1) Ergodicity – the biggest mistake ever made in economics by Lars P Syll

Samuelson said that we should accept the ergodic hypothesis because if a system is not ergodic you cannot treat it scientifically. First of all, that’s incorrect, although I think I understand how he ended up with this impression: ergodicity means that a system is very insensitive to initial conditions or perturbations and details of the dynamics, and that makes it easy to make universal statements about such systems …

Another problem with Samuelson’s statement is the logic: we should accept this hypothesis because then we can make universal statements. But before we make any hypothesis—even one that makes our lives easier—we should check whether we know it to be wrong. In this case, there’s nothing to hypothesize. Financial and economic systems are non-ergodic. And if that means we can’t say anything meaningful, then perhaps we shouldn’t try to make meaningful claims. Well, perhaps we can speak for entertainment, but we cannot claim that it’s meaningful.

…

The only reason risk exists is that we cannot go back and make decisions over again. Economics got very confused about the point of dealing with risk, and had to resort to introducing psychology and human behavior and all sorts of things. I don’t mean to say that we don’t need behavioral economics. What I mean is that there are lots of questions in economics that we can only answer behaviorally at the moment, but at the same time we have a perfectly formal natural physical analytic answer that’s very intuitive and sensible and that comes straight out of recognizing the non-ergodicity of the situation.

To be blunter, I’m pointing out that economics is internally inconsistent. I accept all the models that economists have developed. I could critique them, but I’m not worried about that. I didn’t make them up, the economists did. But when the economists treat the models as if they were ergodic, that’s when someone has to say “stop, that’s enough.”

-Ole PetersWoj’s Thoughts - This timely quote will provide sufficient background for recognizing the importance of the following paper/post...

2) The power and the terror of Irrational Expectations by Noah Smith @ Noahpinion

2) The power and the terror of Irrational Expectations by Noah Smith @ NoahpinionBut to me, that's not even the most disturbing implication of Malmendier's finding, and of this type of expectations model in general. In most theories of non-rational expectations, like Bayesian learning or rational inattention, expectations evolve in a smooth, stable way. And so these models, as Chris Sims writes, look reassuringly like rational-expectations models. But there is no guarantee that real-world expectations must behave according to a stable, tractable model. I see no a priori reason to reject the possibility that expectations react in highly unstable, nonlinear ways. Like tectonic plates that build up pressure and then slip suddenly and unpredictably, expectations may be subject to some kind of "cascades". This can happen in some simple examples, like in the theory of "information cascades" (In that theory, people are actually rational, but incomplete markets prevent their information from reaching the market, and beliefs can shift abruptly as a result). In the real world, with its tangle of incomplete markets, bounded rationality, and structural change, expectations may be subject to all kinds of instabilities.

In other words, to use Lucas' turn of phrase, expectations might just make themselves up...and we might get any result that we don't want.

What if inflation expectations change suddenly and catastrophically? That would probably spell the death knell for macro theories in which the central bank can smoothly steer the path of things like inflation, NGDP, etc. It would raisethe specter of an "inflation snap-up" (or "overshoot", or "excluded middle") - the central bank might be unsuccessful in beating deflation, right up until the moment when hyperinflation runs wild.

And what would be the implications of financial markets and financial theories of the macroeconomy? Belief cascades could obviously cause asset market crashes. It seems like sudden changes in expectations of asset price appreciation might also cause abrupt and long-lasting changes in saving and investment behavior. Which in turn could cause...well, long economic stagnations.

A very disturbing thought.Woj’s Thoughts - While I have yet to read the recent paper by Ulrike Malmendier, I think Noah’s final comment is probably representative of most mainstream economists and perhaps a large percentage of the general population. The basic idea that expectations may not be formed by stable processes suggests that reality is non-ergodic and future outcomes may be path dependent. If so, not only would mainstream macro theories be severely undermined, but also the notion that we can control the future. Although I recognize this lack of control can be scary, in many ways the uncertainty of life is what makes living so special. As the first quote demonstrates, many heterodox economists have already come to terms with the non-ergodic nature of reality and set out to create macro theories acknowledging reality as such. Ultimately I am a firm believer that accepting greater uncertainty allows for advancements in protecting against the unknown risks. The current state of macroeconomics would benefit greatly from moving in that direction.

"Ultimately I am a firm believer that accepting greater uncertainty allows for advancements in protecting against the unknown risks. The current state of macroeconomics would benefit greatly from moving in that direction."

ReplyDeleteNot clear what you mean by "accepting greater uncertainty". Maybe, choosing to be more careful all the time. Maybe the opposite of that.

There is always risk and uncertainty. There is risk and uncertainty when one drives a new car on a new superhighway. But there is greater risk and uncertainty when one tries to see how close one can drive to the edge of the precipice.

No matter the ergodics, if we insist on following a path of greatest risk, there is less uncertainty of danger in the outcome.

The purpose of policy is to establish boundaries that limit us to the safe side, so that the macro economy does not suffer while the luckiest micro-economic risk-takers profit.

ah, a conclusion so obscure only a non-scientist could oppose it, right? **rolls-eyes**

Delete:)

DeleteIt seems I was using words to discover my thoughts.

**shrugs shoulders**

Speaking from a finance background, I see the ergodic hypothesis, REH and EMH as ruling out uncertainty by creating an environment where it appears all risks can be measured. This appearance that the actual risk is known at any time, for any outcome, leads to an overconfidence in one's ability to maximize profits/utility by accepting greater leverage. From this finance perspective, I probably should have said simply accepting uncertainty is a good start to reducing the number of blow ups from "tail risk."

DeleteLooking beyond finance, I think many people (myself included) want to feel we have more control over life outcomes than is true and maybe even possible. On this level I think accepting greater uncertainty as a part of life can make negative surprises easier to handle and get through.

Hopefully that makes my conclusion a bit clearer.

That helps. Thanks Woj. "Uncertainty", meaning not risk, but the inability to measure risk.

ReplyDeleteMy son Jerry helps me understand the word "ergodic"

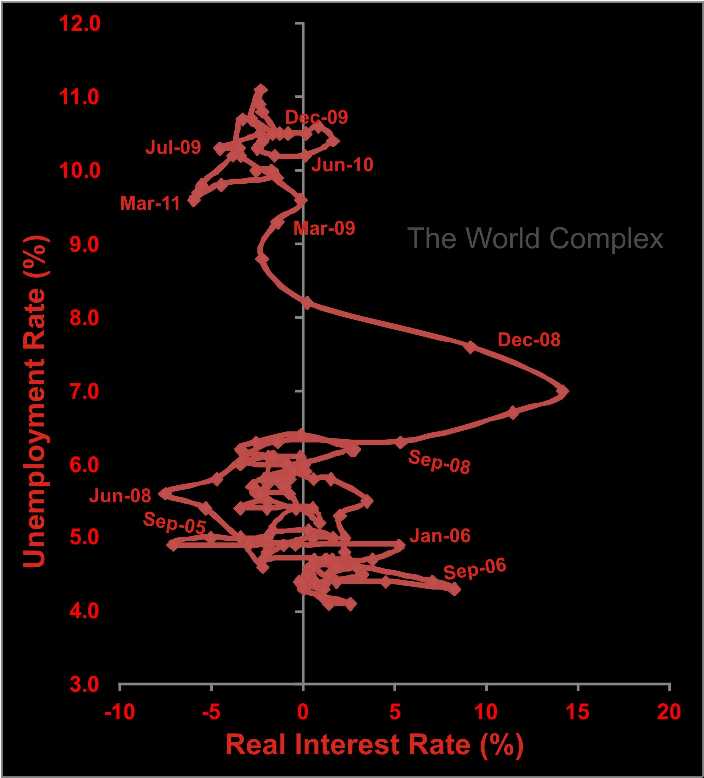

For a "phase space" of all possible conditions, I like the Phillips graph: all possible combinations of inflation and unemployment. Mr. Phillips' own 100 years of empirical data show that the economy "wants" to occupy a particular region of the graph. Economists of the 1960s were certain of it.

But Milton Friedman said "no-no" and since that time, the economy has been all over the phase space. As Noah's graph shows.

My view is that the results since Friedman spoke, are the results of bad policy, not ergodics. The precipice along which we drive is the path of the greatest possible private debt. The longer we insist on following this path, the more risk there is of (for example) a sudden and catastrophic change in expectations.

If we insist upon taking the precipice road, both the realities and the expectations are different. So I guess, yes: future outcomes are path dependent, as you say.

Two roads diverged in a wood, and I—

I took the one less traveled by,

And that has made all the difference.

Typically when I speak of uncertainty I'm thinking of Knightian uncertainty.

DeleteYour son seems to have a very good grasp on ergodic vs non-ergodic systems. To my knowledge, Paul Davidson brought this debate back to economics about 30 years ago.

In terms of the Phillips curve, I think you would find that empirical data across countries and over longer stretches of time tends to resemble Noah's graph far more than Phillips'. That's not to say policy can't alter the levels or that there is no relationship between the variables.

The point of viewing the system as non-ergodic is to recognize that the specific relationship between inflation and unemployment, in this case, is not stable over time. A set of policies that can definitively maintain the combination in a certain region is not merely unknown, but cannot be known. Furthermore, attempts to contain inflation and unemployment will alter other economic factors (i.e. growth, distribution, productivity) in ways that are unknown (ceteris paribus means very little when speaking about the macro economy).

To be honest, whenever I hear the word ergodic, I generally switch off. Can anyone tell me why arguments that can be applied to any arbitrary neoliberal policy cannot equally be applied to post Keynesian policies as well?

ReplyDeleteOn the contrary I think many arguments can be applied to both, especially those that suggest caution due to the inherent uncertainty in trying to control unstable relationships.

DeleteIMO neoclassical economics has gone much further in banishing uncertainty and other aspects of the real world in order to create tractable (determinate) mathematical models. In doing so, those models have not only relinquished predictive power but also weakened the link between effects of policies on the model and those in the real world.

There probably are other specific arguments you have in mind. If you could expand a bit on those it might help myself or others try to address whether or not they apply to both sets of policies.

Can you give me an example of a universal statement that is commonly made by post Keynesians but violates non-ergodicity?

DeleteOff the top of my head, can't say that I can. As best I can tell the Post Keynesians have made it a priority to reject the ergodic axiom for quite some time. I'll try to dig a little deeper and see what I can come up with.

DeleteCould you give me an example of how post Keynesians have incorporated this rejection into their economic theory, then?

DeleteHere is one of the more frequently cited papers on the subject by Paul Davidson, "Is Probability Theory Relevant for Uncertainty? A Post Keynesian Perspective": http://stevereads.com/papers_to_read/is_probability_theory_relevant_for_uncertainty_a_post_keynesian_perspective.pdf

Delete