The quote from the last FOMC minutes suggested the Fed wanted a "new tool". Well here ya go Ben, take the IOER to -25bps, take 2s to -50bps and watch banks start setting LIBOR negative!! If you really want to push the portfolio balance channel this will wake up all the sleeply reserve managers with liquidity needs in USD. Of course as short rates plunge into negative territory, inflation expectations will rise sharply. It will be important to not expect too much love for the long end if this happens. And like I said above, even if this is a low probability event, the mere possibility of it happening makes levered longs in the front end a fantastic trade! No one is prepared for it. Just ask yourself how many risk management departments have shocked 2yr notes to -50bps and 3ml to -30bps in their VAR analytics. Not many!!Many investors seem to view this action positively, believing the resulting increase in bank lending will lead to higher growth and inflation. Before presenting the likelihood of such an action by the Fed, it’s important to clarify the major effects of making IOER negative.

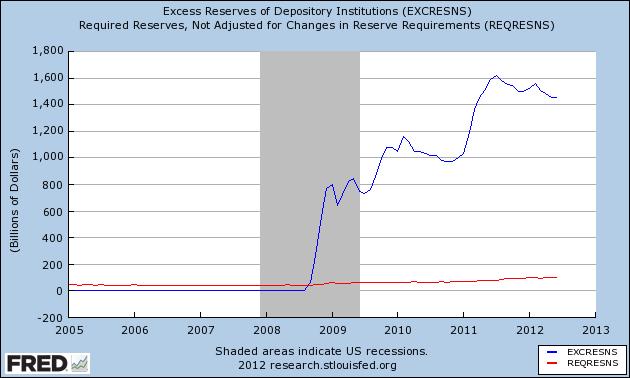

Currently, banks are holding approximately $1.45 trillion in excess reserves:

As Mish Shedlock and Steve Keen have recently reconfirmed, banks cannot lend reserves. Reserves are brought into existence and removed from the system through open market operations. The Fed therefore controls the amount of reserves in the system, as a helpful tool in maintaining its interest rate policy. Since members of the Fed/FOMC and most economists view QE as monetary stimulus, I presume that the Fed will not elect to accompany a reduction in IOER with a policy of reversing QE and reducing its balance sheet. If the IOER becomes negative, given that assumption, banks will face a decision between increasing lending to drive up required reserves or continuing to hold excess reserves at a penalty rate.

Faced with this decision, banks may initially seek to increase lending. The drop in IOER acts similarly to a rate cut and at a negative rate may encourage banks to even extend loans that, though not directly profitable, are expected to lose less than the cost of holding corresponding excess reserves. Regardless, the amount of new borrowing required to significantly reduce excess reserves is inconceivable (a 10% reserve requirement suggests $14 trillion). The current amount of excess reserves will therefore likely remain well above $1 trillion, which is bad for banks and stocks.

Why? Well, given the current IOER rate, banks are effectively earning $3.5 billion per year, risk-free ($1.4 trillion * 0.25%). Flipping the current IOR to negative and maintaining a similar level of excess reserves suggests a yearly drain from the financial system of $3.5 billion. This reduction in profitability will hurt bank capital, which is ultimately the real constraint on bank lending.

While a negative IOER will lower bank profits, it will likely increase profits at the Fed (which are transferred to the Treasury). As Zervos points out, this policy change could also push short-term Treasury rates (at least out to 2-years) negative. If that occurs, holders of short-term Treasury notes would join banks in effectively paying the Treasury to hold funds (ie. negative interest income). Although the combination of these factors will reduce the deficit, it will simultaneously reduce net financial assets of the private sector. In that sense, a negative IOER is equivalent to raising taxes.

Absent countervailing measures to increase the deficit, a reduced deficit will also result in declining corporate profits (ex-Fed). As I’ve noted previously, the federal deficit has been the primary factor supporting corporate profits over the past few years. With a corporate profit recession already in our midsts, this decision by the Fed could result in a corporate profit depression.

In my opinion, any optimism regarding a negative IOER is badly misplaced. Rather than sparking new lending, this change in monetary policy will likely bring about the reverse by hurting bank profits and capital. By inflicting a “tax” on the broader private sector, a negative IOER could even dampen corporate profitability and incomes. In the end, a policy of negative IOER might be enough to inspire a massive sell-off in stocks and push the US economy into recession.

To end on a positive note, I believe it is highly improbable that Bernanke or the Fed enacts such a policy. Apparently Goldman agrees.

(Note: Above I mentioned Zervos’ view that a negative IOER rate would lead to negative short-term Treasury rates. I haven’t had enough time to fully think through the possibility, but my initial reaction is skeptical. Other countries currently with negative rates on short-term government debt are either engaged in a monetary union or maintaining a currency floor. Government debt in those instances therefore, apart from safety, also provides an effective call option on higher relative currency valuations. Given that the US dollar is a floating currency, investors/savers could presumably hold dollars instead of Treasuries. This could cause a rise in the dollar exchange rate but would probably keep rates from going negative (absent the Fed adjusting lower the Fed Funds rate). I’ll plan to do a follow post on this topic in the near future but, in the meantime, does anyone have helpful thoughts on this topic?)

WOJ,

ReplyDeleteNot sure, but wouldn't lowering the IOR rate have a corresponding lowering of the target Fed Funds rate? Furthermore, aren't real short term rates already negative, once you adjust for inflation? Or, are you talking about nominal rates being negative?

The Fed wouldn't have to lower the target Fed Funds rate, but given the amount of excess reserves may face trouble in maintaining the current target. The Goldman link above offers a quote from Bernanke to this effect.

ReplyDeleteAs for rates, you are correct that real short-term rates are currently negative. The above piece is discussing the potential for negative nominal rates.

Woj,

ReplyDeleteSeems like a bit of a paradox, no? Can't lower rates for fear of setting off a panic and sell off in the market, while at the same time, keeping IOR's pat seems to perpetuate the "stalemate." Isn't this current policy, in effect, creating a new bubble in the market? Eventually reserve levels will have to come down and rates will have to go higher. it's the second part of the Fed's dual mandate that needs attention.

No paradox, IMO. The Fed could lower the IOER to zero without much damage, although it would slightly hurt bank profits/capital. I don't see current policy as a stalemate, however, because the Fed lacks any real transmission mechanism by which to engender greater real growth or employment at this time. The issue remains excessive private debt, which requires fiscal policy.

ReplyDeleteAs for a new bubble, if there is one my bet is on US equities. Corporate profits are now declining, yet the market remains positive on the notion of further monetary stimulus (which does little for profits).

The main problem with zeroing the deposit rate or even worse turning it negative is that it hurts the money markets heavily, and will basically make them shrink and leave the central bank as the main market maker.

ReplyDeleteTake the Euro case for example. As long as the ECB kept the deposit rate at 0.25% banks had two profitable trades:

1) Borrow repo short-term from investors with no access to the ECB deposit facility (such as MMMFs) and deposit the funds at the ECB to earn a spread (repo rates were around 0.15%).

2) Earn the bid-offer spread.

Trade (1) is not available anymore while with repo rates at 0.01% or zero/negative, bid-offer spreads almost do not exist. Based on these fees, participants cannot even cover transaction costs, especially for short-term repos (overnight, weekly etc): http://www.eurexrepo.com/euro/principles.html

My view is that various government paper which turns special is used in reverse repo deals which allow earning a profit even with negative rates and push yields negative for more government securities.

A negative deposit rate will make bank reserves and banknotes earn the same (negative) return. I don't see how making them functionally equal can provide stimulus.

This situation was faced in Japan as well, where the BoJ ended up being the main market maker. I don't think you want to do that in the US money market.

http://www.bis.org/publ/work188.pdf section 3.3

Kostas - Very good points. The ECB's actions seem more likely to hurt bank profits/capital and subsequently restrict lending, rather than encourage greater supply of credit. I certainly don't like the Japanese outcome but in many ways the US and Europe appear inching further towards something similar.

DeleteWOJ and Kostas:

ReplyDeleteIt is true that the banks' profit can be hurt if reserve interest becomes negative, assuming that putting money to the Fed is the only thing banks are doing to make a profit. BUT THAT IS EXACTLY THE PROBLEM. A commercial bank's biz model used to be taking deposits and lend them to business. The role of the commercial banks is to examine and price the credit risks in the economy. But now, like Kostas showed in her comment, commercial banks have become pure broker dealers. They make money by flipping paper, instead of analyzing, pricing and extending credit.

Now I do not mean to oversimplify the problem we are facing. In fact, commercial banks, since their merger with the investment banks, have undergone the dis-intermediation for the past 30 years. The business model has changed from lending loans, to initiating the loans, packaging them, and sell them off at a profit, paper flipping model just like a security dealer, but on steroid with the much larger capital a deposit bank can command. The percentage of C&I loans actually held by commercial banks have dropped to below 25% of total loans outstanding. I suspect that banks today do not even have the adequate systems anymore to run a large commercial loan operation. They have to learn again how to analyze credit risk without the pricing from the securitiztion market. This is probably ONE of the reasons why banks are not lending.

Overall, I agree with your assessment that a zero reserve rate may not get banks start lending again. However, my view is that this points to something that is fundamentally wrong with the financial system and the role the commercial banks are supposed play in an economy. It should be changed, but can only be changed with regulatory actions, not just monetary operations by Fed. Repeal Glass-Steagle is a start.

MX,

DeleteThe banking system as a whole cannot get rid of reserves aside from converting them to currency (which seems highly unlikely). Therefore, reducing the rate will hurt financial sector profits in the aggregate without trying to determine how it will impact new lending or other profit streams. One are where my views slightly differ is that I believe bank lending is, in part, constrained by the lack of credit-worthy demand (by which I mean already over-indebted households/corporations).

Other that that, I think we're largely in agreement. The regulatory environment subsidizes, and thereby encourages, many of the practices you highlight as being problematic. The Federal Reserve, within its current statute, can do very little to reduce the private sector debt burden that restrains demand and dampens spending (for both consumption and investment). Fiscal policy, including regulatory changes, are clearly necessary to reduce the volatility and inequality stemming from the financial sector.

Joshua:

DeleteMany have confused the fact of the constancy of overall reserve funds with the act of lending. You are correct that the overall reserve size cannot be changed by banks because that is determined by the size of the asset side of the Fed's balance sheet. But that fact is not what people are debating with. No doubt, money will always come back to the Fed's balance sheet, that is just the consequence of the fact that only Fed can create, and destroy, total money base. But what is being debated is not where the final destination of money. What is being debated is the PATH of money before it returns to Fed's balance sheet.

Right now, the money Fed created by QE goes to the banks and come back right away to Fed, the shortest path possible. The debate is whether by lowering IOER, the money will take a longer path, for example, from Fed to the banks, then to the business, then to the suppliers, then to the customers, then to the banks again, then back to Fed. The longer this PATH takes, the more economic activities will be put into motion, (and yes, by the same amount of TOTAL reserve funds), and hopefully that is going to help the economy.

So this is the debate, not the total size of reserve, it is the path, the turnover, the speed of the money that makes up the reserve we are debating about.

I agree that it may not be the case the money will flow to business and used in production and capacity expansion. There are just too many "distractions" in the economy today that seem to offer much quicker ways of making a profit - commodity, derivatives, PE funds, etc etc.. Money can easily flow into more financial operations to distort supply and demand (and ultimately market prices) rather than productive economic activities.

But I disagree with notion that even in theory lower IOER cannot divert more money to lending.

Joshua:

DeleteYou do make a good point that the consumers are already heavily indebted, although I think business are as a whole are awash with cash after hoarding it for the past 2 years. In either cases, there is a strong argument that there is sheepish demand out there for credit.

However, I often wonder, which is just an unsubstantiated hunch, whether there are lots of demand for credit out there from new business, or potential business, small business, that is unmet with banks because they are less credit established.

Ultimately, I think people have to realize that the loans market has long changed from what we think it is. Banks don't evaluate and lend loan anymore. Banks have become initiator and brokers of loans. The loans are evaluated and invested by capital market at large in the form of CLOs. With the CLO market suddenly went from $1tr a year to nothing, suddenly banks lost the pricing mechanism and the ultimate takers of the loans.

I always have thought in the past this is a big advance forward in the US financial system, because now it is the market that ultimately prices the risk of credit. I always thought more people making decision have got to be better than a few loan officers. But now market has proven its fragility. This discussion goes beyond that of financial system. Can you trust a market that is driven solely by greed can somehow balance out all the cheats and misconducts and produce a system that is productive to the society as a whole?

I don't have the answer yet.

MX,

DeleteIn terms of the corporate sector, I think the claims about firms being "awash with cash" are a bit misleading. Companies are holding a greater percentage of assets as cash these days, but they also have significantly more debt on the balance sheets. If firms were to use cash to pay off the debt, they would therefore seemingly be in a worse financial position, which makes little sense.

As for small businesses with less established credit, the idea sounds plausible. I don't see how the Fed can alter the banks determination of credit-worthy without implicitly/explicitly promising to cover any corresponding losses.

Lastly, regarding the markets, I don't believe one can eliminate greed/self-interest from humanity, hence it makes little sense to try. The important thing is to establish institutions that allows those incentives to work towards trade and providing the greatest number of goods. You shouldn't trust markets to perform perfectly just as you shouldn't expect governments to avoid the incentive traps that lead to regulatory capture, etc. The question is more accurately, given our desired ends and real-world constraints, which system is likely to encourage the means that achieve those ends?

Well said.

Delete