Today, I think Marcus Nunes (another Market Monetarist) is making a similar mistake in highlighting Australia’s consistent growth as a success of monetary policy. There are many charts in Marcus’ post, but I presume an important one to highlight is Australia’s NGDP during the past two decades (the post compares the relative success of Australia to New Zealand):

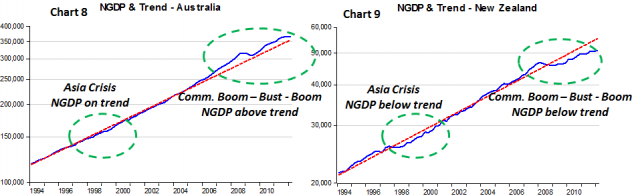

Chart 8 is intended to depict how monetary policy maintained NGDP growth near trend through the Asia Crisis and above trend throughout the global financial crisis. A concern of many non-Market Monetarists is what portion of NGDP growth will be derived from inflation versus real growth. To address that question, Marcus offers the following chart and notes:

Chart 8 is intended to depict how monetary policy maintained NGDP growth near trend through the Asia Crisis and above trend throughout the global financial crisis. A concern of many non-Market Monetarists is what portion of NGDP growth will be derived from inflation versus real growth. To address that question, Marcus offers the following chart and notes:

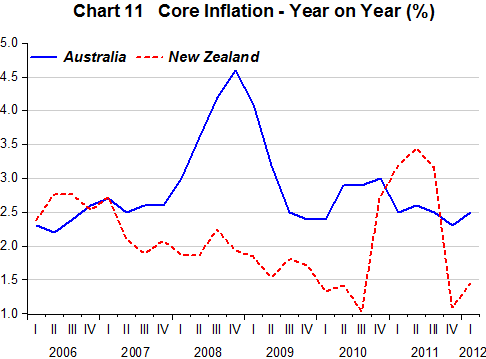

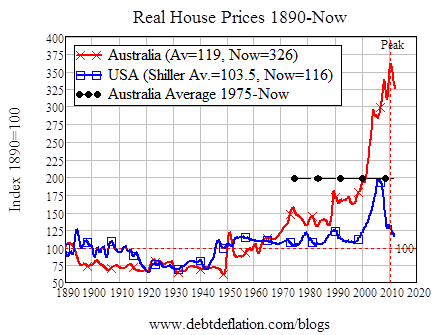

Chart 11 shows that generally, inflation has not been an ‘issue’ in either country.If I knew little about the Australian economy, Marcus’ display of graphs and explanation might prove very convincing. However, having long been a fan of Steve Keen (an Australian economist), I was surprised at the lack of discussion regarding Australia’s housing market. Keen, a highly regarded Post-Keynesian, has for years been pointing out the positive and negative effects of private credit on growth. Regarding this topic, Keen frequently points out similarities between the US and Australia. Here’s a chart from Steve’s blog comparing Australian and US real house prices:

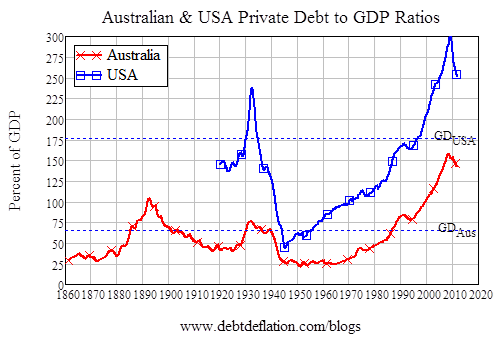

After nearly doubling between the mid-1990’s to 2005, US house prices have now given back most of the gains. Meanwhile, in Australia, house prices nearly tripled from the late-1980’s to the recent peak in 2010. Currently house prices remain at levels double those witnessed in the mid-1990’s. Similar to the US, the rise in home values is not well accounted for in national inflation data. As Keen regularly notes, a major factor in both housing bubbles and macroeconomic cycles (frequently overlooked by mainstream economists and monetarists) is private debt. Below is a chart comparing the levels of private debt in Australia and the US:

During the extended period of growth in Australia, private debt to GDP has been growing consistently. The rise in private debt and housing prices, which supported Australian growth for two decades, have now turned south. Similar, more exaggerated, drops in the US were at the heart of the US crisis and continuing economic malaise. As the housing bubble in Australia busts and private sector deleveraging speeds up, the Australian central bank (RBA) will be unable to overcome the deflationary momentum. GDP growth in Australia has been slowing of late and the most recent unemployment report showed a surprise uptick. If Keen is right, monetary policy is likely to prove inept in the coming years as NGDP falls below trend without large fiscal stimulus.

The US experienced a great-run of economic growth on the back of a staggering rise in private debt that ultimately caused the subsequent crash and stagnation. Australia appears to have built its remarkable run on the same principles and will soon find out if the optimism was equally misplaced. Market Monetarists are claiming Australia a success, while the Post-Keynesians are warning of impending trouble. My bet is on Steve Keen and the Post-K’s. Where’s yours?

Yes my bet is on Keen. But I'm not surprised there was little talk of debt and credit from the MMs. It's my impression they know little about Keen's work - mainly because of what Keen characterises as their "effortless superiority".

ReplyDeleteThat failure is a long time coming. I agree completely that Australian housing prices are a series of bubbles and that many Australian households are highly leveraged on bureaucratic approval. But the air was out of the various American housing bubbles before the GFC or Great Recession hit. The former was a result of (1) some bizarre evolution in financial instruments, (2) poor prudential regulation, (3) a pattern of the destruction of prudence by intervention and the (4) US Fed deciding to go with specific credit management rather than general liquidity support. It then proceeded to (5) disinflate by "passively" tightening monetary policy while (6) entirely fail to anchor income expectations.

ReplyDeleteIn the case of Australia, (1) does not apply anywhere to the same degree (2) is likely rather better (but as yet not seriously tested by a domestic crisis rather than an imported one) (3) does not really apply (4) is not something the RBA is likely to do, (5) it won't do and (6) it does the reverse.

Like Keen, I admire Fisher's Debt-Deflation analysis of the Great Depression. But that analysis was in the situation of massive deflation imposed on the goldzone by the Bank of France abetted by the US Federal Reserve. You need seriously destructive monetary policy to get the effect.

Yes, it will be ugly when the bubbles burst but better monetary policy than the Fed managed will make things a lot less ugly in Australia when and if the housing bubbles burst (rather than subsiding).

I have done a response post with links added:

ReplyDeletehttp://lorenzo-thinkingoutaloud.blogspot.com.au/2012/07/rba-is-not-fed-thank-goodness.html

Lorenzo,

DeleteThanks for the reply and thoughtful comments. I completely agree that the Fed was far too passive in reacting to the housing bust and the ensuing liquidity crisis. However, I don't believe the Fed was/is equipped to deal with the solvency issues that arose in the financial sector or the private sector deleveraging. If the RBA is more proactive, which still seems open to question, then I agree the fall in NGDP and subsequent stagnation will likely not be as bad as the US. That outcome, while better, still leaves a lot to be desired with regards to central banks maintaining a consistent rise in NGDP.

http://www.ft.com/cms/s/0/6cf1dd88-b96c-11e1-a470-00144feabdc0.html#ixzz20YLQsSue

ReplyDeleteJune 20, 2012 10:43 pm

Hey, the sky hasn’t fallen after all ...

From Mr Rory Robertson.

Sir, Steven Keen, whom you quote in “Mine, all mine” (Analysis, June 18), notes that nominal house prices in Australia have risen by “a factor of six since 1986”, and forecasts a dismal road ahead for Australia’s housing markets. He overlooks the fact that household disposable income rose five and a quarter times over the same period, and that the collapse of inflation in the early 1990s means that mortgage rates since then have averaged about half their 1980s levels.

Readers might be amused to know that Prof Keen is famous in Australia because in 2008 he took a high-profile bet that house prices would fall by 40 per cent from “peak to trough”. It was agreed that the loser would trek across 230km of dull roads from Canberra, the nation’s capital, to the top of Mt Kosciuszko, the nation’s highest “peak” (only 2,228m), wearing a T-shirt saying: “I was hopelessly wrong on home prices! Ask me how”.

In the event, home prices in that episode fell by 5 per cent, not 40 per cent. Wrong by a factor of eight but still a good sport, Prof Keen enjoyed a nine-day holiday trekking the tar to Mt Kosciuszko. Awkwardly, average home prices today remain 10 per cent or so above the level at which “Australia’s Chicken Little” sold his home in favour of renting in 2008. The bet now is that pensions will grow faster than rental costs over the next four decades.

Apparently the RBA has reversed its course back to being hawkish (http://www.macrobusiness.com.au/2012/07/hawkish-rba-backflips/). Considering the broad global slowdown, the RBA may yet prove itself equally as inept as the Fed/ECB in implementing proactive monetary policy.

ReplyDelete