1) Musings on MMT - Firming Up The Soft Bits by Neil Wilson @ 3spoken

Effect on the Exchange Rate

The problem here I think is a matter of viewpoint. The world is a closed system. Each individual monetary area operates within that closed system. So if you press in one area, the results of that will pop up somewhere else in the world.

The world can be modelled as an interacting set of non-convertible floating rate monetary systems (with pegged nations treated as part of the currency area they are pegged to). So that means for your currency to go down all the others have to go up. It only takes the central bank of one of the other areas to start buying your currency to halt that decline.

And if a currency area has an export led policy, then they will intervene to assist their exporters by providing liquidity in the currency the exporters actually want - their own. This is pretty much what the Swiss did against the Euro, and frankly as the Chinese central bank does against pretty much everything.

So I think the driver is not so much demand for your currency, as desire to access your market by foreign exporters. And that is obviously linked to how wealthy your country is perceived by export-led nations. (my emphasis)Woj’s Thoughts - Recently I’ve spent significant time thinking about exchange rate movements in relation to the current monetary system. My initial impression was that two separate theories may be necessary to explain the effects of trying to depreciate or appreciate a given currency. Neil’s observation in bold may provide a common link to explain observed changes. The focus on exports (trade) does, however, leave out demand for access to financial markets as a potential driver. While this may only be meaningful for the largest developed countries, all of these questions will require further exploration.

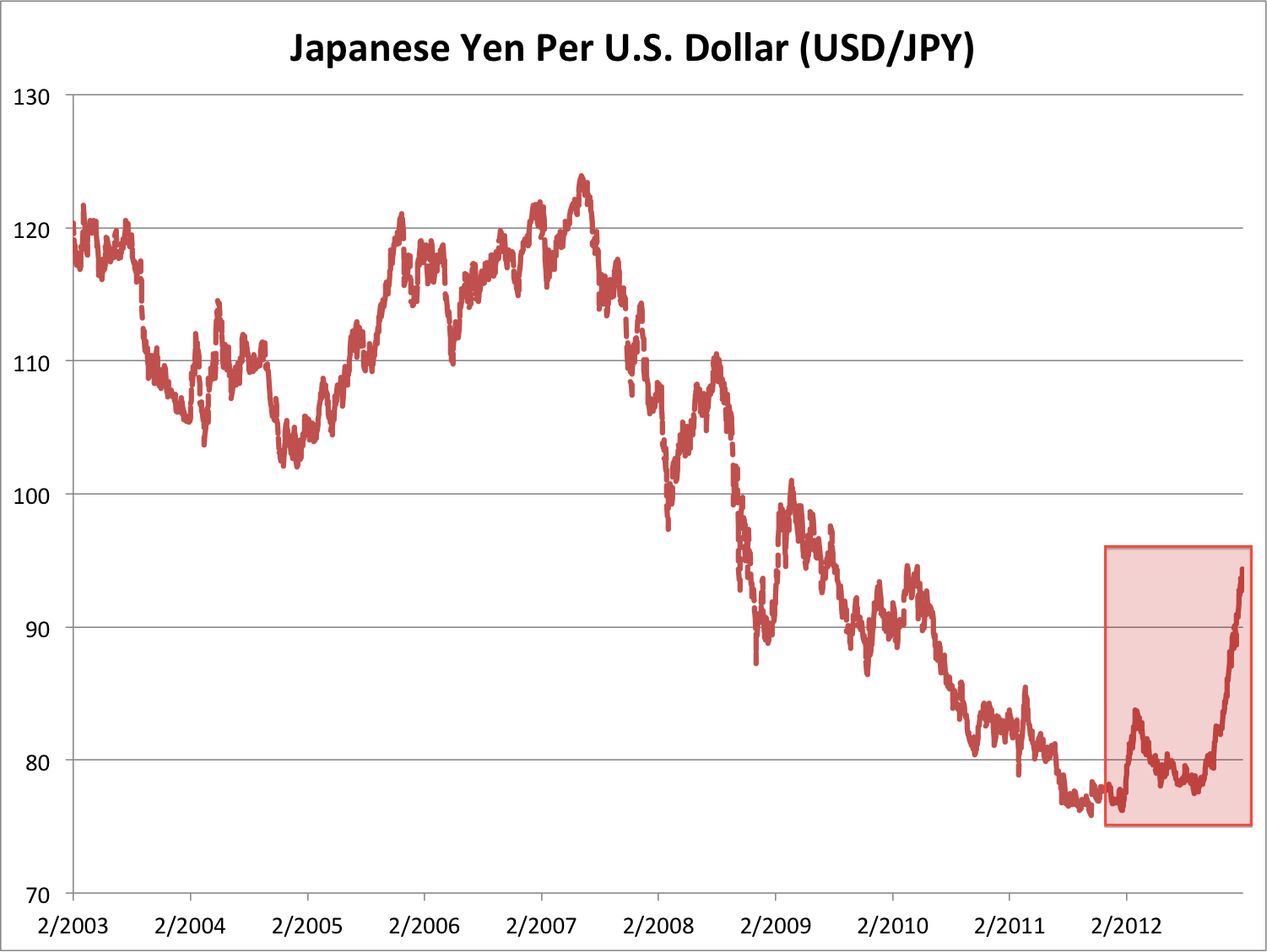

2) a word on the euro, US deficit doves, and Japan by Warren Mosler @ The Center of the Universe

Japan’s weak yen, pro inflation policy seems to have been all talk with only a modest fiscal expansion to do the heavy lifting. Changing targets does nothing, nor does the BOJ have any tools that do the trick as evidenced now by two decades of using all those tools to the max. And while I’ve been saying all the while that 0 rates, QE, and all that are deflationary biases that make the yen stronger, there is no sign of that understanding even being considered by policy makers, so expect more of same. What has been happening to weaken the yen is a quasi govt policy of the large pension funds and insurance companies buying euro and dollar denominated bonds, which shifts their portfolio compositions from yen to euros and dollars, thereby acting to weaken the yen. I have no idea now long this will continue, but if history is any guide, it could go on for a considerable period of time. Yes, it adds substantial fx risk to those institutions, but that kind of thing has never gotten in the way before. And should it all blow up some day, look for the govt to simply write the check and move on.Woj’s Thoughts - Though I expect the yen to strengthen a bit by the end of the year, the willingness of Japanese pension funds and insurance companies to continue increasing fx risk remains a wildcard. Considering the large negative impact on GDP from declining exports in the fourth quarter, it will be interesting to see what effect the weakening yen has on Japan’s trade balance going forward.

No comments:

Post a Comment