This discussion of asset bubbles comes on the heels of St. Louis Federal Reserve Governor Jeremy Stein’s speech that suggested the Fed was becoming increasingly concerned about bubbles, not inflation. According to a recent Bloomberg article, apparently Fed Chairman Bernanke was not onboard with the supposed shift (h/t Tim Duy):

Federal Reserve Chairman Ben S. Bernanke minimized concerns that the central bank’s easy monetary policy has spawned economically-risky asset bubbles in comments at a meeting with dealers and investors this month, according to three people with knowledge of the discussions.

Do Bernanke’s comments imply the change Stein alluded to is not really happening? Not necessarily. To understand why, one must consider the goals assigned to Bernanke or any Fed Chairman for that matter. The following is from Chapter 2 of the Federal Reserve System’s own publication, Purposes & Functions:

The goals of monetary policy are spelled out in the Federal Reserve Act, which specifies that the Board of Governors and the Federal Open Market Committee should seek “to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

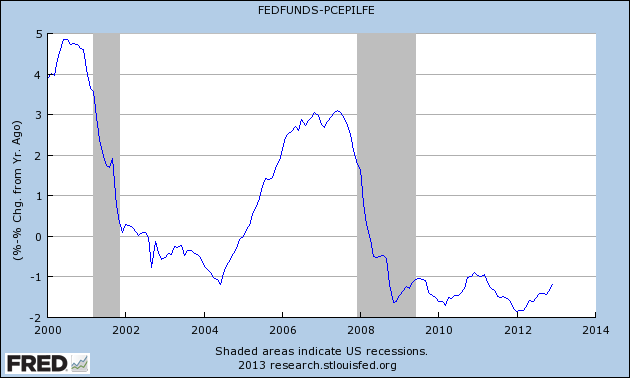

Although no explicit mention of preventing asset bubbles is made, the goal of stable prices leaves the door open for such an interpretation. Before addressing the Fed’s own interpretation of stable prices, its worth discussing the specific types of assets that are seemingly most prone to bubbles. The three major categories are commodities (e.g. oil, copper, sugar), financial assets (e.g. stocks and bonds), and housing. During the past decade real interest rates have actually been negative more often than not (Real Interest Rate = Effective Fed Funds rate - core PCE):

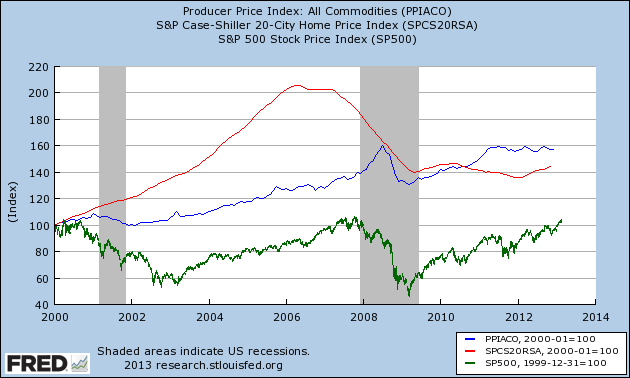

Unsurprisingly the past decade has also witnessed asset bubbles in commodities, stocks and housing:

Prices of these assets have clearly been anything but stable. So has the Fed failed in that aspect of its mandate? The answer is a resounding “NO.”

To remedy the cognitive dissonance readers may be experiencing, consider how the aforementioned real assets affect the FOMC’s preferred inflation measure, core Personal Consumption Expenditures (PCE). Financial assets are noteworthy in their distinct omission from the type of products making up PCE. Commodities are included in the general price measure, however core PCE is calculated by excluding a couple of the more volatile commodity components: food and energy. Housing is actually included in core PCE but is calculated using the space rent of nonfarm owner-occupied homes, not actual house prices. Focusing on core PCE thereby removes any direct concern with asset bubbles.

Bernanke has already announced his plans to step down as Fed Chairman early next year (2014). Given the Fed’s stated mandate and preferred measure of prices, it is no wonder that Bernanke is unconcerned with asset bubbles. The goals of his chair are to maximize employment and maintain stable prices. Since the types of assets prone to bubbling are not included in core PCE and appear relatively uncorrelated with that measure, to the degree that bubbles can benefit employment in the short run, they may actually be desirable.*

These institutional incentives of a Fed Chairman are unfortunately at odds with the country’s longer term economic goals. Asset bubbles created by excessive lending and/or negative real interest rates are always followed by busts. These busts are simply the recognition of malinvestment that already took place during the boom. If the booms are financed with significant leverage, the resulting deleveraging may lead to a debt deflationary spiral. Whether or not that’s the case, though it usually is, malinvestment suppresses both employment and economic growth over time.

One can argue over whether Bernanke’s views on the effectiveness of monetary policy are correct or not, but his decision to ignore asset bubbles is perfectly rational given the circumstances. Shifting the Fed’s focus from inflation to bubbles will therefore require changing the institutional incentives.

*The three major asset categories mentioned above presumably will have very different effects on employment. Among the three, commodity bubbles are least desirable from an employment perspective. Higher commodity prices generally hurt consumer spending, which may lead to a temporary decline in employment. Housing bubbles are the most desirable in these terms since the increased demand can generate a temporary employment boom in construction and housing-related services.

When the cb takes its chief job to be price stability, then it can ignore other equally or even more significant aspects of the economy. In fact, in targeting inflation, monetary policy based on the Phillips curve, NAIRU and Taylor rules uses employment as a tool by expanding and contracting the buffer stock of unemployed.

ReplyDeleteAs far as asset bubbles go, the cost of capital is determined by the interest rate and borrowing is not only for productive investment, as the theory assumes, but also speculation in financial capital. This creates speculative bubbles not only in capital markets but also in commodity markets, since commodities are now considered to be asset classes in the portfolio mix. Ignoring this is inane.

Great points Tom. The use of unemployment to limit inflation suggests the Fed had internally developed a hierarchy among the given mandates, which I didn't fully address here. I suspect the Fed may have done so in the hopes of building credibility on the inflation front (since credibility on the employment front would have been significantly more challenging).

DeleteNow that the Fed is trying to target both employment and inflation, I suspect it may lose much of the credibility it had over the coming years. Unfortunately I remain pessimistic about Fed actions actually recognizing the potential of creating asset bubbles.

So in the monetarist world "price stability" (shouldn't that be every increasing price stability) is targeting a metric that excludes key parameters and that's fine because despite all the evidence of the last ten years bubbles don't really matter or don't exist or can't be predicted or you never know when your in one or.. *gonemad*

ReplyDeleteI guess if you think private banks can't create money you say stuff like this http://www.washingtonpost.com/wp-dyn/content/article/2005/10/26/AR2005102602255.html

Haha, that's a great find. Your comment is definitely true about monetarism. As for Bernanke, I'm willing to concede he may just be playing the political game (which Greenspan did very well). Had he spoken out about housing he may not have become Fed Chairman. We'll see what revelations he offers after his term ends.

DeleteThere's a very interesting article on Vox related to this subject. Output gaps of 0% are correlated with nominal credit growth higher than nominal GDP growth (the actual number is close to 7%). In other words, credit bubbles allow for output gap smoothing but create long-term risks since (private) credit grows faster than income.

ReplyDeleteA central bank targeting a zero output gap (which should be consistent with long-term price stability) is actually contributing to financial instability, especially if credit growth is due to investments in secondary markets (housing, stocks).

http://www.voxeu.org/article/how-central-banks-contributed-financial-crisis

Thanks for the link. Only took a quick glance but some of the charts remind me of Steve Keen's work. After this recent crisis it just seems crazy to return to a world that ignores the growth of private debt.

Deletekuşadası

ReplyDeletemilas

çeşme

bağcılar

adana

DORLR