When discussing the price stability mandate, most commenters typically refer to an inflation target of 2% based on the FOMC’s preferred measure of core PCE inflation (See the report for more on previous measures and Bernanke’s argument for using a measure of core inflation). The preferred measure is clearly set forth by the FOMC, but what about the 2% target? Widely regarded as being explicit, actual Fed statements regarding a target suggest otherwise. In 2010, the Federal Reserve Bank of St. Louis published a short essay asking, Is the Fed’s Definition of Price Stability Evolving? The essay points out that:

Relatively few Federal Reserve officials have publicly indicated what level of the inflation rate corresponds to price stability.Noting a few exceptions, the essay highlights comments by former Fed officials, William Poole and Alan Greenspan, suggesting a target for core inflation closer to 1%. One might dismiss these comments as irrelevant today so instead, consider those made by current Chairman Bernanke (my emphasis):

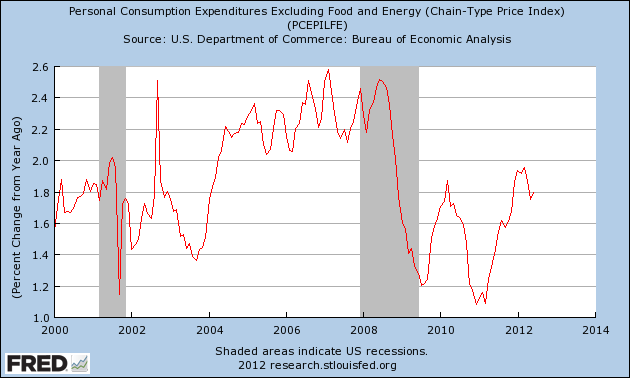

It is not clear whether Chairman Bernanke, or any other current member of the FOMC, accepts either of these definitions of price stability. However, before he replaced Greenspan in January 2006, then Fed Governor Bernanke publicly stated in 2005 that his “comfort zone” for core PCE inflation was between 1 and 2 percent. More recently, Bernanke stated that the FOMC’s “mandate-consistent inflation rate” is generally judged to be “about 2 percent or a bit below.”Unless Bernanke has made more recent statements revising this judgment, 2% is clearly not a target but rather the ceiling of his target range. Having clarified the Fed’s own measurement of success, here is graph showing the actual results of core PCE since 2000:

Inflation falls noticeably below Bernanke’s range in late 2009 and then again in late 2010. However, take a close look at the inflation readings during the first half of 2012. Core PCE has averaged 1.9% and held within a range just below 2%. One can argue about the correct measure or target the Fed should use, but by the Fed’s own standard of price stability, current policy is proving very successful. If these conditions persist, those hoping for further monetary easing may be disappointed.