The Myth Of The Money Multiplier by Barkley Rosser @ EconoSpeak

That Fed control over the money supply has become a phantom has been quite clear since the Minsky moment in 2008, with the Fed massively expanding its balance sheet without much resulting increase in measured money supply. This of course has made a hash of all the people ranting about the Fed "printing money," which presumably will lead to hyperinflation any minute (eeek!). But the deeper story that some of us were unaware of is that apparently this disjuncture happened a long time ago. Even so, one of our number pointed out that official Fed literature and even many Fed employees still sell the reserve base story tied to a money multiplier to the public, just as one continues to find it in the textbooks, But apparently most of them know better, and the money multiplier became a myth a long time ago.Woj’s Thoughts - Rosser refers to a paper from the Federal Reserve Board’s Finance and Economics Discussion Series that was the source of a recent Quote of the Week:

“Money, Reserves, and the Transmission of Monetary Policy: Does the Money Multiplier Exist?” (by Seth B. Carpenter and Selva Demiralp, May 2010):

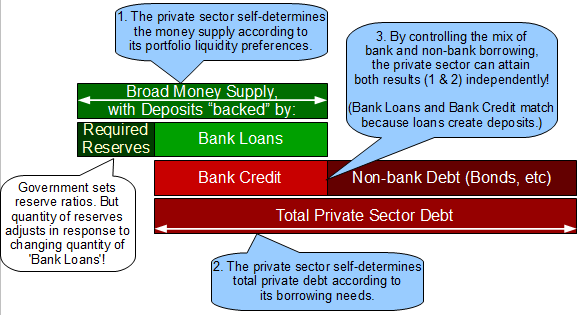

Changes in reserves are unrelated to changes in lending, and open market operations do not have a direct impact on lending. We conclude that the textbook treatment of money in the transmission mechanism can be rejected.As I noted in that post:

If staff members at the Federal Reserve are aware of the money multiplier myth than surely Bernanke and the other board members have heard the arguments. Unfortunately most mainstream economists, especially monetarists, continue to promote monetary stimulus as if the old regime still persists.Fortunately the economics professors at James Madison stumbled across this paper and were convinced of its conclusion. Hopefully they will join a minority of current economists in training future economists to recognize the money multiplier does not exist.

Related posts:

Fullwiler - "The main shortcoming of the money multiplier paradigm"

IOR Killed the Money Multiplier

Fighting for Endogenous Money on Two Fronts

Actually, both the ECB and BIS also know that the multiplier does not exist:

ReplyDeletehttp://www.ecb.europa.eu/pub/pdf/mobu/mb201205en.pdf

"The occurrence of significant excess central bank liquidity does not, in itself, necessarily imply an accelerated expansion of MFI credit to the private sector. If credit institutions were constrained in their capacity to lend by their holdings of central bank reserves, then the easing of this constraint would result mechanically in an increase in the supply of credit. The Eurosystem, however, as the monopoly supplier of central bank reserves in the euro area, always provides the banking system with the liquidity required to meet the aggregate reserve requirement. In fact, the ECB’s reserve requirements are backward-looking, i.e. they depend on the stock of deposits (and other liabilities of credit institutions) subject to reserve requirements as it stood in the previous period, and thus after banks have extended the credit demanded by their customers."

http://www.bis.org/publ/work297.pdf

"This paper contends that the emphasis on policy-induced changes in deposits is misplaced. If anything, the process actually works in reverse, with loans driving deposits. In particular, it is argued that the concept of the money multiplier is flawed and uninformative in terms of analyzing the dynamics of bank lending. Under a fiat money standard and liberalized financial system, there is no exogenous constraint on the supply of credit except through regulatory capital requirements. An adequately capitalized banking system can always fulfill the demand for loans if it wishes to."

Thanks for bringing those papers to my attention. Most central bankers therefore realize the multiplier doesn't exist, yet I still had the privilege of learning the loanable funds model in class last night.

DeleteOn the positive side, I spent a couple hours yesterday discussing/teaching Post-Keynesian endogenous money to a few Austrians in my program. Their reaction, "so it's a theory about how the monetary system works in practice." Exactly!

The cognitive dissonance you must experience as a Economics student knowing what you know must be immense!

ReplyDeleteAs a layperson I often find myself aghast at the apparent disconnect between what is supposedly mainstream theory and reality.

Read my comment (above) to Kostas...you're exactly right! Hopefully I can convert enough others to help slowly change the tide going forward.

DeleteWhat happens if the Fed stops paying interest on reserves? Does the multiplier matter then? Does it re-appear? How would banks meet reserve requirements?

ReplyDeletePaying IOR actually does not alter the existence of a money multiplier. Although in theory it could exist, to my knowledge it has never existed in practice (at least not within the US).

DeleteLoans create deposits, which can in turn generate demand for reserve balances (for either requirement or settlement purposes). If the Fed does not provide enough reserves to meet requirements, the interbank rate will rise to the discount window rate (where the Fed promises to provide unlimited reserves). If for some reason the Fed elected not to provide reserves through the discount window, payments made against the initial loans would bounce and the bank short on reserves would effectively be in default. Since a primary goal of the Fed is to ensure a functioning payments system, the Fed is highly incentivized not to take this path.

A good example to keep in mind is Canada, which has no reserve requirements. In fact, the banking system in aggregate typically holds zero reserves overnight. Despite this policy, banks are still perfectly able to make loans upon demand.

Woj, Thanks for the response. This topic has had me up all night, and is not helping with my recovery! lol. I looked at a recent post by Billy Mitchell that I think you might consider adding to your related post roster: http://bilbo.economicoutlook.net/blog/?p=10733.

ReplyDeleteSo the main argument is that the central bank cannot determine the supply of money under a fiat currency regime? As Mitchell explains: So the supply of money is determined endogenously by the level of GDP, which means it is a dynamic (rather than a static) concept. Central banks clearly do not determine the volume of deposits held each day. These arise from decisions by commercial banks to make loans. The central bank can determine the price of “money” by setting the interest rate on bank reserves.....

I think there is a connection between this post and your other post, "The Fed's Massive Amounts of Treasuries Won't Be Unwound" I'm still trying to figure it out. What do you think of the idea of sterilizing the debt? Or is this not possible either under a fiat currency system?

nanute, sorry for keeping you up. I've definitely had similar experiences although maintaining good health is a bit more important.

DeleteThanks for the link as well. Mitchell is definitely a great resource on modern monetary operations and I agree with the points you noted above.

As for the connection, I'm not quite sure but am certainly open to ideas. When you suggest "sterilizing the debt", what exactly do you mean? Cancelling the Treasuries? Buying all new issues? Once I have a better idea I can hopefully outline my thoughts a little more.

Here's a part of the idea of sterilizing v, monetizing the debt from Rebecca Wilder: first, let’s address sterilizing the monetary base. The Fed’s standard monetary transaction is to maintain the federal funds rate - the interest rate at which U.S. banks make overnight loans to each other - at (or close to, see this post ) the Fed’s chosen target by injecting (the rate falls) and extracting (the rate rises) liquidity from the banking system. Usually the Fed does this through repurchase agreements (repos) or by manipulating the stock of Treasuries on its balance sheet (see Table below).

ReplyDeleteHowever, when the Fed wants to keep the federal funds rate unchanged but add liquidity by other means (perhaps by auctioning off funds), the Fed sterilizes the effects of the new liquidity on the monetary base by performing an offsetting open market operation - an overnight repo or selling Treasuries outright.

The counterfactual: The Fed does not sterilize a new TAF auction – let’s say in the amount of $150 billion – and the money supply rises. The Fed allows the new $150 billion to stay in the banking system as excess reserves, which increases the supply of federal funds and reduces the federal funds rate (below the Fed’s target). The money supply increases as banks loan out the new funds, which is inflationary – too much money chasing the same number of goods and services....http://www.newsneconomics.com/2008/11/monetization-sterilization-whats-going.html

In other words, if the Fed does not put funds back into the system via excess reserves, the effect would cancel out the increase in the money supply. In effect, sterilizing the currency. I believe this happened during the depression but at that time we were still operating on a gold standard. Or, am I way off base here?

I think this is a bit off base. Here's my take:

DeleteThe Fed adjusts the interbank overnight rate simply through "open mouth" operations because the threat of intervention is enough to move the market. On a regular basis the Fed engages in open market operations to maintain a level of reserves necessary to meet requirements and payment obligations, in effect countering changes due to govt spending and bank lending (Fed acts passively). If the Fed is forced to extend liquidity either domestically or internationally that would create excess reserves, it can either sterilize the change or allow the interbank rate to fall to the IOR rate. Prior to 2008 the Fed always chose the former option.

Since 2008, the Fed has been operating under a "permanent floor" monetary regime. Expansion of the balance sheet does not result in any change to the interbank rate since the rate is already at the floor (IOR rate). While QE expands the money supply, it does not necessarily increase the amount of bank loans and certainly does not increase loanable funds, which are not constrained by reserves.

The Fed's actions, per-2008, to sterilize the currency were therefore decisions to maintain the current target rate while providing extra liquidity to certain pockets of the market.

Not sure if that answers your initial question or not. If not, let me know and I'll try to expand.

Woj,

ReplyDeleteThanks. It answers my question. I guess well just have to wait and see how the Fed unwinds that massive amount of Treasuries it's been purchasing. Or, if like you say it can't be unwound.