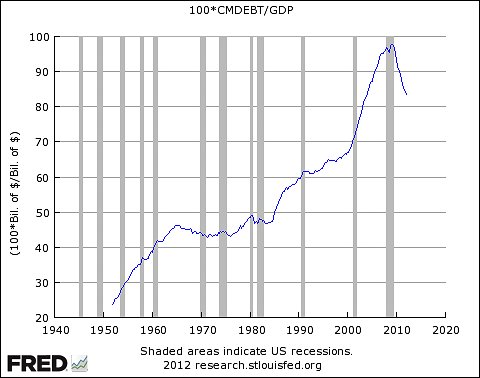

Second, a dramatic rise in household debt, which many of us now believe lies at the heart of our continuing depression. Here’s household debt as a percentage of GDP

Sumner says:

What do you see? I suppose it’s in the eye of the beholder, but I see three big debt surges: 1952-64, 1984-91, and 2000-08. The first debt surge was followed by a golden age in American history; the boom of 1965-73. The second debt surge was followed by another golden age, the boom of 1991-2007. And the third was followed by a severe recession. What was different with the third case?The difference is the aggregate amount of household debt compared with incomes (GDP). The use of credit (debt) instead of money (income + savings) has an extra cost associated with the interest payments. As the aggregate amount of debt rises, aggregate interest costs follow. To simply stem the rise in debt, let alone maintain the current level, an increasing percentage of income and savings becomes necessary to cover interest costs and/or pay back previous debt. These actions reduce the amount of income and savings available for consumption and investment, creating a drag on economic growth.

Since households are no longer in a position to drive growth, other sectors must pick up the slack to prevent incomes from stagnating or falling. If incomes struggle, many households will have to shift an even larger percentage of income to paying interest and debt, while others simply become unable to repay the full amount. This deleveraging worsens the contraction from the household sector and leads to losses within the corporate and financial sector. If those sectors are equally leveraged with debt (as was the case in the US) then the losses in income and capital may cause those sectors to reduce spending and lending, respectively. This process can ultimately generate a vicious cycle where attempts to deleverage by each group reduces the income of others and subsequently increases the burden of debt. Absent growth in income from either the public or external sectors, this cycle will eventually slow but at a much lower level of GDP.

Update: The Arthurian continues to dissect the Monetarist disregard of rising household debt levels:

During the famous flat spot of 1965-1983, the comparable rate of debt growth was 9.36%. That's near 90% of the growth rate for the 1952-1964 "debt surge" and it is higher than the growth rate for the third debt surge Sumner identifies.

There was no remission. Debt did not stop growing. It barely slowed.

Prices increased at a compound annual growth rate of 6.6% per year between 1965 and 1983, more than tripling during those years. There was no remission of debt. There was only erosion of debt because of the inflation.

I am speechless. You actually just made me want to learn more about this topic. Your blog has developed into a stepping stone for me, my fellow blogger. Thank you for the detailed journey.

ReplyDelete