1) Hit the “Defer” Button, Thanks… by David Merkel @ The Aleph Blog

This is why I believe that the biggest issue in restoring prosperity globally, is finding ways to have creditors and stressed debtors settle for less than par on debts owed. Move back to more of an equity culture from what has become a debt culture. A key aspect of that would be making interest paid non-tax-deductible for corporations, housing, etc., while making dividend payments similar to REITs, while not requiring payouts equal to 90% of taxable income. Maybe a floor of 50% would work, with the simplifying idea that companies get taxed on their GAAP income — no separate tax income base. Would certainly reduce the games that get played.

Anyway, those are my opinions. The world yearns for debt relief, but governments and central banks argue with that, and in the short-run try to paper over gaps with additional short-term debt that they think they can roll over forever. They just keep trying to hit the “defer” button, avoiding any significant reforms, in an effort to preserve the “status quo.”Woj’s Thoughts - After reviewing the results of my 2012 predictions, I mentioned:

My main takeaway is that politicians are far more determined to maintain the status quo than I had expected. The underlying economic (and social) problems have once again been kicked down the road for future governments to handle.Although David’s policy recommendations are becoming increasingly pervasive, they unfortunately remain nowhere near the level necessary for governments to test uncharted waters.

2) Can Germans become Greeks? by Dirk @ econoblog101

The ECB as well as other policy makers and politicians do not understand economics. They think that a simple recipe like “decrease government spending, export more” is enough to solve the euro zone crisis. The increase in government debt is a symptom of the crisis, not a cause. The cause of rising government debt was negative economic growth and bank bail-outs. These are the two problems which must be tackled. They are intertwined, so solutions should address both. Households cannot pay their mortgages in Spain and Ireland at the existing unemployment levels, and that is due to a lack of demand as households consume less and save more. This downward spiral must be stopped and turned around, since at negative growth rates even a government debt of €1 is too high.

It seems that instead of Greeks becoming Germans now the German are becoming Greeks. That means that without government spending Germany will not have positive growth rates. While this will come as a surprise to many, it shouldn’t be.Woj’s Thoughts - Germany managed to run a slight fiscal surplus during 2012 that ultimately came at the expense of growth. In the fourth quarter, German GDP shrank by 0.5 percent. Meanwhile, attempts at structural reform (i.e. fiscal consolidation) in the European periphery appear to be speeding up the rise in unemployment and decline in growth. This dynamic is neither economically or socially sustainable, therefore the governments and ECB must either substantially change the current course or wait for countries to eventually exit the Eurozone.

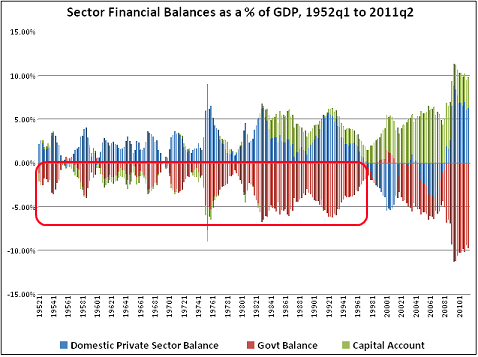

3) Did We Have a Crisis Because Deficits Were Too Small? by JW Mason @ The Slack Wire

The logic is very clear and, to me at least, compelling: For a variety of reasons (including but not limited to reserve accumulation by developing-country central banks) there was an increase in demand for safe, liquid assets, the private supply of which is generally inelastic. The excess demand pushed up the price of the existing stock of safe assets (especially Treasuries), and increased pressure to develop substitutes. (This went beyond the usual pressure to develop new methods of producing any good with a rising price, since a number of financial actors have some minimum yield -- i.e. maximum price -- of safe assets as a condition of their continued existence.) Mortgage-backed securities were thought to be such substitutes. Once the technology of securitization was developed, you also had a rise in mortgage lending and the supply of MBSs continued growing under its own momentum; but in this story, the original impetus came unequivocally from the demand for substitutes for scarce government debt. It's very hard to avoid the conclusion that if the US government had only issued more debt in the decade before the crisis, the housing bubble and subsequent crash would have been much milder.Woj’s Thoughts - The scenario laid out by JW sounds equally plausible and compelling to me. Changes in tax policies during the 1980’s and 1990’s set the stage for massive increases in real estate loans and the corresponding housing price boom. Then the unmet demand for safe-liquid assets prompted both the rise of shadow banking and the dispersion of U.S. housing assets to the rest of the world. So as the last sentence attempts to make clear, the “crash would have been much milder” but a similar crisis would likely have occurred.

Woj, when Merkel says making interest paid non-tax deductible on housing, does he mean ending the mortgage interest deduction?

ReplyDeleteIf he does that would mean a significant tax hike for middle class families.

I actually think one of the worst parts of the Reagan "tax reform" of 1986 ended the deduction for normal interest tha individuals can take.

I

In reference to housing, I presume Merkel is discussing the mortgage interest deduction. This would be a significant tax hike for the middle class and a much larger one for the upper class. It's odd that you should point out the regressive nature of the 1986 tax reform considering that the mortgage interest deduction is potentially the most regressive, current tax expenditure.

DeleteI recognize there are decent arguments for not raising the cost of housing while so many remain underwater, but if not now, when? As I see it, there is a very big difference between being in favor of home ownership and encouraging the accumulation of debt while simultaneously raising the cost of ownership.

Fiscal and monetary policy is currently doubling down on a housing boom driving sustainable economic growth and employment for the foreseeable future. I fail to see how the outcome will be any different than the numerous housing busts and recessions that continue to unfold around the globe (e.g. Spain, Netherlands, Australia, Canada, China). So while I'm actually not in favor of reducing the deficit currently, I think there are few better ways to promote long-term growth than the elimination of tax-deductible interest for all sectors.

While many when they talk about tax reform look back on the 1986 deal as a kind of model for what we should want I see that a one of the worse deals ever that was very regressive.

ReplyDeleteI'm all for the objective of bringing down debt but surely there are better ways? One way is to give people other ways to get needed cash.

You say it's the most regressive expenditure because it benefits the rich? It also benefits the middle class. I would agree with phasing it out or limiting it for the rich, however,

ReplyDeleteAs far as the future, do we really have the luxury of deciding what kind of prosperity we have? You seem to be saying we shouldn't try to stimulate a recovery, and that in the long run this restraint will lead to healthy more sustainable growth.

Is it possible though that part of a capitalist economy is boom and bust-the business cycle?

I don't know that a more sustainable kind of growth is really possible-there isn't much historical precedent for it that I'm aware of.

I'm suggesting it's the most regressive because of its magnitude and heavy skew towards wealthy households. Here is a chart showing the average value per income group from 2009 (https://prospect.org/sites/default/files/mortgage_interest_deduction.jpg). The average benefit at the top is equivalent to the total average benefit of all other groups. If we consider all households making over $100k, the average benefit is nearly double the other groups.

DeleteAs for the future (maybe ~20-30 years), I do believe that we have some degree of control over the type of prosperity. My suggestion would actually be TO stimulate the economy by writing down debt primarily for the lower four income quintiles. What I don't recommend is stimulating the economy by diverting income towards the top quintile, which has largely been the case.

I completely agree with you that the boom-bust cycle is an inherent aspect of capitalism and probably any economic system for that matter. My claim, however, is that stimulating the economy by increasing income/wealth inequality will create more frequent and volatile cycles. As the most recent crisis shows, the result tends to favor creditors (wealthy). So when I say sustainable, I simply mean average real GDP will be higher and with less variation over a given period of time.