Duke professor Michael Munger and LearnLiberty come together in this wonderful and short video about externalities and Pigouvian taxes (h/t Cafe Hayek):

This past semester I was fortunate to attend lectures by Professor Munger on two different occasions. His humor and knowledge of economic history, highlighted toward the end of the video, make his presentations especially enlightening and entertaining. If you have the opportunity to hear him speak in the future, I highly recommend the experience.

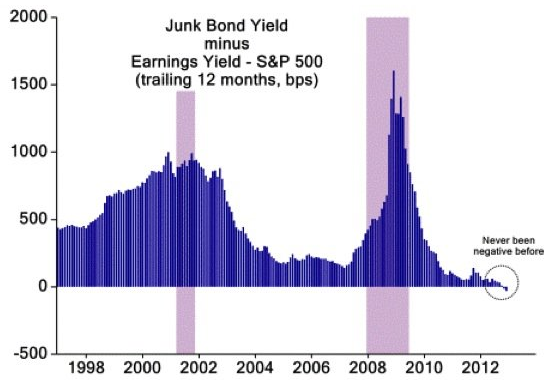

“The chart below shows the spread between the yield on junk bonds and the yield received from holding stocks. The spread recently turned negative for the first time ever, showing just how much the yields on high-risk bonds have come down as central banks keep benchmark borrowing rates depressed and investors search further out on the risk spectrum for yield.”

Woj’s Thoughts - This chart, more than almost any other, may highlight the potential harm induced by the Federal Reserve’s attempts to push private investors further out on the risk spectrum. Unless junk bond companies have truly become significantly less risky, when the next round of increasing defaults begins, investors will find that current yields fail to even remotely compensate for future losses. Stocks may currently be slightly overvalued from a historical perspective, but certainly not compared with junk bonds.

I have long believed that the problem market economies have with statists is misunderstood.

Pro-market folks tend to think that statists just don't understand markets. And to some extent that's true. But the real problem is that statists have too much faith in markets.

Wait...too MUCH? How can that be? (More after the jump...)

The Fed buys the IOU from my lender. The lender gets cash. And I get to make the same payments I made before, except now I pay somebody else. That really doesn't do much for me. It doesn't do much for the economy, either.

Purchasing assets removes those assets from the economy, replacing them with money. But the liabilities remain as they were: draining income, depressing demand, hindering economic growth.

Woj’s Thoughts - Art explains in a very straightforward manner the basic problems with QE. If the heart of the issue is excessive debt, asset swaps do basically nothing to reduce household liabilities while removing interest income from the private sector. I think Art goes a bit too far in suggesting the Fed cancel private liabilities outright since explicit fiscal policy should be left to elected officials.

“Neoclassical economics has since long given up on the real world and contents itself with proving things about thought up worlds. Empirical evidence only plays a minor role in economic theory, where models largely function as a substitute for empirical evidence. Hopefully humbled by the manifest failure of its theoretical pretences, the one-sided, almost religious, insistence on axiomatic-deductivist modeling as the only scientific activity worthy of pursuing in economics will give way to methodological pluralism based on ontological considerations rather than formalistic tractability. To have valid evidence is not enough. What economics needs is sound evidence.”

“Those who glibly speak of ‘market clearing prices’ tend to forget that over wide areas of modern markets it is not with this purpose in mind that prices are set. They seem unaware of the important insights into the process of price formation, an Austrian responsibility, of which they deprive themselves by clinging to a level of abstraction so high that on it most of what matters in the real world vanishes from sight.”

At The Everyday Economist some months back, Josh Hendrickson captured my attention with hisNominal Income and the Great Moderation. In that post, Hendrickson introduced a forthcoming paper and said:

As I argue in the paper, during the Great Inflation period of the 1970s, members of the FOMC regularly asserted that the process of inflation determination had changed. Relying on public statements and personal diary entries from Arthur Burns, I demonstrate that there is little evidence that the Federal Reserve was less concerned with inflation during the 1970s. Rather, the view of Burns and others was that inflation was largely a cost-push phenomenon. Burns thought that incomes policies were necessary to restore price stability and stated that “monetary and fiscal tools are inadequate for dealing with sources of price inflation that are plaguing us now.”

The shift in policy, beginning with Paul Volcker, was an explicit attempt to stabilize inflation expectations and this was done deliberately at first through monetary targeting and ultimately through the stabilization of nominal income growth. Gone were notions of cost-push versus demand-pull inflation.

I can see a natural progression there: from the thought that "incomes policies were necessary" to policies for "the stabilization of nominal income growth." Incomes policies meanswage-and-price controls. The method is crude, but the objective of wage and price controls is precisely "the stabilization of nominal income growth."

Beside the point. What concerns me is "the view of Burns and others was that inflation was largely a cost-push phenomenon." That, and the apparent fact that this issue of cost-push was never resolved. It was simply dismissed.

As with many aspects of science, there is an inherent desire to find one all-encompassing explanation for macroeconomic phenomenon. Maybe it’s naivete, or pragmatism, but there seems little reason to expect one simple reason behind inherently complex phenomena. Returning to inflation, maybe a simple primary cause exists at certain periods of time and in certain locations, but throughout history there may very well be numerous causes.

Approaching the question of inflation from a Keynesian perspective, it seems obvious that demand-led inflation is plausible. Individual’s desire for goods can clearly shift faster than the economy’s ability to produce new output. Similarly, from a Monetarist perspective, one can easily envision an excess supply of money causing a decline in its value that represents an increase in the price level. Or, as Nick Rowe suggests,maybe monopoly power causes inflation.

While all of the above views likely have their time and place, a way to reconcile cost-push inflation with today’s circumstances may not exist within mainstream models. In The Bubble and Beyond, by non-mainstream economist Michael Hudson, a case is made whereby rising interest expenses on debt could generate cost-push inflation. Over the past 30 years, there has been a massive increase in the amount of private debt both at the household and corporate levels. The reliance on debt funding involves interest expenses that push up the cost of production. Since interest expenses can rise at compounding rates, the impact on the overall cost structure becomes larger over time. These effects on inflation may help to explain persistent inflation throughout the recent crisis despite the significant drop in aggregate demand and broad measures of money.

The cost-push inflation of an earlier era may be gone, but the phenomena may still be with us today. The dismissal of private debt and interest expenses from macro models may be the reason the issue of cost-push inflation was “simply dismissed.”

In the wake of the crisis the Too Big To Fail problem has grown across the rich countries. When something happensalways and everywhere we should start looking for underlying laws. We're not at "always and everywhere" here but it's getting close: Time to theorize.

I don't think political influence from big banks is a major reason for the recent rise in bank size. Political influence is a constant, like gravity, so the question is what changed after 2008. Why the rise in bank concentration just as economists, policymakers, and politicians became more worried about bank concentration?

It sounds to me like an interaction between hyperbolic discounting (impulsivity, short term impatience in the government sector) and time inconsistency (depositors know the regulator will cave later so depositors put more money in TBTF banks today, making it even more tempting for the regulator to cave).

Woj’s Thoughts - Jones goes on to make the case for banning acquisitions by the biggest banks. I left the following comment on his blog:

While I agree that "hyperbolic discounting by bank regulators is a big problem", I wonder whether banning acquisitions would solve the problem. Looking at the most recent crisis, Bank of America, Wells Fargo and JP Morgan were practically begged by regulators to acquire other large banks presumably because no better alternative existed. Had those mergers been prevented, what actions would have been taken? Speed bankruptcy is an option, but likely wasn't on the table. It seems plausible that the government and Fed would have bailed out those failed banks more explicitly.

One of the other channels, that I think may be a greater issue, is the subsidies inherent in an implicit government backing for SIFIs. My reading suggests these institutions are able to finance their operations at rates 50-100 bps below other financial institutions. This cost advantage could eliminate smaller institutions regardless of banning acquisitions.

All this gets me back to the idea that the path towards deficit reduction in this hopelessly out of paradigm region keep coming back to the unmentionable PSI/bond tax. Seems to me we are relentlessly approaching the point where further taxing a decimated population or cutting what remains of public services becomes a whole lot less attractive than taxing the bond holders. And the process of getting to that point, as in the case of Greece, works to cause all to agree there’s no alternative. With the far more attractive alternative of proactive increases in deficits that would restore output and employment not even making it into polite discussion, I see the walls closing in around the bond holders, along with the argument over whether the ECB writes down it’s positions back on page 1. And just the mention of PSI in polite company throws a massive wrench (spanner) into the gears. For example, if bonds go to a discount, they’ll look towards ECB supported buy backs to reduce debt, again, Greek like. And if prices don’t fall sufficiently, they’ll talk about a forced restructure of one kind or another, all the while arguing about what constitutes default, etc.

The caveats can change the numbers, but seems will just make matters worse.

Woj’s Thoughts - Mosler has been one of the few voices that predicted this outcome for the Euro zone from the beginning. His thoughts on the forthcoming strength of the euro have certainly made me reconsider my views. I continue to worry about the political aspect within Europe and whether the people will continue to accept depression dynamics to remain in the Euro zone.

"In practice, of course, the purists were unable to deliver, and the new tricks involve the 'modern macroeconomists' in ad hoc assumptions of their own that are at least as objectionable as the Keynesian macroeconomic generalizations that [Michael] Wickens objected to. We have already encountered one example, the 'Gorman preferences' needed to make the representative agent at least minimally plausible... Two others are equally incredible. The first is the 'no-bankruptcies' assumption in Walrasian models and the related 'No Ponzi' conditon that is imposed on D[ynamic] S[tochastic] G[eneral] E[quilibrium] models. This eliminates the possibility of default, and hence the fear of default (since these are agents with rational expectations, who know the correct model, and hence know that there is no possibility of default), and hence the need for money, since if your promise to pay is 'as good as gold', it would be pointless for me to demand gold (or any other form of money) from you. Money would be at most a unit of account, but never a store of value. The second is the unobtrusive postulate of 'complete financial markets', smuggled into Michael Woodford's Interest and Prices(Woodford 2003, p. 64), which means that all possible future states of the world are known, probabilistically, and can be insured against: this eliminates uncertainty, and hence the need for finance..." -- J. E. King, The Microfoundations Delusion: Metaphor and Dogma in the History of Macroeconomics (2012: p. 228)

This quote is the lead in a recent post by Robert Vienneau putting forth the question, “Can General Equilibrium Theory find a role for money?” During my first semester in a PhD Economics program, application of the ‘No Ponzi’ condition appeared almost universal in macroeconomic models. At points I tried to raise the question of how removing this condition would impact results from the various models. Although a sufficient answer, at least for me, was not forthcoming, it appeared as though that condition was necessary to ensure a general equilibrium existed.

As for the inclusion of ‘complete financial markets’, I am not yet familiar with Woodford’s book, mentioned above. Having worked in financial markets for a few years, the notion of probabilistic uncertainty is not only false but completely misses an important aspect of investing. The purpose of holding various levels of cash over time is specifically because future states and their probabilities are unknown.

On the whole, general equilibrium models appear to remain consistent with the classical view ofcommodity trade, C-M-C' (a commodity is sold for money, which buys another, different commodity with an equal or higher value). Meanwhile two other views, put forth to account for a financial sector by Marx, have been largely ignored:

1) M-C-M' (money is used to buy a commodity which is resold to obtain a larger sum of money)

2) M-M' (a sum of money is lent out at interest to obtain more money, or, one currency or financial claim is traded for another. "Money begets money.")

Based on my initial exposure to advanced macroeconomics, it appears true that “money would be at most a unit of account, but never a store of value.”

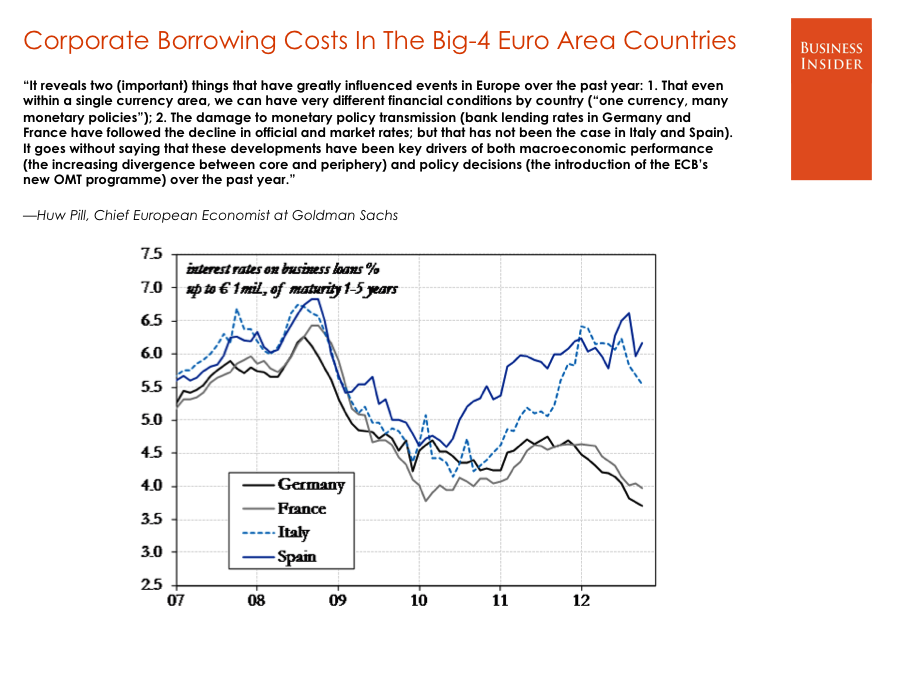

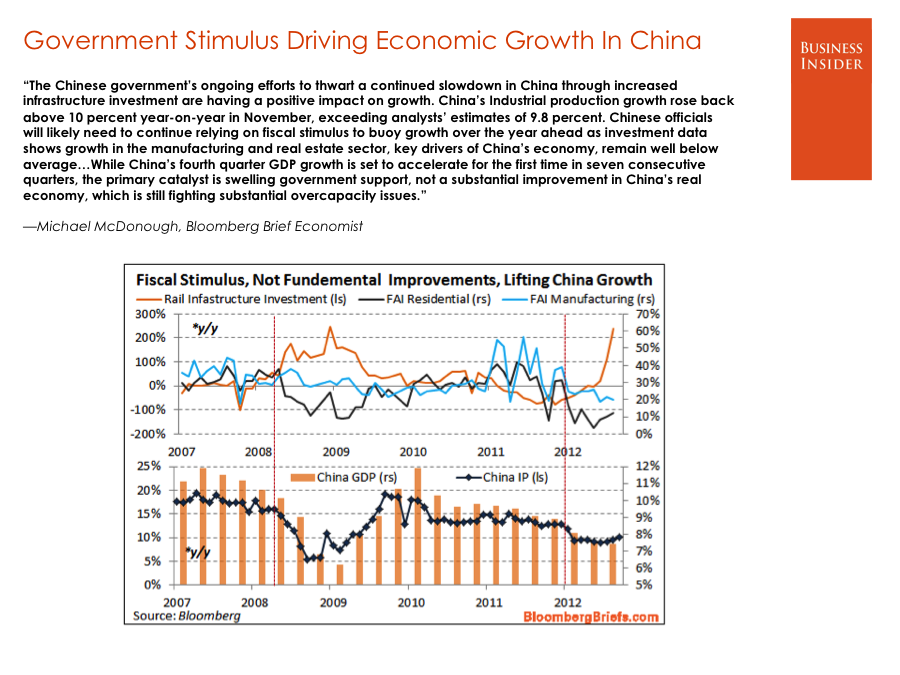

Business Insider has put together a fantastic list of Wall Street’s 75 Most Important Charts of 2012 (h/t Pragmatic Capitalism). The entire list is worth looking through and sure to spark numerous insights. Many of the charts need no further comment, so I’ll just offer my top few here:

Responding to a debate between Krugman and Steve Williamson on the current state of macroeconomics, Noah Smith asks, Macro, what have you done for me lately? The entire post is definitely worth reading, including the updates and comments. With apologies, I have copied several paragraphs here:

So if collegiality and similarity of technique are measures of a field's health, then macro is doing quite well. But I feel like there's a larger question: What has macro done for the human race in the last 40 years? How are we better off as a result of all this macro research effort?

…

So macro has not yet discovered what causes recessions, nor come anywhere close to reaching a consensus on how (or even if) we should fight them.

Given this state of affairs, can we conclude that the state of macro is good? Is a field successful as long as its members aren't divided into warring camps? Or should we require a science to give us actual answers? And if we conclude that a science isn't giving us actual answers, what do we, the people outside the field, do? Do we demand that the people currently working in the field start producing results pronto, threatening to replace them with people who are currently relegated to the fringe? Do we keep supporting the field with money and acclaim, in the hope that we're currently only in an interim stage, and that real answers will emerge soon enough? Do we simply conclude that the field isn't as fruitful an area of inquiry as we thought, and quietly defund it?

And who do we call in to evaluate the health of a science? If we only rely on insiders to evaluate their own field, we are certain to run afoul of vested interest (If someone asked you "How valuable is the work you do", what would you say?). But outsiders often lack the relevant expertise to judge someone else's field.

It's a thorny problem. And (warning: ominous, vague brooding ahead!) it seems to be cropping up in a number of fields these days, from string theory in physics to "critical theory" in literature departments. Are we hitting the limits of Big Science? Dum dum DUMMMM...But no, this question leads us too far afield...

In general my views on the matter are well represented by Smith. My early frustrations with economics were largely because I thought pursuits within macro had gone far afield from trying to understand business cycles in a modern economy. Since that time, I have been inspired by a group of competing theories that incorporate money and the financial system into macroeconomic models. My hope and belief is that these currently heterodox methods will, in time, be able to largely explain what causes recessions and how to fight them. If, and when, that occurs, the state of macro will be good. Also see: The New Classical Revolution: Technical or Ideological? by Simon Wren-Lewis

A steady state is characterized by the economy having a constant rate of growth. I here select a number of expositions of analyses of steady state I have made on this blog:

The Harrod-Domarmodel of warranted and natural rates of growth.

Karl Marx's volume 2model of simple and expanded reproduction.

Anyhow, most of the mainstream has been working under some form of the “liquidity preference” theory or “liquidity trap” theory to explain why rates have remained low in the USA. This was the thinking that economic agents were choosing to just sit on the excess liquidity provided via the government and the Fed. It sounds right in theory, but it’s wrong in reality.

First, the government doesn’t increase the money supply through government spending (already confused? Seehere). It redistributes inside money (bank money) and adds a net financial asset in the form of a government bond. This improves private balance sheets and is particularly useful during a balance sheet recession, but it’s not the equivalent of firing dollar bills out into the economy (though it does increase the velocity of spending as the government becomes the “spender of last resort” when an economy is stagnant for whatever reason). Second, when the Fed implements QE they swap reserves for bonds. No change in net financial assets. And since banks don’t lend reserves there is no firm transmission mechanism through which this policy can impact the money supply. In short, fiscal policy hasn’t been the equivalent of increasing the money supply in the traditional “money printing” sense that most believe and QE has most certainly not resulted in an increase in the money supply because the primary transmission mechanism is busted (the lending channel).

Woj’s Thoughts - Paul Krugman has recently changed his views to acknowledge that bond vigilantes are not an issue for the US. While he should be commended for taking this step away from the typical mainstream position (which he held prior to the crisis), his views remain tied to “liquidity trap” models. Although these models will, in some instances, come to correct conclusions, that may be due to chance rather than logic.

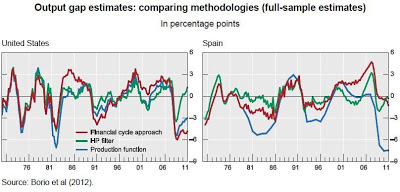

Claudio Borio from the BIS has written a widely citedpaper.

…

The new output gap measure would include financial variables. He correctly notes that output gap measures take into consideration only inflation, when ascertaining whether the economy is above the potential or not, and that "it is quite possible for inflation to remain stable while output is on an unsustainable path" [and you can have inflation without being at full employment too, I would add]. His measure of the output gap would include information about asset price inflation too (property prices and measures of credit booms) and is shown for the US and Spain as the red line below.

…

I have several problems with these views, even if there are some good things, beyond good intentions, in Borio's paper. In fact, I think that there is significant evidence for the notion that potential output varies with demand expansion (Kaldor-Verdoorn Law), so that if a revision of the way potential output is measured it would be in the opposite direction.

Woj’s Thoughts - An accurate measure of the output gap would be very beneficial in demonstrating the periods when macroeconomic smoothing is necessary. Unfortunately trying to create that measure is no easy task and previous efforts have likely led to false policy prescriptions. Given the substantial variation based on methodology, as shown above, the current benefit of such measures to policy making seems limited.

Mr Abe plans to empower an economic council to “spearhead” a shift in fiscal and monetary strategy, eviscerating the central bank’s independence.

The council is to set a 3pc growth target for nominal GDP, embracing a theory pushed by a small band of “market monetarists” around the world. “This is a big deal. There has been no nominal GDP growth in Japan for 15 years,” said Mr Christensen.

Since my extreme skepticism towards NGDP targeting has been previously outlined on numerous occasions (here, here, and here for example), I won’t rehash those arguments now. With Monetarists focusing attention on the possible NGDP target, I want to consider a different view from Tim Duy (h/t Economist’s View):

The loss of the Bank of Japan's independence to force the direct monetization of deficit spending is the real story.

…

Bottom Line: Inflation targeting is not the whole story in Japanese monetary policy. It is a facet of a much greater story. A story of a modern central bank stripped of its independence. Of a modern central bank forced to explicitly monetize deficit spending. Ultimately, it is the story of the end game of the permanent zero interest rate policy.

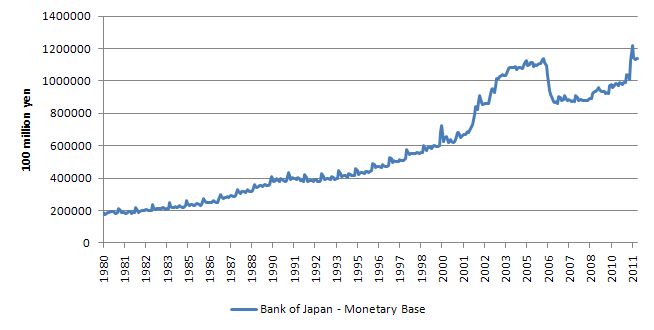

Over the past couple decades, the Bank of Japan (BOJ) has been implicitly monetizing deficit spending through its own QE programs (graph courtesy of billy blog) : The question then becomes, is making these actions explicit really a game changer? The BOJ has been unsuccessful in trying to stimulate private credit markets (and thereby growth and inflation) for the better part of two decades. Zero-interest rates, a rapidly expanding balance sheet, and unconventional asset purchases have all failed to do the trick. If removing the central bank’s independence simply results in more of the same, with larger quantities and new targets, then I fail to see why the outcome will be any different.

From my perspective, the loss of independence only really matters to the degree it permits a looser fiscal stance. As modern money proponents have frequently shown, currency issuers such as Japan need not worry about bond vigilantes and the BOJ can set interest rates indefinitely at whatever level it chooses. If Abe wishes to increase inflation and nominal GDP, there is little doubt he could do so by expanding the government’s budget deficit. The economic significance of Prime Minister Abe’s appointment therefore lies more with his stance on fiscal policy, not monetary policy.

Since Abe previously held the Prime Minister position from September 2006 through September 2007, we have the good fortune of reviewing his fiscal policies during that time. According to Bloomberg, following that election:

“The government [was] aiming to find as much as 90 percent of the money it needs to achieve a primary balance from spending cuts, with the rest coming from other measures such as higher taxes.”

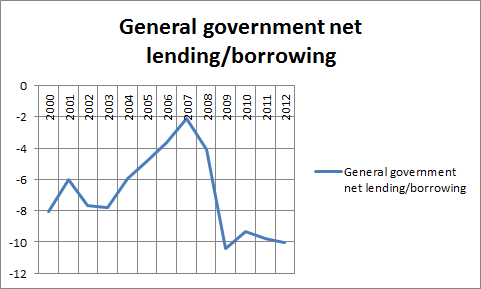

As the following chart shows, Abe’s previous leadership entailed the smallest budget deficit during the past 12 years, by a wide margin (Source: IMF): Although Abe may be willing to accept short-term fiscal expansion this time around, his medium and long term views still seem focused on reducing public debt.

After 20-plus years of shifting debt from the private to public sector, the private sector is once again in position to drive growth and inflation higher. The ongoing struggle for policy makers is how to revive private demand for credit that has been lacking for so long (chart courtesy of The Economist):

Considering this background, the most likely outcome from Abe’s election is brief fiscal stimulus that is reversed once the economy begins to recover. As demographics continue to work against the Japanese economy, encouraging private credit demand will become even tougher. Whether or not the BOJ officially loses its independence, explicitly monetizes the budget deficit or targets NGDP, it will be of little consequence for medium-run inflation and economic growth if fiscal policy remains effectively the same.

Five months ago, when word was spreading that the Fed might cut the interest rate on excess reserves (IOER), I argued that making IOER negative equates to raising taxes. Part of the misguided notion that such a policy will be stimulative is due to the incorrect belief that banks are choosing to hold excess reserves on the central bank balance sheet instead of lending them out. Presenting work from the NY Fed itself, I tried to debunk that myth by explaining why cash “parked” at the Fed will remain there. Discussion of this policy has been revisited in Europe over the past couple months and its enactment remains a major risk to the global economy.

For those readers unconvinced by previous discussion or simply interested in the topic, Frances Coppola recently provided an in-depth look at the strange world of negative interest rates. Trying not to dissuade readers from viewing the entire post, here is a small sample (emphasis mine):

It's worth remembering, too, that reserves are created by the central bank, not by commercial banks, and that commercial banks have no power to reduce the total amount of reserves in the system. That can only be done by the central bank. So if commercial banks were discouraged by negative interest rates from holding excess reserves, but there were still excess reserves in the system, banks would look for ways of passing on those excess reserves to other banks. Excess reserves would become something of a hot potato, with no bank wanting to be caught with excess reserves at the end of the day. I suppose that might improve the velocity of money, but I could see it leading to all manner of stupid investments.

…

But consider what would happen if an economy experiencing deflationary pressure introduced negative interest rates. The squeeze on the margins of already-damaged banks would inevitably lead to higher rates to borrowers and reduced lending volumes. This is monetary tightening, not easing, and the effect would be contractionary. It would make the recession worse.

…

Like negative rates on reserves, negative policy rates could actually have a toxic effect on the real economy. Across Europe, including the UK, many loan rates - especially mortgages and business loans - are tied to the policy rate. So if the policy rate were cut to below zero, lenders would find their margins squeezed on existing lending: they could even find themselves receiving negative returns on these loans. Realistically they cannot cut their deposit rates to savers to below zero (savers would stuff mattresses instead), so their only option is to RAISE lending rates to new borrowers, widening credit spreads. Exactly the same effect as negative interest rates on reserves, in fact - and the same effect as QE.

…

So cutting policy rates to below zero would be as counter-productive as cutting interest rates on reserves. And it would be unpopular. I can't imagine any electorate, wounded as they are by the behaviour of banks, tamely accepting bank funding being subsidised while interest rates to new borrowers soared and the economy crashed.

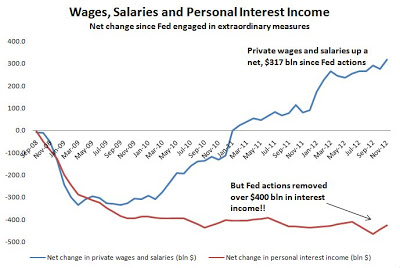

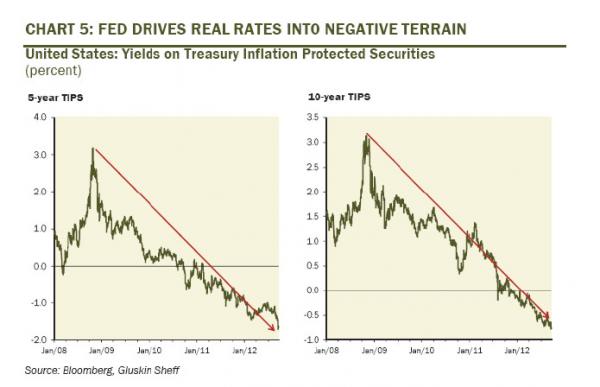

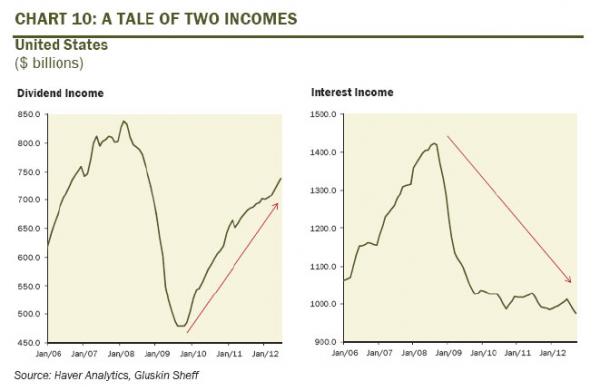

Earlier today, I presented several charts from David Rosenberg’s 2013 Investment Outlook. One of those charts depicted the steep drop in interest income earned by the private sector since the financial crisis began. A primary driver behind that decline has been the Federal Reserve, lowering interest rates and then swapping low-paying reserves for higher yielding securities (Treasuries and Agency-MBS). Countering the mainstream view that more monetary stimulus is needed, Mike Norman asks, “What stimulus?? Fed actions completely offset wage and salary gains!

Case in point, the $80 bln in profits that the Fed earned and turned over to the Treasury last year, was from income earned on the assets it bought. That was income that would have been earned by the private sector if it still had those bonds and securities.

So while the net change in wages and salaries since 2008 has been an increase of $317 bln, personal interest income dropped by $425 bln. That's not a stimulus by any means. It's mind boggling that the mainstream economics community and the Fed itself, doesn't understand this when they incessantly call for more "stimulus."

Unlike the Market Monetarists and New Keynesians, who have been constantly begging for the Fed to “do more”, this is why myself and many others have been wishing the Fed would do far less. While stimulating present paper profits in the stock market through negative real yields, the Fed’s actions are actually removing income from the private sector. Instead of stimulating the economy, ZIRP and QE help ensure the economic recovery remains weak. These actions will only further the reliance on credit and exacerbate downturns going forward.

One of the best resources for investment advice and economic projections over the past several years has been David Rosenberg. Courtesy of Zero Hedge, here is part of his outlook for 2013:

The Fed has also completely altered the relationship between stocks and bonds by nurturing an environment of ever deeper negative real interest rates. Therein lies the rub. The economy and earnings are weak, and getting weaker, but the Interest rate used to discount the future earnings stream keeps getting more and more negative, and that lowers the corporate cost of capital and in turn raises the present value of expected future profits. It's that simple.

...

Beneath the veneer, there are opportunities. I accept the view that central bankers are your best friend if you are uber-bullish on risk assets, especially since the Fed has basically come right out and said that it is targeting stock prices. This limits the downside, to be sure, but as we have seen for the past five weeks, the earnings landscape will cap the upside. I also think that we have to take into consideration why the central banks are behaving the way they are, and that is the inherent 'fat tail' risks associated with deleveraging cycles that typically follow a global financial collapse. The next phase, despite all efforts to kick the can down the road, is deleveraging among sovereign governments, primarily in half the world's GDP called Europe and the U.S. Understanding political risk in this environment is critical.

...

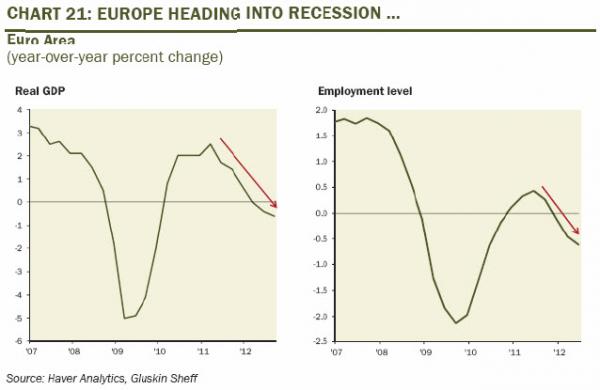

With regard to global events, we continue to monitor the European situation closely. Euro zone finance ministers have given Greece an additional two-year lifeline and the Greek parliament just passed another round of severe austerity measures, which I think will only serve to make matters worse there from an economic standpoint, but I doubt that the creditors are going to let Greece go just yet. So this never-ending saga remains a source of ongoing uncertainty, but at the same time. Is a key reason why the Fed and the Bank of Canada will continue to keep short-term interest rates near the floor, and all that means is to build even more conviction over income equity and corporate bond themes.

...

As for something new, after a rather significant slowdown in China for much of this year that put the commodity complex in the penalty box for a period of time, we are seeing some early signs of visible improvement in the recent economic data out of China and this actually has happened even in advance of any significant monetary and fiscal stimulus. And while the Chinese stock market has been a laggard, if there is one country that does have the room to stimulate, it is China (make no mistake, however, China's economic backdrop is still quite tenuous, especially as it pertains to the corporate sector - excessive inventories, stagnant profits, rising costs and lingering excess capacity are all challenges to overcome).

Keep in mind that much of this slowing in China was a lagged response to prior policy tightening measures to curb heightened inflationary pressures - pressures that have since subsided sharply with the consumer inflation rate down to 2% (near a three-year low) from the 6.5% peak in the summer of 2011 and producer prices are deflating outright. What is providing a big assist to this sudden reversal of fortune in China is a re-acceleration in bank lending as a resumption of credit growth and bond issuance has allowed previously- announced infrastructure projects out of Beijing (railways in particular) to get incubated.

The nascent economic turnaround we are seeing in China, if sustained, is Positive news for the commodity complex and in turn resource-sensitive currencies like the Canadian dollar, which I'm happy to report has hung in extremely well this year even in the face of all the global economic and financial crosscurrents. Just consider that the low for the year for the loonie was 96 cents - you have to go back to 1976 to see the last time intra-year lows happened at such a high level.

...

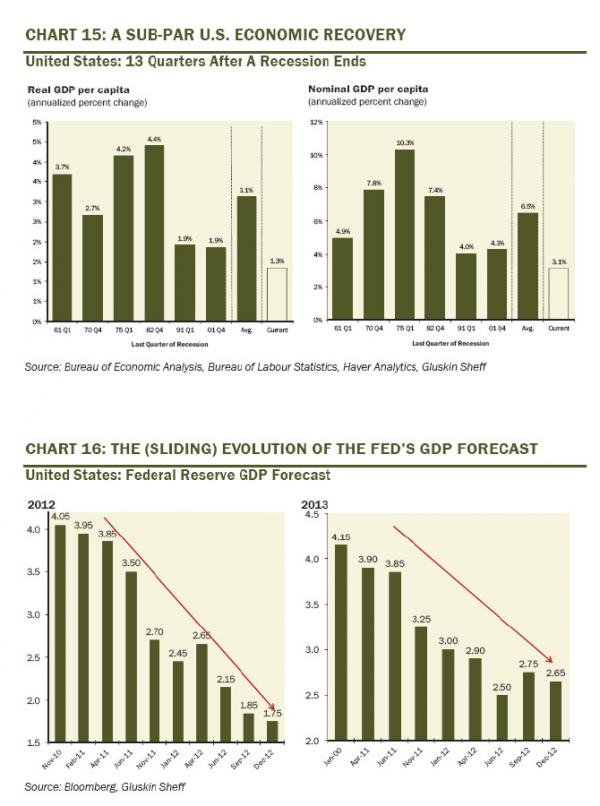

To reiterate, our primary strategy theme has been and remains S.I.R.P. - Safety and Income at a Reasonable Price - because yield works in a deleveraging deflationary cycle.Not only is there substantial excess capacity in the global economy, primarily in the U.S. where the "output gap" is close to 6%, but the more crucial story is the length of time it will take to absorb the excess capacity. It could easily take five years or longer, depending of course on how far down potential GDP growth goes in the intermediate term given reduced labour mobility, lack of capital deepening and higher future tax rates. This is important because what it means is that disinflationary, even deflationary, pressures will be dominant over the next several years. Moreover, with the median age of the boomer population turning 56 this year, there is very strong demographic demand for income. Within the equity market, this implies a focus on squeezing as much income out of the portfolio as possible so a reliance on reliable dividend yield and dividend growth makes perfect sense.

...

Gold is also a hedge against financial instability and when the world is awash with over $200 trillion of household, corporate and government liabilities, deflation works against debt servicing capabilities and calls into question the integrity of the global financial system. This is why gold has so much allure today. It is a reflection of investor concern over the monetary stability, and Ben Bernanke and other central bankers only have to step on the printing presses whereas gold miners have to drill over two miles into the ground (gold production is lower today than it was a decade ago - hardly the same can be said for fiat currency). Moreover, gold makes up a mere 0.05% share of global household net worth, and therefore, small incremental allocations into bullion or gold-type investments can exert a dramatic impact. Gold cannot be printed by central banks and is a monetary metal that is no government's liability. It is malleable and its supply curve is inelastic over the intermediate term. And central banks, who were selling during the higher interest rate times of the 1980s and 1990s, are now reallocating their FX reserves towards gold, especially in Asia. With the gold mining stocks trading at near record-low valuations relative to the underlying commodity and the group is so out of favour right now, that anyone with a hint of a contrarian instinct may want to consider building some exposure - as we have begun to do.

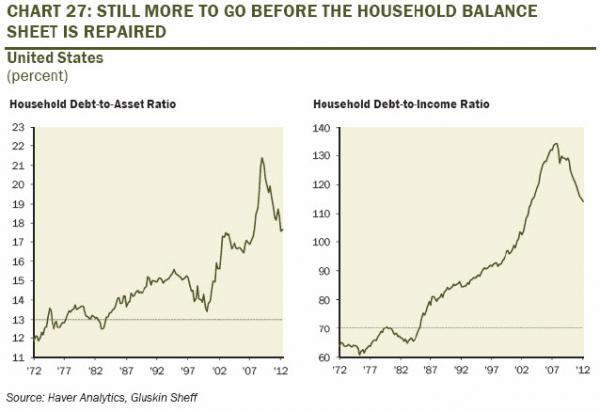

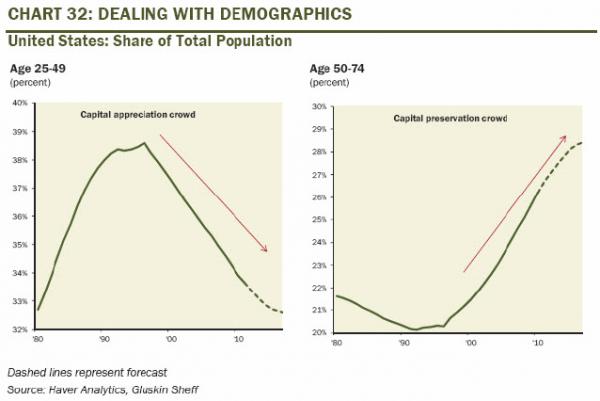

The Fed’s recent actions imply that it will permit inflation to temporarily rise above 2% in the hopes of reducing unemployment and spurring growth at a faster pace. While that occurrence remains to be seen, there is potential for even deeper negative real yields over the coming year to boost stocks further. However, as I’ve been arguing for many months, future earnings growth will likely be much weaker than expected and may turn negative. Last year I offered my own predictions for 2012. In the next couple weeks, I hope to discuss those successes and failures, while also putting forth new predictions for 2013. In the meantime, here are few charts from Rosenberg’s outlook that caught my eye: