In the wake of the crisis the Too Big To Fail problem has grown across the rich countries. When something happens always and everywhere we should start looking for underlying laws. We're not at "always and everywhere" here but it's getting close: Time to theorize.

I don't think political influence from big banks is a major reason for the recent rise in bank size. Political influence is a constant, like gravity, so the question is what changed after 2008. Why the rise in bank concentration just as economists, policymakers, and politicians became more worried about bank concentration?

It sounds to me like an interaction between hyperbolic discounting (impulsivity, short term impatience in the government sector) and time inconsistency (depositors know the regulator will cave later so depositors put more money in TBTF banks today, making it even more tempting for the regulator to cave).Woj’s Thoughts - Jones goes on to make the case for banning acquisitions by the biggest banks. I left the following comment on his blog:

While I agree that "hyperbolic discounting by bank regulators is a big problem", I wonder whether banning acquisitions would solve the problem. Looking at the most recent crisis, Bank of America, Wells Fargo and JP Morgan were practically begged by regulators to acquire other large banks presumably because no better alternative existed. Had those mergers been prevented, what actions would have been taken? Speed bankruptcy is an option, but likely wasn't on the table. It seems plausible that the government and Fed would have bailed out those failed banks more explicitly.

One of the other channels, that I think may be a greater issue, is the subsidies inherent in an implicit government backing for SIFIs. My reading suggests these institutions are able to finance their operations at rates 50-100 bps below other financial institutions. This cost advantage could eliminate smaller institutions regardless of banning acquisitions.

2) quick look ahead for the euro zone by Warren Mosler @ The Center of the Universe

All this gets me back to the idea that the path towards deficit reduction in this hopelessly out of paradigm region keep coming back to the unmentionable PSI/bond tax. Seems to me we are relentlessly approaching the point where further taxing a decimated population or cutting what remains of public services becomes a whole lot less attractive than taxing the bond holders. And the process of getting to that point, as in the case of Greece, works to cause all to agree there’s no alternative. With the far more attractive alternative of proactive increases in deficits that would restore output and employment not even making it into polite discussion, I see the walls closing in around the bond holders, along with the argument over whether the ECB writes down it’s positions back on page 1. And just the mention of PSI in polite company throws a massive wrench (spanner) into the gears. For example, if bonds go to a discount, they’ll look towards ECB supported buy backs to reduce debt, again, Greek like. And if prices don’t fall sufficiently, they’ll talk about a forced restructure of one kind or another, all the while arguing about what constitutes default, etc.

The caveats can change the numbers, but seems will just make matters worse.Woj’s Thoughts - Mosler has been one of the few voices that predicted this outcome for the Euro zone from the beginning. His thoughts on the forthcoming strength of the euro have certainly made me reconsider my views. I continue to worry about the political aspect within Europe and whether the people will continue to accept depression dynamics to remain in the Euro zone.

3) Wealth and Redistribution Revisited: Does Enriching the Rich Actually Make Us All Richer? by Steve Roth @ Angry Bear

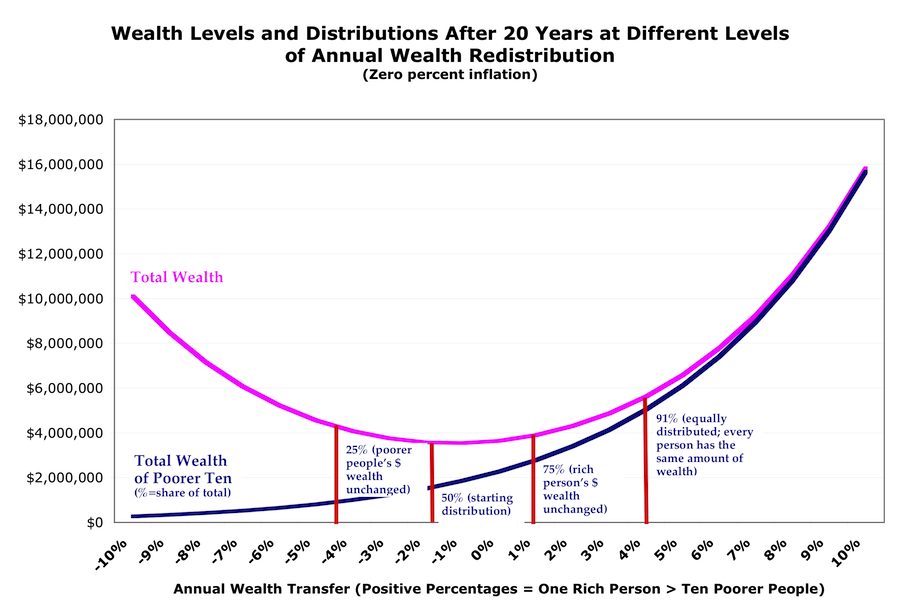

Here’s what that looks like, with starting wealth of $2 million, divided 50/50 between the rich person and the ten poorer people. (click for larger):

Woj’s Thoughts - Click through for surprising lessons about redistribution from this very basic model.

No comments:

Post a Comment