Potential Explanations

One might expect similar patterns to be evident also in other major asset classes, such as short-and long-term fixed-income instruments and exchange rates. Surprisingly, though, we don’t find any differential returns for these assets on FOMC days compared with other days. In other words, the pre-FOMC drift is restricted to equities. Further, we don’t find analogous drifts ahead of other macroeconomic news releases, such as the employment report, GDP and initial claims, among many others. The effect is therefore restricted to FOMC, rather than other macroeconomic, announcements. In the Staff Report, we attempt to account for standard measures considered in the economic literature that proxy for different sources of risk, such as volatility and liquidity, but they also fail to explain the return. Finally, we consider alternative theories that feature political risk, investors with capacity constraints in processing information, as well as models where stock market participation varies over time. Although these theories can help qualitatively explain the existence of a price drift ahead of FOMC announcements, they are counterfactual in some dimension of the empirical evidence.

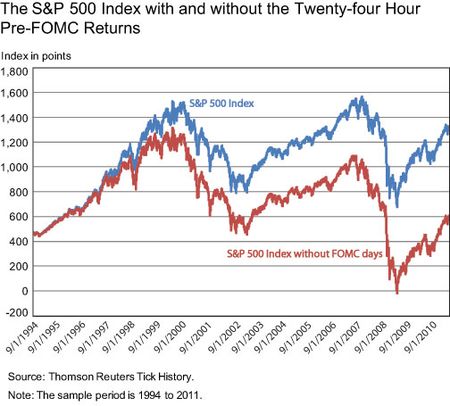

Our findings suggest that the pre-FOMC announcement drift may be key to understanding the equity premium puzzle since 1994. However, at this point, the drift remains a puzzle.Read it at Liberty Street Economics

By David Lucca and Emanuel Moench

Does anyone still need further proof of the Greenspan/Bernanke put? What I found most telling about this research note is that the positive effect of Fed anticipation extends to equity markets in Canada and Europe, but not to fixed income or exchange rate markets. As this correlation suggests, the expectations channel for Federal Reserve policy through equity markets is very strong. Unfortunately, for proponents of the Fed, the wealth effect from higher equity prices has minimal effect on GDP growth or employment.

No comments:

Post a Comment