction in interest income from removing higher yielding securities is certainly deflationary. Given the perception of QE, it is equally likely that it raises inflation expectations temporarily putting upward pressure on interest rates. I'm inclined to think the first effect has a longer-term effect.

DeleteIs your question also related to the idea that low interest rates are good for the economy? If so, I think that entails a different discussion of why rates are so low. Market monetarists often discuss how Bernanke and the FOMC are lying when saying they want lower rates because they actually want higher rates from increased inflation expectations.

I still don't have a full understanding of this at present, to me QE is a continuation of a theme, that of a one way monetary intervention against a badly measured benchmark - that being "inflation". One way, because in the interest of always preventing a "recession" that intervention conveniently ignored massive inflation in assets which eventually became a Ponzi leading to unsustainable private sector debt levels. Main stream economists flawed thinking about private sector debt levels apparently leading them to think the size of private sector debt was irrelevant.

DeleteOnce it because apparent these debt levels weren't sustainable policy makers response - as always - was to reduce interest rates and manipulate the yield curve with a view to the knock on effect on the sustainability of that private sector debt level. My understanding was that QE was a crucial part of this, without which peoples mortgage rates would be heading up. So while QE reduces interest income the narrative was that this was just the cost savers have to pay to prevent a large increase in mortgage costs.

"Ah. Well I would agree that QE played some role in lowering interest rates, but the question is by what channel and how much?"

Yes, I guess this is the key, what role does QE play in reducing private sector debt servicing costs, if any, and is this offset by how much it hits savers.

Every time I get into a discussion of this stuff I realise how much I don't know!

Just to add to my comment Scott Fullwiler has written a series of posts which will probably fill some of the gaps in my knowledge here http://neweconomicperspectives.org/2012/12/functional-finance-and-the-debt-ratio-part-i.html

DeleteApologies for the delayed response but I was on vacation the past several days.

DeleteYou are certainly not alone in recognizing how nuanced monetary policy actually is and how many competing views there are of the same action. I haven't had the chance to read through Fullwiller's full series yet, but his papers and other work have had a significant influence on my current thinking.

Getting back to your previous comment, there are seemingly three basic views of QE. Bernanke will likely argue that QE helps maintain low interest rates by reducing supply and thereby increases demand for housing and other financial assets, keeping prices higher than they otherwise would be. Sumner argues QE should influence inflation expectations and therefore, to the degree it is successful, actually raise mid-to-long term interest rates. Modern money proponents argue that QE keeps interest rates low by promoting a deflationary outcome (closer to Bernanke's views).

Those are my best interpretations of the different camps. My view is that in the short-term, QE does raise people's expectations of inflation (including asset prices), which leads to higher interest rates and asset prices. After the initial effect, investors realize actual inflation and GDP growth and not picking up, which leads to declines in interest rates. These declines still spur asset prices since low interest rates should increase the PV of future cash flow (I'd argue the future cash flow is declining, but that aspect has gone unrecognized so far).

To try and sum up this part...my view is that QE helps reduce debt servicing by creating a more deflationary (disinflationary) environment beyond the short-run. I'd argue that the US could reduce those costs further by lowering the upper-end of the inflation target to 1%. I doubt that would actually create a positive boost to the economy.

No problem, thanks for the perspective.

DeleteAs an aside "The case for concerted action" chimed in on the Fullwiler piece here http://www.concertedaction.com/2013/01/05/wynne-godley-and-the-dynamics-of-deficits-and-debts/