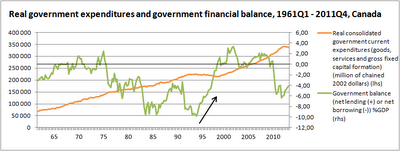

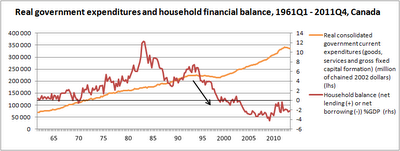

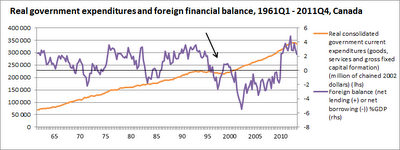

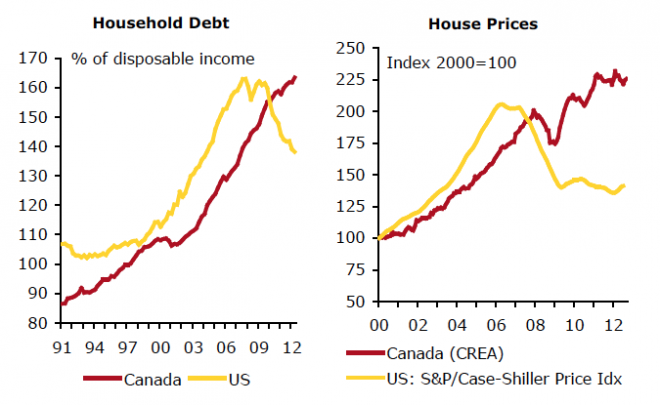

During the 1990’s, Canada witnessed a dramatic rise from a ten percent budget deficit to a fiscal surplus. That reduction in aggregate demand was countered by a significant decline in the household financial balance to a net borrowing position and a substantial trade surplus (foreign net borrowing). Keeping with global trends, the massive rise in Canadian household debt was primarily funneled into the domestic housing sector, pushing prices into bubble territory:

Source: Macleans.ca

The Canadian government’s hopes of repeating its “success” from over a decade ago will require a renewed surge in demand from one of the other sectors. Weak global growth, especially in China, suggests that commodity-rich Canada will not witness a dramatic reversal in their trade balance anytime soon. That leaves the household (or business) sector to pick up the slack.

As witnessed recently in the US and throughout Europe, there comes a point at which households can no longer credibly be expected to repay outstanding debts. Regardless of what event brings about this realization (possibly declining house prices), the ensuing household deleveraging will be a major headwind to growth.

A global commodity boom and domestic housing bubble bailed out the Canadian government last time it attempted to drastically reduce the budget deficit. This time around, the government’s actions may be enough to bust the housing bubble and push Canada into a recession.

No comments:

Post a Comment