This data is consistent with rising income and wealth inequality but requires reversing Stiglitz’s “underconsumption” hypothesis. Trying to maintain relative consumption levels, many households clearly chose to rely on previous savings or new debt as a means of temporarily boosting consumption. As inequality continues to rise, wealthy households are now electing to retain more of their savings within corporations. It doesn’t take a leap of faith to suggest this combination of factors depresses aggregate demand.Still unconvinced, Krugman has been searching for further data (see here and here) that would lead him to believe inequality really is holding back the recovery.

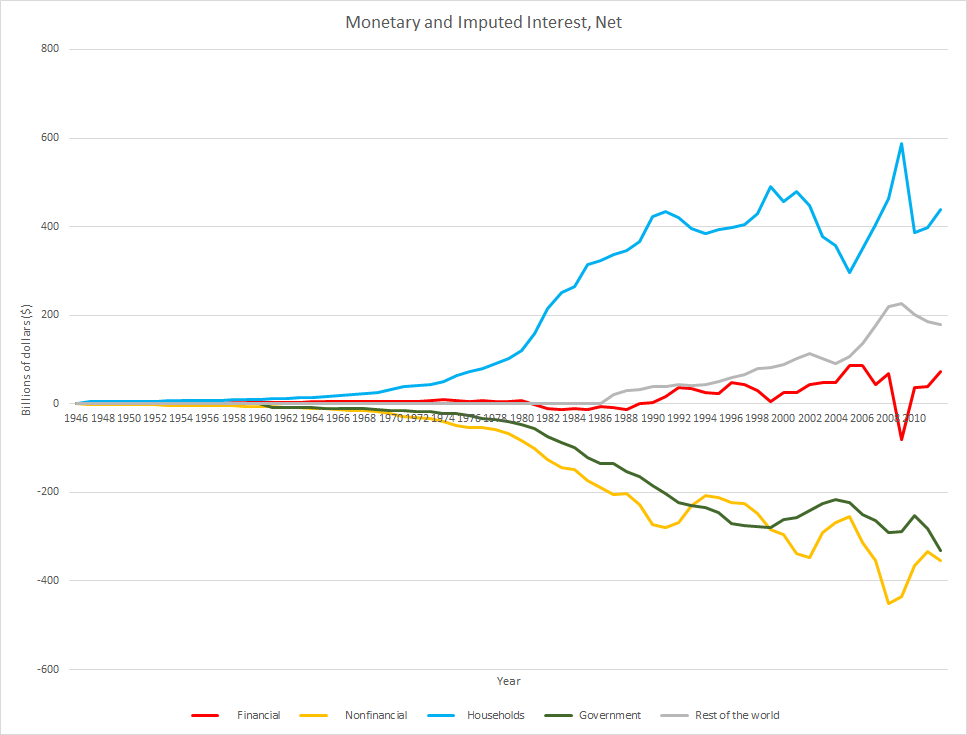

Hoping to aid Krugman in his quest and expand upon my “overconsumption” theory, let me respond to a critique of the previous post. Over at Mike Norman Economics, a commenter (Ryan Harris) kindly noted the obvious omission of interest income and sectoral balances. After sorting through interactive data from the Bureau of Economic Analysis, here are net amounts of monetary and imputed interest by sector [positive (negative) total implies sector receives (pays) net interest]:

Unsurprising to those familiar with sectoral balance analysis, households net interest position took a sharp turn upwards when federal budget deficits began expanding more rapidly in 1980:

Around the same time, household interest income received a significant boost from the nonfinancial business sector. The pronounced decline in the net interest position of that sector aligns closely with high interest rates of the preceding period and a massive expansion of nonfinancial corporate debt shortly afterwards:

Since then the rise and fall of nonfinancial interest payments (and outstanding debt) has tracked the business cycle, with the overall trend remaining steadily lower (higher net payments and outstanding debt). Although these transfers support household income, they also increase income inequality since wealthy households hold a vast majority of financial assets (including corporate debt).

Turning to the foreign (rest of the world) sector, the U.S. current account (trade) balance fell heavily in the 1990’s:

Foreign countries began amassing large quantities of U.S. financial assets (primarily Treasuries) corresponding to the substantial trade deficits. The growth in net interest receipts arising from these holdings represents an ongoing leak in domestic aggregate demand.

With the beginning of a new millennium and the dot-com bubble, a hostile environment was created for the household net interest position. Federal budget surpluses, declining interest rates, rapidly expanding trade deficits, and increasing payments to the financial sector (for housing) led to a nearly 40% decline in household net interest receipts. Combined with increasing income inequality, many households drew upon savings and increased demand for new debt to maintain previous levels of consumption.

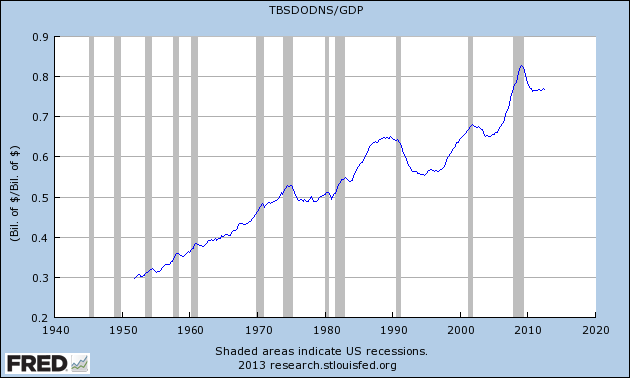

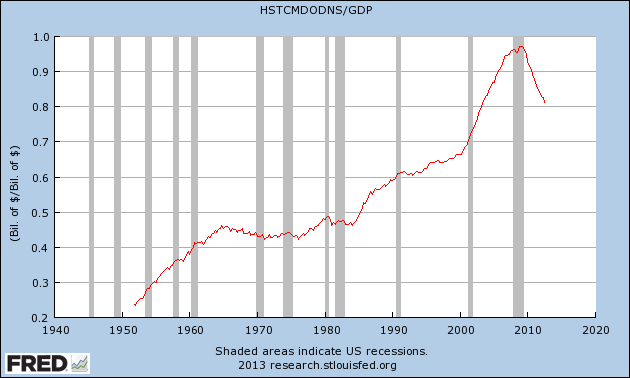

A side effect of the budget surpluses was a growing desire for safe financial assets separate from U.S. Treasuries. Securitization provided a means for new loans of varying risk to be converted into supposedly “super-safe” assets and transferred off of bank’s balance sheets. These factors encouraged banks to meet the surging demand for new loans coming from households (Chart: Household Debt-to-GDP):

The effects of these transactions can also be seen in the transfer of net interest payments from households, and later businesses, to the financial sector. Apart from adding to inequality, these transfers reduce aggregate demand since, as Michael Hudson notes in The Bubble and Beyond, “financial institutions tend to save all their income.” (2012: Kindle Locations 6814-6815)

Since the financial crisis ended, the trend towards higher net interest receipts by the financial sector and greater net interest payments by the nonfinancial corporate sector have returned. These transfers of income up the income/wealth ladder serve to exacerbate the weak demand stemming from two decades of stagnating household interest income. Unfortunately, and so far unsuccessfully, public policy (fiscal and monetary) remains dedicated to originating a new private debt led boom.

The changes in net interest payments/receipts over the past few decades highlight the growing income and wealth disparities present in our society. For many years households dug themselves deeper in debt to maintain relative consumption levels. The costs of excessively accumulating private debt have now been recognized, but the burden of interest payments suppressing aggregate demand will be felt for years to come.

Bibliography

Hudson, Michael (2012-10-04). THE BUBBLE AND BEYOND (Kindle Locations 6814-6815). ISLET. Kindle Edition.

Maybe in another post you could get your hands on time series data for the current account that is net of treasuries and then separately net of MBS later. I hear it mentioned a lot that the treasuries detract from the current account - but I don't ever hear the relative magnitudes...

ReplyDeleteAppreciate the suggestion. I'll see what I can dig up in the future...

DeleteI agree with the conclusion that interest payments suppress demand because of income inequality. However, this is not the case for Treasury bond interest payments under negative real rates. The owners of T-bonds -- presumably the top 5% -- are losing real wealth by holding them. This real wealth is effectively being transferred to taxpayers.

ReplyDeleteMy sense is that negative real rates primarily affect the real wealth of wealthy households. So far, these households have tried to escape the loss in wealth by selling Treasuries (to the Fed, non-wealthy households, foreigners) and buying risk assets. This works until risk assets stop performing and perhaps begin to fall in price. At that point, the top 5% will be exposed to the wealth transfer again, and would need to sell both Treasuries and risk assets in favor of a "safe real wealth" asset (T-bonds, as discussed, are not one).

The above dynamic is typical of Latin countries, where the source of inflation is the desire of the wealthy to protect their wealth from persistently negative real interest rates. It is their hedging activity (aka, capital flight) that sparks the inflation dynamic.

Definitely agree with you here. I purposefully tried to focus attention on household and nonfinancial corporate debt since government debt adds net financial assets and spending power to the economy. Do you have any good data on the percentage of Treasuries or other assets held by different income/wealth classes? I would have suspected Treasuries were a bit more spread out given their inclusion in the social security trust fund and many pension funds.

DeleteIn terms of negative real rates you highlight an important part of the portfolio rebalancing I see stemming from the Fed's action. I suspect the point at which the current pattern stops working may occur much sooner than many expect (next 12-18 months). At that point it will be interesting to see how policy makers respond.

I am confused about Net financial Assets and the "money supply." Government spending creates deposits and net financial assets in the non-government sector. So, I assume these new new financial assets, those deposits, are part of the money supply. Correct? Lending does does not create net financial assets because everything nets to zero. But I keep reading that commercial bank lending does add ( and some places it says most of) to the money supply unit the loan is paid off.

ReplyDeleteSo are both government spending and bank lending the money supply?

Let me try to respond to this line of thought first.

DeleteFirst of all, when discussing the "money supply' it's important to recognize that numerous different definitions exist and therefore have very different implications for macroeconomic variables. The most basic, and possibly frequent, definition is that the money supply is the monetary base, which includes central bank reserves and currency.

Using this terminology, it would be incorrect to say that commercial bank lending adds to the money supply. However, as recent debates in the econ blogosphere have outlined, there are many assets which are money-like (money-substitutes) and trade each day as if they were money. An example is commercial bank loans created ex nihilo. These loans generate a corresponding deposit in the banking system which can be used freely by anyone willing to accept that bank's loan. This new deposit adds to broader measures of the money supply and increases purchasing power, at least temporarily. When the loan is ultimately repaid, the broader money supply declines.

Further to my question above is this. The govt spends by marking up the recipient's bank's reserve account. Then the recipient's bank marks up the recipient's deposit account. So the bank's balance sheet's composition has changed -- more reserves (assets) and more deposits (liabilities). So, in that sense there is no new net financial assets. Banks are part of the non-governmental sector, so how does that square with govt spending creates net financial assets. Is it because the bank's reserves are offset with the deduction of reserves from the Treasuries account?

ReplyDeleteWhen the government spends reserves it increases the base money supply and when it receives taxes it reduces the base money supply. The increase in NFAs arises when the govt deficit spends. In those instances the govt spends reserves and then sell Treasuries to mop up an equivalent amount of reserves. Individuals/corporations receive new deposits in their account. The financial system marks the new deposits as liabilities and the new Treasuries as assets. To zero out the overall accounting, the govt marks the Treasuries as a liability.

DeleteIn the example above, the govt ends up with net new liabilities and the private sector receives new net financial assets (Treasuries).

Hopefully these explanations helped but if they weren't clear or didn't fully answer the question, let me know and I'll try again.

*The above example is my understanding of modern monetary operations, which I believe to be correct, but may contain errors.

Joshua - Thank you very much for your replies. i will study and think on tonight and let you know tomorrow if I have further questions or comments. John

DeleteJoshua: "When the government spends reserves it increase the base money supply..." But say the govt spends $100. The Fed removes $100 in reserves from the Treasury's reserve account and adds $100 in reserves to the recipient's bank's reserve account. So that nets to zero, doesn't it? So how is that an increase in base money?

DeleteAlso your comment "when gov't spends reserves it sells equvalent amount of Treasuries to mop up reserves." Is the "equivalent" actually the reserve spending above revenues collected. In other words, the deficit spending? John

John,

DeleteReserves held in the Treasury's account at the central bank are not counted as part of the money supply/monetary base. It may seem odd, but that's why govt spending adds to the money supply/monetary base.

Yes. The govt is only required to sell Treasuries equivalent to the amount of deficit spending (spending above revenues). This is a relic of the gold standard since the govt doesn't actually need to borrow reserves in order to spend. Prior to the crisis, however, the sale of Treasuries was a relatively efficient means for controlling the supply of reserves and therefore helping the Fed maintain its interest rate target. Now that the Fed is operating under a "Permanent Floor" with excess reserves, Treasury sales are basically just provision of safe assets to meet investor demand and provide a transfer of funds from the govt to the private sector.

Here is a quote from "Modern Central Bank Operations -- The General Principles" by Scott Fullwiler:

Delete"First, the national government’s account is a liability on the central bank’s balance sheet, which means spending necessarily credits reserve balances to reserve accounts of recipients’ banks, while taxation debits them."