New research confirms that the Federal Reserve’s monetary policy has little effect on a number of financial markets, let alone the wider economy. Politicians, and a few economists, have been imploring the Federal Reserve to help the economy grow before November. But the effects of monetary policy on the wider economy are small.Although I have repeatedly attempted to show that, under current conditions, monetary policy would be largely ineffective at stimulating the broader economy, this should not be taken as a dismissal of the general potential for monetary policy. Cullen Roche chimes in on the subject with a conclusion that sums up my views:

monetary policy has been very weak in the current environment for several reasons. The primary reason is due to a lack of demand for debt. Consumers are saddled with excessive debt so demand for “inside money” has been abnormally weak in recent years. This is perfectly normal following a credit driven bubble. And since monetary policy primarily works through altering the cost of “inside money” it’s not surprising that the actions of the Fed have appeared rather ineffective in recent years. But this unusual environment should not be taken to mean that the Fed has zero options or that monetary policy is never effective. To do so would be a vast misunderstanding of the basics of banking and the way our monetary system works. Monetary policy might be a blunt instrument at times, but let’s not make extreme comments that sound ideological or take the uniqueness of today’s environment to make sweeping generalizations.Beyond this main issue concerning the effectiveness of monetary policy, Mulligan’s post raised the question of whether the Federal Reserve controls long-term interest rates. Since the Federal Reserve could purchase all outstanding Treasuries at a given price/yield, I think it’s fair to say the potential power for strict control exists. A more basic question, however, is whether past and current policy displays control over long-term Treasury rates. I’ve argued affirmatively, drawing on comments from Edward Harrison, Gary Becker and others, that long-term Treasury rates are primarily a function of expected short-term rates over a given period. JW Mason, whose work I highly regard, disputes this claim:

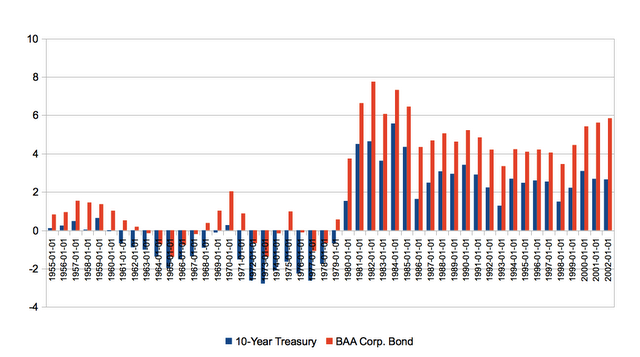

it's not at all obvious that long rates follow expected short rates either. Here's another figure. This one shows the spreads between the 10-Year Treasury and the Baa corporate bond rates, respectively, and the (geometric) average Fed Funds rate over the following 10 years.

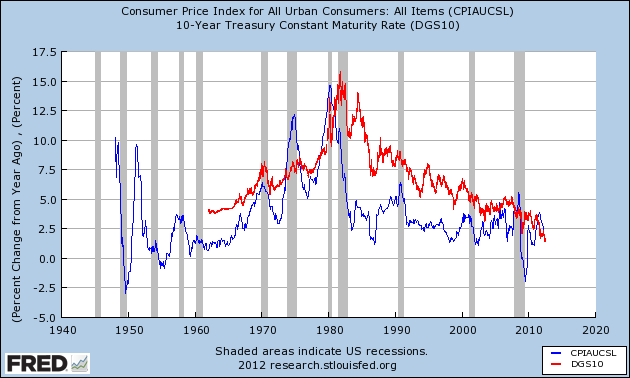

If DeLong were right that "the long government bond rate is made up of the sum of (a) an average of present and future short-term rates and (b) term and risk premia" then the blue bars should be roughly constant at zero, or slightly above it. [2] Not what we see at all. It certainly looks as though the markets have been systematically overestimating the future level of the Federal Funds rate for decades now. But hey, who are you going to believe, the efficient markets theory or your lying eyes?From my perspective, this preliminary conclusion from Mason confuses expected average rates with actual outcomes. Although I can’t speak for DeLong (or others), the notion that markets might/have systematically overestimated and underestimated future Fed Funds rates does not undermine the theory. As the following chart shows, inflation and 10-year Treasury rates were primarily rising from the early 1960’s until the early 1980’s. Based on economic theory at the time (e.g. Phillips curve), it was not unreasonable to expect that inflation would subside with increasing unemployment and the Federal Reserve would lower rates in response. The unexpected persistence of inflation likely caused many investors to consistently underestimate future Fed Funds rates during this period.

By the time Paul Volcker took over as Chairman of the Federal Reserve, many (most) investors had probably come to expect persistent inflation. When inflation crashed in the early 1980’s, it would have been equally reasonable to expect a return to high inflation and Fed Funds rates. The actual outcome has been largely subdued inflation, now going on 30 years. To understand how unexpected this outcome was, one only has to consider that returns on long-term Treasuries has exceeded returns on stocks during this 30-year period (a previously unthinkable feat missed by nearly all investors).

Mason continues his post with the counter claim that:

What profit-maximizing bond traders do, is set long rates equal to the expected future value of long rates.

I went through this in that other post, but let's do it again. Take a long bond -- we'll call it a perpetuity to keep the math simple, but the basic argument applies to any reasonably long bond. Say it has a coupon (annual payment) of $40 per year. If that bond is currently trading at $1000, that implies an interest rate of 4 percent. Meanwhile, suppose the current short rate is 2 percent, and you expect that short rate to be maintained indefinitely. Then the long bond is a good deal -- you'll want to buy it. And as you and people like you buy long bonds, their price will rise. It will keep rising until it reaches $2000, at which point the long interest rate is 2 percent, meaning that the expected return on holding the long bond and rolling over short bonds is identical, so there's no incentive to trade one for the other. This is the arbitrage that is supposed to keep long rates equal to the expected future value of short rates. If bond traders don't behave this way, they are missing out on profitable trades, right?

Not necessarily. Suppose the situation is as described above -- 4 percent long rate, 2 percent short rate which you expect to continue indefinitely. So buying a long bond is a no-brainer, right? But suppose you also believe that the normal or usual long rate is 5 percent, and that it is likely to return to that level soon. Maybe you think other market participants have different expectations of short rates, maybe you think other market participants are irrational, maybe you think... something else, which we'll come back to in a second. For whatever reason, you think that short rates will be 2 percent forever, but that long rates, currently 4 percent, might well rise back to 5 percent. If that happens, the long bond currently trading for $1000 will fall in price to $800. (Remember, the coupon is fixed at $40, and 5% = 40/800.) You definitely don't want to be holding a long bond when that happens. That would be a capital loss of 20 percent. Of course every year that you hold short bonds rather than buying the long bond at its current price of $1000, you're missing out on $20 of interest; but if you think there's even a moderate chance of the long bond falling in value by $200, giving up $20 of interest to avoid that risk might not look like a bad deal.Once again, I think this example confuses some aspects of bond trading. While Mason considers a bond in perpetuity, let’s instead consider a 10-year Treasury with a 4% yield and 2% Fed Funds rate expected to continue indefinitely. Now assume that this expectation for the Fed Funds rate holds true. Entering year ten, if prices don’t adjust, investors will have the option of purchasing notes with equal maturities (the 10-year Treasury only has a year remaining before maturity) that offer either a 2% or 4% yield. Given the option, investors will purchase the 4% note, pushing the price up and yield down until it reaches approximately 2%. Even if 10-year Treasury rates are still 4% at that time, the previously held bond no longer has a long-term maturity and becomes the equivalent of a short-term note/bill. This is why the expected short term rates, and not long-term rates, matter for controlling long-term Treasury rates.

Despite our differences in opinion over influencing long-term Treasury rates, Mason and I agree that:

for policy to affect long rates, it must include (or be believed to include) a substantial permanent component, so stabilizing the economy this way will involve a secular drift in interest rates -- upward in an economy facing inflation, downward in one facing unemployment. (As Steve Randy Waldman recently noted, Michal Kalecki pointed this out long ago.)Currently, unemployment and disinflation are persisting far longer than most economists, politicians and investors expected. These outcomes have led the Federal Reserve to maintain a zero percent Federal Funds rate for three years and predict continuation of that policy for at least a couple more. As investors become increasingly convinced that short-term rates will remain at or near zero indefinitely, long-term Treasury rates have continued the secular drift lower that began in the early 1980’s.

So yes, the Federal Reserve can control long-term Treasury rates and has been doing so by adjusting market perceptions of future Fed Funds rates. Unfortunately, as Mason says:

adjusting expectations in this way is too slow to be practical for countercyclical policy.Monetary policy, in a future crisis, will once again have its time to shine. For now, fiscal policy must take center stage to reduce household debt burdens and counteract previous measures aimed at inducing a credit bubble.

No comments:

Post a Comment