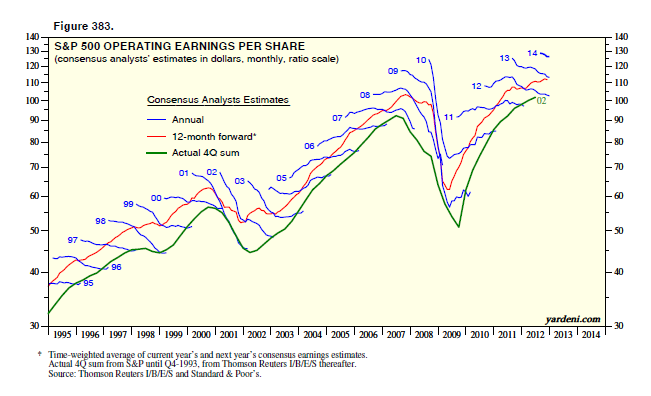

The estimates for 2012 and 2013 mostly fell all last year, yet the S&P 500 rose 13.4%. I have the Squiggles data back to 1979 on a monthly basis. More often than not, they tend to trend down; yet more often than not, the market has trended higher. That’s because the market discounts 12-month forward consensus expected earnings. A good proxy for this concept is forward earnings, i.e., the time-weighted average of consensus estimates for the current and coming years. It tends to be a good 12-month leading indicator for actual profits, with one important exception: Analysts don’t see recessions coming until we all do too.Woj’s Thoughts - After viewing this chart a few times, several observations stand out from the rest: 1) Each “earnings squiggle” that rises near the end is associated with higher actual earnings. 2) Each “earnings squiggle” that falls near the end forecasts at least a temporary decline in actual earnings. 3) Earnings estimates for 2010, at the beginning of 2009, were higher than forecasts for the current year (2013) and equivalent to current estimates for 2014. 4) The clear upward bias in estimates promotes higher prices, to the degree market participants trust the forecasts.

2) Why the US economic crisis is a depression and not a recession by Edward Harrison @ Credit Writedowns

What is now playing out in Congress is very much in line with what I said a little over three years ago in October 2009. Deficit fatigue has become too large to resist. Austerity is coming to the US. The crux here is to remember that this has been a crisis brought on by high private debt – not public debt or deficits. The government has been effective in preventing a private sector debt deflation by providing economic stimulus, permitting large-scale deficit spending and bailing out the banks. This has added a huge slug of net financial assets to the private sector and supported asset prices and private sector balance sheets. When these government deficits get cut, there will be serious pain in the private sector because balance sheets are still stressed and the result will be a relapse into economic depression.Woj’s Thoughts - The House Republicans have agreed to temporarily raise the debt ceiling and postpone the debate over sequestration in return for Congress (focusing on the Senate Democrats) actually passing a budget for the first time in four years. Backed into a corner, this is probably the best decision for the Republicans as it puts the onus (temporarily) on Democrats to reach a budget agreement. This progression raises the chances that spending cuts, either tied to sequestration or the budget, will take place this year. With the tax hikes already in place, the smaller deficits could very well lead to the outcome that Edward fears.

3) Ben Bernanke Is Facing A Legacy Problem by Bruce Krasting @ Money Game

Bernanke’s term at the Fed will set many historical precedents. To a significant extent, history will judge Bernanke on what he did while chairman of the Fed. But the books will also look at what happened after he left.

I believe that Bernanke would very much like to leave his successor with a Fed that had policy choices. As of today there are no options left. Just more useless QE. I doubt that Bernanke wants to exit with the Fed’s foot planted firmly on the gas pedal. The next guy does deserve a cleaner plate than now exists.

Is the Legacy factor influencing Bernanke? I think it has some sway in his thinking. Consider what Greenspan did before he left. After years of soft monetary policy he ratcheted up the Federal Funds rate 17 times in 22 months. He took the funds rate from 1% all the way up to 6%. Part of that rapid increase was driven to get monetary policy “neutral”, so that Bernanke could do as he wished. Not long after Bernanke took over, he took the funds rate down to zero.

Clearly, Greenspan tried to get monetary policy back to neutral before he left, I don’t see any reason why Bernanke would think differently. Are we watching a repeat of history? At a minimum, his legacy, and where he wants the Fed to be when he leaves, is part of Ben’s thinking today.

Woj’s Thoughts - It’s hard to argue with this logic given Greenspan’s actions as Fed Chairman prior to the last two years of his reign. While deserve is an overly strong word in this instance, my guess is the next Fed Chairman would appreciate having the option to ease, beyond merely expanding QE. With initial unemployment claims now at multi-year lows and a labor force still in decline, the table is set for a further meaningful drop in the unemployment rate. As the rate approaches 7 percent, I suspect Fed chatter about ending QE will pick up. If the legacy issue is simultaneously weighing on Bernanke’s mind, the urge to pull back on easing may be too great to ignore. Considering the ongoing multiple expansion in stock markets, it appears most market participants are not yet discounting this potential outcome.

Woj, If Senate Democrats we're smart, (I'm not saying they are), they would propose a budget that is the complete opposite of the austerity nature of the House budget. Call for more stimulus and raising of revenues, forcing the Republicans to clearly define what cuts they want. In other words, make the Republicans own the austerity they've been insisting is the only true path back to prosperity. What the Republicans and most average citizens fail to realize is that we have a serious private debt problem. Unless and until this problem is met, head on, there is no chance for meaningful, sustainable recovery. The level of student debt,which continues to rise as a result of high unemployment, forbearance and the inability to default on the debt is the next big crisis waiting to happen.

ReplyDeletenanute,

DeleteThat is certainly an interesting (wise) proposal. Unfortunately the Democrats also appear to accept the austerity doctrine, although neither party has yet to follow through.

You are right on target in highlighting the private debt problem. Recently people have been showing a chart about the debt service ratio reaching 30-year lows. What that chart fails to show is the breakdown among income levels, which would likely portray a very different picture for the bottom 80%.

Not sure your thoughts on student debt, but my instinct is that the resolution will ultimately involve massive write-offs by the government?

Woj,

DeleteThe student debt problem is the same as the bankruptcy "reform" legislation. They both suffer from the law of unintended consequences. On the student debt issue, I just don't see Republicans agreeing to massive write offs by the government. They (republicans), were the primary drivers of insisting on the current provisions that make it virtually impossible to repudiate student debt through bankruptcy. The reason being, that the government is the ultimate guarantor of the liabilities. The same problem arises in the mortgage industry. It is high time that the private sector assume the risk, or better yet, just have the government take over the student lending programs and cut out the middle man. Why on earth do we need private finance backed by public guarantees?

Woj, I forgot to address your point regarding the Democrats acceptance of the austerity doctrine. Are we all Austerians now? lol. While it certainly can be argued that some in the party hold this view, it is less so than on the Republican side of the aisle. The progressive, Keynesian side of the Democratic Party has been out of favor since the Chicago School of thought has taken hold in policy circles since the '80's. The irony is that the austerity crowd keeps insisting that deficits matter, and continue to propose budgets that increase the debt rather than reduce it at the expense of the consumer, middle class that fuels economic growth.

ReplyDelete