In the 1980s, Japan engaged in ill-conceived financial deregulation (Fukao 2003: 134–135), which was one major cause of the asset bubble in these years (although poorly designed tax policies and monetary policy were clearly involved too). The collapse of the asset bubble and the balance sheet recession (a form of debt deflationary crisis) caused the “lost decade.”

From the data above, we can see that the “lost decade” was really an era of low growth, not continuous negative growth. Japan was not in recession from 1993–1997, but had serious deleveraging problems, a banking crisis, and debt deflation.

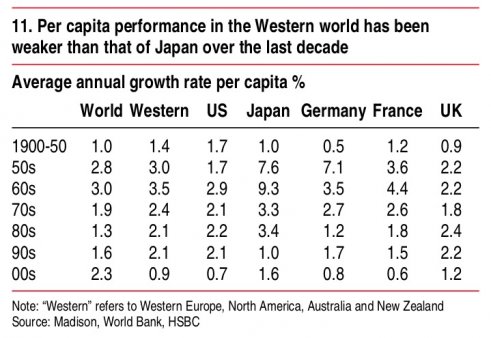

Many myths have arisen about the lost decade, and one of them is that Keynesianism somehow “failed” to work in this era. That is nonsense. If anything, Keynesianism saved Japan from a terrible depression. In fact, when fiscal stimulus was abandoned for austerity in 1997, the economy plunged into a recession in 1998.Of the myths regarding Japan’s lost decade (now decades), I’ll admit to having been unaware that 1998 marked the first year of negative real GDP growth since 1974 (and only second since 1945!). Since then, Japan has unsuccessfully tried to get on a fiscally sustainable path (whatever that means) as more frequent recessions have led to larger budget deficits (and growing debt/GDP) that merely prevent larger economic declines. Despite the persistence of misguided fiscal (and monetary) policy, Japan’s per capita economic growth has remained on par with the Western world.

With nonfinancial private sector balance sheets largely repaired, Japan appears poised to continue leading the Western world if government policies improve. Unfortunately last night’s Joint Statement of the Government and the Bank of Japan on Overcoming Deflation and Achieving Sustainable Economic Growth shows the lessons of a previous age remain forgotten.

No comments:

Post a Comment