producer prices (roughly approximated by the GDP deflator) grew much more quickly than consumer prices (roughly approximated by the CPI).If the Bank of Canada were to begin targeting NGDP in the future, it would effectively be altering the primary measure of inflation in its goal. This leads Gordon to beg the question, What should a central bank do when producer and consumer prices diverge?

My (possibly incomplete) understanding is about how inflation affects welfare is on its effect on the price of consumption goods, especially in a world where nominal wages are slow to adjust. So it makes sense to me to make consumer prices the focus of attention and let producer prices go.

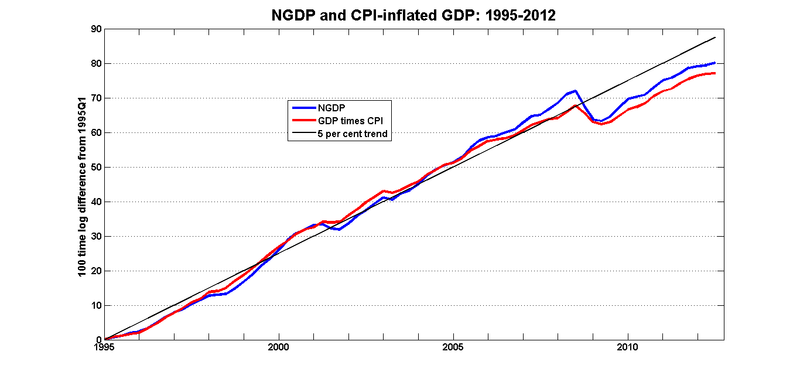

I'm not sure how to interpret this next graph, but I made it and I may as well post it. It compares NGDP with the series you get when you multiply real GDP by the CPI. I guess it's the counterfactual NGDP series for the scenario where producer prices and CPI stayed together:

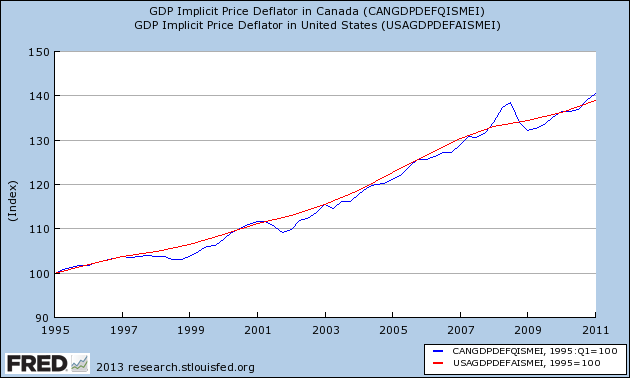

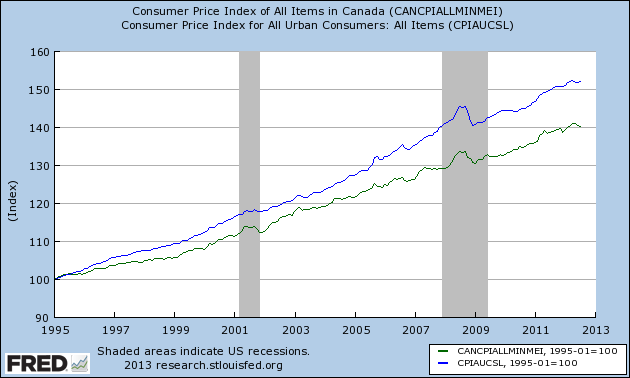

Gordon and Rowe’s focus is strictly on Canada, but given the hype surrounding NGDP targeting in the US, it might prove interesting to compare similar data. The following charts compare the GDP deflator and CPI between both countries over the same time period:

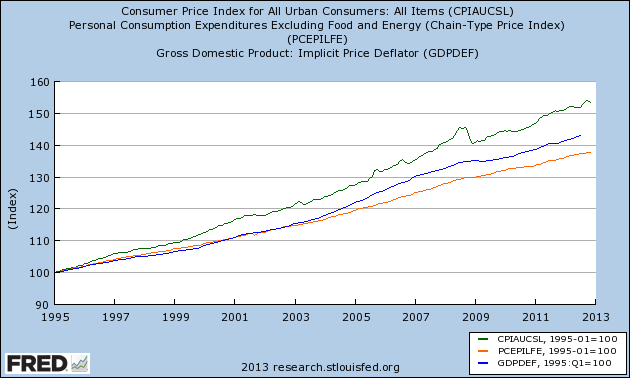

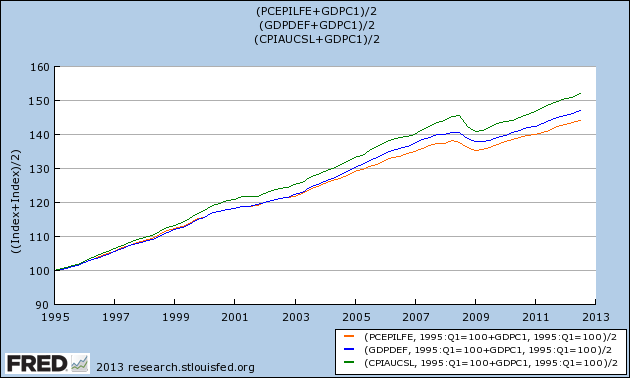

While producer prices between the two countries remained closely tied throughout the period, consumer prices in the US began diverging from their Canadian counterpart immediately and the gap continues to widen today. Shifting focus to the U.S., the data series for consumer and producer prices are combined into one chart. Returning to discussion of central bank policy, as well, it’s important to include the Federal Reserve’s preferred measure of inflation, core-PCE:

The inclusion of core-PCE helps resolve the discrepancy between consumer prices in Canada and the US. Of note is the dramatic difference between CPI and core-PCE over the past two decades. As I understand Fed policy, CPI (or PCE) is too volatile a target due to the wide swings in food and energy prices. Over time, however, the total and core measures are expected to converge. Depending on the time frame one assigns to the long-run (~18 years seems reasonable), the double-digit difference suggests that Fed policy has been looser than many believe. The Fed’s success has been limited to targeting core inflation, while food, energy and asset prices (not accounted for in CPI) have drifted significantly higher.

The inclusion of core-PCE helps resolve the discrepancy between consumer prices in Canada and the US. Of note is the dramatic difference between CPI and core-PCE over the past two decades. As I understand Fed policy, CPI (or PCE) is too volatile a target due to the wide swings in food and energy prices. Over time, however, the total and core measures are expected to converge. Depending on the time frame one assigns to the long-run (~18 years seems reasonable), the double-digit difference suggests that Fed policy has been looser than many believe. The Fed’s success has been limited to targeting core inflation, while food, energy and asset prices (not accounted for in CPI) have drifted significantly higher. Returning to Gordon’s chart and altering data to depict the US, these last two charts show a “counterfactual NGDP series for the scenario where producer prices and CPI stayed together.”

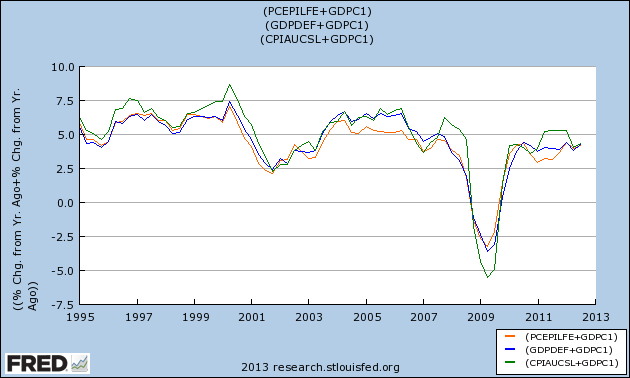

Regardless of the inflation measure chosen, the Fed’s policy was clearly too loose in the decade preceding the most recent recession. In fact, an interest rate targeting regime focused on core-PCE permitted the Fed to remain looser than it would have been following either of the other indexes.

Regardless of the inflation measure chosen, the Fed’s policy was clearly too loose in the decade preceding the most recent recession. In fact, an interest rate targeting regime focused on core-PCE permitted the Fed to remain looser than it would have been following either of the other indexes.Gordon concludes with “the question of what happens to the volatility of consumer prices if we adopted NGDP targeting.” Oddly enough, the divergence of core-PCE from the GDP deflator began around the same time the Fed started targeting core-PCE in 2004. Is it possible that the Fed’s actions altered the relationship between core-PCE and the GDP deflator? The similarities between Canada and the US during that period suggests not, but it’s worth considering. Separately, will the stark difference between CPI and core-PCE ultimately correct or has the world entered a new era of food and energy inflation?

My guess is that the volatility of core consumer prices will change only slightly under an NGDP targeting regime, while total consumer prices become far more volatile. Apart from my concerns about the viability of NGDP targeting, its effect on consumer prices raises important questions about wages and welfare costs. Hopefully these potential unintended consequences of NGDP targeting are being carefully considered before such a policy is actually implemented.

No comments:

Post a Comment